Miniaturization Boom Accelerates Global Surface Mount Switch Market Toward $7.9 Billion by 2031

Other |

2026-05-26 05:53:25

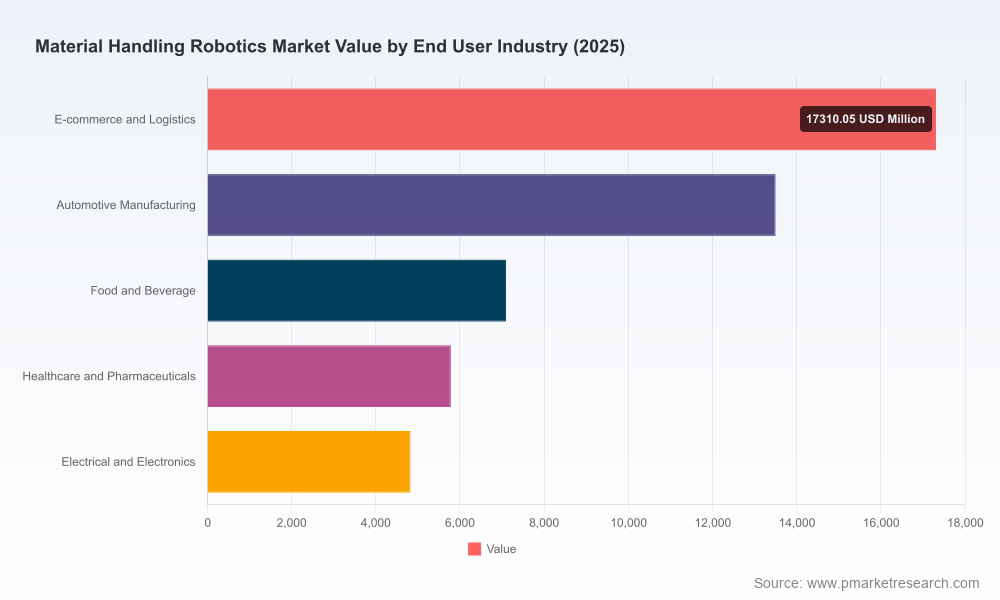

As organizations prepare capital and operational plans for 2026, material handling robotics has moved from a niche automation option to a strategic enabler across manufacturing, logistics and distribution. PW Consulting’s new Market Research on Material Handling Robotics (base year 2025, forecast 2026–2032) provides a data-driven, execution-focused playbook for executives, supply‑chain leaders and technology investors. The market’s recent trajectory — accelerating from roughly USD 25.1 billion in 2020 to USD 48.5 billion in 2025, and forecast to expand at a compound annual growth rate (CAGR) of 15.01% through the 2026–2032 period — underscores the urgency of making informed choices in 2026.

Material Handling Robotics Market Research

Timing of adoption: 2026 is a structural inflection year. The market momentum entering 2026 creates a window for adopters to lock in favorable supplier capacity, secure integration partners and pilot programs before broader demand drives lead times and pricing pressure.

Material Handling Robotics Market Research

Risk-adjusted investment: With a high-growth market, capital allocation requires a clearly articulated risk-return framework. Our report translates market-level growth into actionable investment thresholds, payback horizons and sensitivity scenarios tailored for board-level approval processes.

Material Handling Robotics Market Research

Vendor selection and negotiation: The industry exhibits moderate concentration at the top—our analysis of market concentration (CR3 ~38.5%; CR5 ~52.1%) shows leading vendors maintain meaningful share but a healthy competitive set remains. This dynamics creates leverage opportunities for buyers who rigorously benchmark total cost of ownership (TCO), service SLAs and integration roadmaps.

Operational readiness: Beyond hardware selection, the biggest determinant of value capture is operational integration—workforce redesign, control-system interoperability and data pipelines into supply‑chain planning. The report provides operational templates and a stepwise implementation roadmap to reduce time-to-value.

Market sizing and scenario modelling — transparent methodologies that map macro demand drivers to addressable market estimates for 2026–2032, including stress tests for demand shocks and supply constraints.

Technology assessment — comparative evaluation of key robotic modalities, software stacks, perception systems and end‑of‑arm tooling across common material handling tasks.

Implementation playbooks — 90–180–365 day plans for proof-of-concept to scaled rollout, with checklists for site readiness, safety validation and workforce re-skilling.

Commercial frameworks — templates for RFPs, commercial negotiation levers (warranty, spare-parts economics, software licensing), and a supplier scorecard tailored to material handling use cases.

TCO & ROI models — configurable calculators that capture capital, installation, recurring maintenance, downtime risk and labor offset assumptions so CFOs can compare leasing vs. buying and capex timing alternatives.

Regulatory & standards index — curated guidance on safety, interoperability and Industry 4.0 mandates most relevant to 2026 deployments.

M&A & partnership playbook — opportunities and risks for strategic acquisitions, minority investments and strategic alliances in the rapidly consolidating landscape.

The report’s vendor analysis profiles incumbent robotics OEMs and system integrators that shape procurement and innovation trajectories. Key players examined include FANUC, ABB Robotics, KUKA, Yaskawa (Motoman), Kawasaki, Daifuku, SSI SCHAEFER, Dematic, Stäubli, Jungheinrich, Honeywell Intelligrated, Toyota Material Handling, Geek+, OTTO Motors (Clearpath) and Seegrid. Each profile synthesizes product focus, go-to-market motions and partnership ecosystems.

Strategic incumbents (e.g., long-established industrial robotics OEMs) emphasize reliability, payload capability and deep service networks—traits that favor high-throughput, heavy-pallet environments.

Systems integrators and automation platform providers concentrate on end‑to‑end solutions—combining robotics, AS/RS, conveyors and WMS integration—which reduces buyer integration risk but can raise switching costs.

Emerging AMR and vision-guided specialists prioritize rapid deployment, flexibility and software-defined behaviors—appealing for e-commerce and dynamic fulfillment operations that require goods-to-person models.

Geopolitical and supply-chain positioning matters: vendors with diversified manufacturing footprints and established parts distribution networks provide resilience against raw-material and logistics shocks.

For procurement teams, the implication is clear: negotiate on serviceability, modular upgrades and software portability, not just on headline robot unit prices. For investors, the combination of moderate top-end concentration and ongoing technological differentiation points to selective opportunities in software layers, perception, and integration-as-a-service models.

Labor scarcity and rising labor cost pressures remain a primary adoption catalyst. Persistent skilled labor shortages across warehousing and manufacturing continue to accelerate automation strategies as firms seek predictable throughput and reduced dependency on volatile labor markets.

Regulatory momentum for Industry 4.0 and interoperability standards is lowering integration friction. Policy and standards alignment in 2025–2026 are improving the plug-and-play potential of heterogeneous robotic fleets.

Raw material and component cost structures are non-trivial: high-grade steel and advanced polymers account for a sizeable portion of production costs in robotic structures and modules. That reality should inform procurement cadence and supplier diversification strategies for 2026 deployments.

E-commerce-driven distribution expansion continues to be a reliable demand engine, pressing logistics operators to prioritize flexible, scalable robotic systems that support rapid SKU proliferation and peak-season variability.

Trade-show momentum: leading robotics OEMs and integrators showcased new material handling solutions at MODEX 2026. These events reveal product roadmaps and partnership alignments that often presage commercial rollouts.

Product updates from AMR and AGV vendors late in 2025–early 2026 emphasize autonomy, fleet orchestration and safety enhancements—areas that materially reduce total integration cost for greenfield and brownfield sites.

Consolidation and partnership activity remains active. Watch for M&A that bundles software orchestration platforms with hardware incumbents; these combos can accelerate adoption but also alter competitive dynamics for mid‑market buyers.

Prioritize modularity. Design projects around modular cells and software-defined behaviors so you can scale incrementally and redeploy assets as demand patterns evolve.

Run dual-track pilots: one focusing on throughput-heavy, high-certainty tasks (quick ROI) and another on flexibility-centric use cases (longer-term strategic value). This balances short-term returns with future-proofing.

Embed TCO governance into procurement. Require multi-year TCO projections, spare-parts lead-time commitments and software upgrade roadmaps as preconditions in major contracts.

Invest in internal capabilities. Make 2026 the year to upskill operational teams in robot maintenance, fleet orchestration and data analytics—outsourcing can only carry you so far.

Manage supply risk actively. Given material-cost realities and lead-time sensitivity, diversify suppliers and consider multi-sourcing critical components or staging purchases to mitigate cost spikes.

Prepare governance for human-machine transition. Create workforce transition plans that combine retraining, safety protocols and clear career pathways to preserve morale and institutional knowledge.

PW Consulting’s full Material Handling Robotics report provides the detailed segment tables, vendor scorecards, implementation templates and downloadable financial models that executives need to make 2026 commitments with confidence. In keeping with our “trailer” approach, this briefing surfaces the strategic contours and practical implications; the in‑depth, segment-level datasets and proprietary supplier benchmarking are available in the complete report for subscribers and clients.

For leaders setting budgets, negotiating suppliers or evaluating acquisitions in 2026, the choices you make now will determine competitive positioning for the next decade. PW Consulting’s research converts noisy market signals into disciplined decision frameworks—helping you move from vendor evaluation to operational deployment with speed and predictability.

Contact PW Consulting to access the full report, the scenario models, and a tailored briefing that applies these findings to your specific operations and strategic objectives.

For detailed analysis of this topic, please visit the official page:Material Handling Robotics Market Research

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com