Asthma and COPD Drugs Market Dynamics, Drivers, Restraints, and Opportunities

Health |

2026-06-01 11:48:11

As digestive health continues to move from niche therapeutic use into mainstream preventive and personalized nutrition, the global Digestive Enzyme Complex market is entering a phase where strategic choices made in 2026 will disproportionately determine market leadership through the forecast window. PW Consulting’s new market intelligence briefing — grounded in a 2020–2025 historical base and a 2026–2032 forecast — synthesizes commercial, regulatory, and supply-side signals into actionable decision pathways for C-suite and business unit leaders.

Digestive Enzyme Complex Market

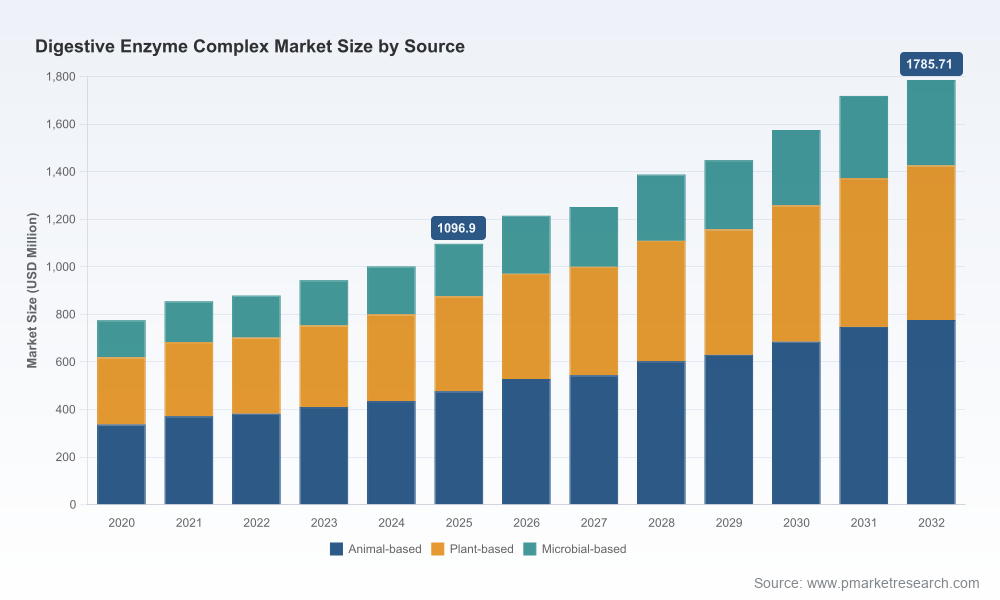

The market has demonstrated steady expansion over the historical period and is projected to continue growing at a compound annual growth rate (CAGR) of approximately 7.21% through the forecast horizon. This expansion reflects both increasing consumer and clinical demand for digestive support solutions and sustained innovation across enzyme sources and formulations. Market concentration is moderate: the top three companies account for roughly one-third of market value, while the top five approach just under half — a structure that creates opportunity for specialist manufacturers, agile brands, and strategic consolidators alike.

Digestive Enzyme Complex Market

Acceleration in mainstream adoption. Consumer and practitioner channels are converging: evidence-based enzyme formulations are moving from prescription and practitioner-only channels into retail and e-commerce at a faster pace. Companies that can bridge clinical credibility with scalable retail execution will gain disproportionate share.

Digestive Enzyme Complex Market

Supply and regulatory inflection. Recent capacity investments and regulatory scrutiny of animal-derived pancrelipase therapies have amplified the importance of supply security and source transparency. Firms that secure diversified supplier networks or develop non-animal enzyme platforms will mitigate downside risk.

Product & market segmentation maturation. Buyers increasingly demand targeted claims (e.g., symptom relief, nutrient absorption, compatibility with specific diets) and delivery formats (clinician-prescribed, direct-to-consumer, practitioner-only). The players that combine clinical data with clear channel strategies will outpace competitors that rely on legacy formulations alone.

This briefing is built as an operator’s playbook, not an academic survey. Clients can expect:

Scenario-led demand models spanning conservative, baseline, and upside adoption paths through 2032 — enabling stress-tested revenue and capacity planning.

Supply-risk heatmaps and a supplier due-diligence toolkit that quantify exposure to animal-sourced raw materials, single-source APIs, and geopolitical concentration.

Regulatory impact guides that translate FDA and regional guidance into commercial development gates (labeling, safety dossiers, clinical endpoints, contamination controls) and a checklist for transitioning products between therapeutic and supplement classifications where applicable.

Channel and pricing playbooks: margin maps for practitioner, retail, and e-commerce channels; private-label and contract-manufacturing decision trees; and a practical commercialization timeline for clinician-to-consumer launches.

Innovation and formulation templates: prioritized enzyme portfolios (animal, plant, microbial), stability/encapsulation strategies for oral delivery formats, and an R&D roadmap that aligns clinical validation with claims defensibility.

Competitive benchmark matrices and an M&A playbook: valuation sensitivities, integration risk factors for manufacturing assets, and a shortlist of strategic acquisition archetypes (raw-material control, formulation capability, channel access).

The market is populated by a mix of global pharmaceutical incumbents, ingredient suppliers, specialty enzyme manufacturers, and health-and-wellness brands. Key strategic observations from our company-level analysis:

AbbVie (Creon): As the incumbent PERT supplier with an established prescription foothold, AbbVie illustrates the durability of clinical brands in therapeutic segments. For competitors, the strategic lesson is threefold — maintain clinical partnerships, preempt supply bottlenecks, and invest in payer-facing evidence generation when targeting therapeutic indications.

Enzymedica, Garden of Life, NOW Foods and similar consumer brands: These companies demonstrate how clean-label, plant-forward messaging and trusted retail distribution can scale enzyme complexes to mainstream consumers. Brand-led entrants should prioritize formulation transparency, third-party testing, and e-commerce optimization to protect margins as competition intensifies.

Specialty manufacturers (Bioseutica/Neova, Specialty Enzymes & Probiotics, Amano, DSM-Firmenich, Advanced Enzyme Technologies): These suppliers are the innovation engine — offering tailored enzyme systems, clinical-grade actives, and manufacturing scale. Strategic buyers should evaluate partnerships or minority investments to secure preferential supply and co-develop next-generation enzyme stacks with differentiated claims.

Contract manufacturing and nutritional ingredient providers (National Enzyme Company / ADM-Deerland): The integration of ingredient supply with CMO services accelerates time-to-market for private-label and mid-sized brands. Vertical buyers should weigh the trade-offs between owning a CMO vs. long-term offtake agreements to lock capacity.

Innovative challenger entrants (examples: Microbiome Labs, Enzyme Science): New product formats that combine enzymes with probiotics or microbiome-targeted ingredients are testing new demand vectors. Monitoring small but fast-moving launches is essential for incumbent strategy — either to replicate or to acquire complementary IP.

FDA and product classification. Several digestive enzyme products straddle the line between dietary supplement and therapeutic product. The regulatory landscape requires detailed characterization of enzyme sources (animal, plant, microbial) and manufacturing controls to prevent contamination — a key gating item for any product moving toward clinical claims.

Porcine-derived enzyme sourcing. Pancreatic enzyme therapies remain largely animal-sourced in certain therapeutic niches. This creates both supply fragility and reputational risk; companies should model scenarios that include procurement constraints, alternative sourcing, and consumer sensitivities (religious, cultural).

Capacity investments and supply announcements. Recent announcements by major supply-side actors to expand API or finished-dose capacity indicate the market’s response to sustained demand. For purchasers and brand owners, securing multi-year supply agreements or strategic equity stakes in key manufacturers will reduce time-to-market risk.

1) Diversify enzyme sourcing and formulation platforms. Prioritize a dual-track R&D strategy that advances plant/microbial alternatives while protecting critical animal-derived supply where clinically necessary.

2) Invest in claims-defensible clinical evidence. Allocate a portion of R&D to pragmatic, endpoints-driven trials that support high-value claims and payer discussions for therapeutic applications.

3) Lock supply via partnerships or partial vertical integration. Assess the economics of upstream investment versus offtake contracts; use supply-risk heatmaps to prioritize negotiations.

4) Channel-sense segmentation. Develop differentiated GTM strategies for practitioner channels, retail, and DTC—each requires unique packaging, pricing, and evidence strategies.

5) Build M&A optionality. Target acquisitions that close capability gaps: specialty manufacturing for scale, niche brands for route-to-consumer access, or ingredient companies for long-term margin protections.

PW Consulting’s Digestive Enzyme Complex briefing is designed as an executive decision tool for 2026 strategic planning cycles: use it to inform capital allocation, R&D prioritization, supply-chain stabilization, and M&A screening. The report translates complex market dynamics into prioritized actions and measurable milestones to track execution over quarterly and annual planning horizons.

This article previews the intelligence depth and operational orientation of the full report while intentionally withholding granular segmentation figures and proprietary model outputs to preserve analytic value for subscribers. For the complete dataset — including the detailed scenario models, supplier scorecards, channel-level economics, and downloadable decision-support templates — please visit our report page or contact your PW Consulting account lead to request access.

In a market growing at a steady mid-single-digit CAGR and undergoing both clinical and consumer evolution, the choices firms make in 2026 about sourcing, evidence generation, and channel strategy will define competitive boundaries for the coming decade. PW Consulting’s analysis equips leaders to make those choices with confidence.

For detailed analysis of this topic, please visit the official page:Digestive Enzyme Complex Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com