Swing Granulator Market Outlook 2026: Strategic Imperatives for Buyers, OEMs and Investors

PW Consulting today releases its authoritative industry briefing derived from the new Swing Granulator Market report (base year: 2025; historical series: 2020–2025; forecast horizon: 2026–2032). As the senior strategy team and lead industry analyst, we present a concise, decision-focused synthesis designed to inform procurement, investment, and product strategy in 2026. Highlights: the global swing granulator market is estimated at approximately USD 1.3 billion in 2025 and, under our baseline scenario, is projected to grow to just under USD 2.0 billion by 2032 at a compound annual growth rate (CAGR) of 6.2% over the forecast period. This release previews the report’s strategic findings while preserving detailed segment tables to encourage direct engagement with the full report on our website.

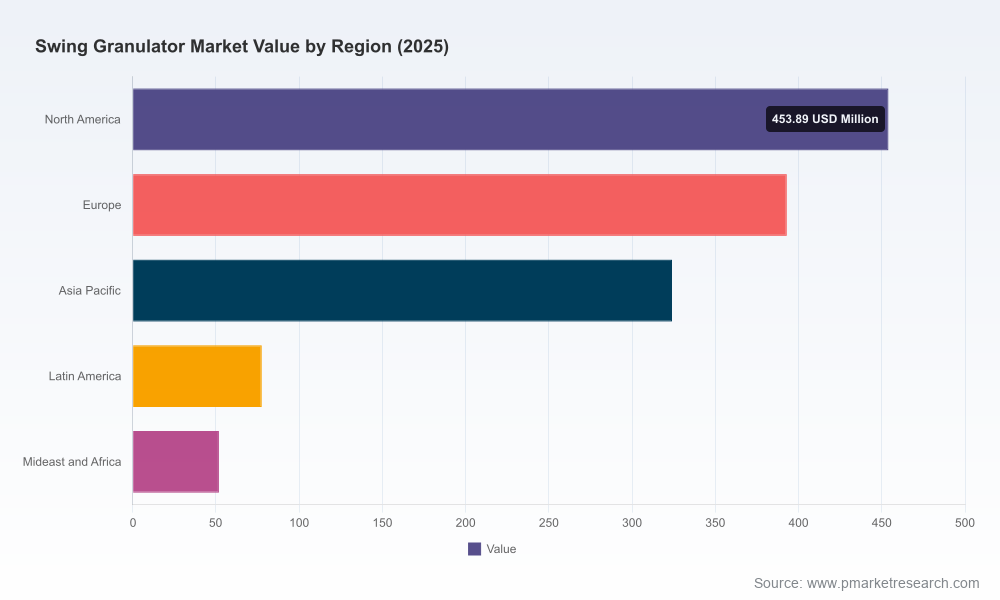

Swing Granulator Market

Why 2026 Is a Pivotal Year

Several converging forces make 2026 a decision point for manufacturers, contract packagers and capital allocators in the granulation value chain:

Swing Granulator Market

- Regulatory and quality requirements are tightening in primary end markets (notably pharmaceutical tablet production). cGMP compliance continues to drive equipment specifications—stainless contact materials (typically SS316/316L), hygienic design and validated cleanability are now baseline procurement filters.

- Input-cost volatility is re-shaping sourcing strategies. Stainless alloy surcharges for 316/316L increased in early 2026, driven by higher nickel and molybdenum costs, and U.S. hot-rolled coil prices moved above the $1,000/ton threshold amid tariff adjustments—both trends that materially affect machine BOMs and lead-times.

- Market structure remains moderately concentrated: our concentration metrics show top-three suppliers control a sizeable but non-dominant share (CR3 ~38.5%), while the top five account for just over half the market (CR5 ~52.7%). The consequence: meaningful market power resides with leading OEMs, yet substantial opportunity exists for specialized players and service-led differentiation.

What the Report Delivers — Practical, Transaction-Ready Content

For executives who must convert insight into action in 2026, the report is deliberately practical. Its core deliverables include:

Swing Granulator Market

- Transparent market sizing and forecast methodology, with scenario runs (base, upside, downside) to stress-test capital budgeting decisions.

- Procurement playbook and total cost of ownership (TCO) model, reflecting capital, installation, validation, spare parts, energy and labor under alternate input-cost regimes.

- Supplier due-diligence and scorecard templates aligned to cGMP validation checkpoints, maintenance intervals and spare-part availability.

- Operational benchmarking for throughput, yield, particle-size uniformity and downtime—enabling comparative tender evaluation beyond glossy spec sheets.

- Go-to-market and M&A playbooks: target screens for bolt-on acquisitions, integration risk matrices and quick models to estimate service-revenue uplift.

- Technology and retrofit roadmap: guidance on digital sensors, predictive maintenance and retrofits to convert legacy oscillating granulators into higher-margin service platforms.

- Regulatory impact briefings and supplier contract clauses optimized for material-surcharge pass-through, lead-time protections and quality claims.

Note: the report contains fully itemized segmentation tables (regional, by type, by application), time-series matrices and supplier revenue splits. Those detailed numerical tables are intentionally reserved for the full report and the database download on our landing page.

Competition Snapshot — Profiles and Strategic Posture

The swing granulator vendor landscape is diverse, with established OEMs concentrated in Asia and India and a mix of smaller regional specialists. Our competitive analysis highlights three strategic archetypes: (1) scale-focused OEMs offering broad product lines; (2) compliance- and service-oriented suppliers targeting pharma cGMP buyers; and (3) niche engineering specialists focused on rugged industrial applications.

- Hywell Machinery (Changzhou, China) — Strengths: breadth of YK-series lab and industrial units, stainless construction options (SS304/SS316L) and a strong export footprint. Strategic play: cost-competitive OEM with opportunity to add higher-margin validation and life-cycle services for regulated buyers.

- Lodha International LLP (Ahmedabad, India) — Strengths: cGMP-compliant oscillating granulators (LI-OG series), SS316 contact parts and designs that target pharmaceutical, herbal and food sectors. Strategic play: focused on regulated markets where documentation, material traceability and validation support command price premiums.

- JUNZHUO Machinery; Wanda Machinery; LK Mixer; Changzhou Yibu Drying Equipment; Tianhe Pharmaceutical Machinery — These suppliers collectively represent the innovation and distribution backbone for the sector, offering YK-series models, CE certifications and exhibition presence that sustain global tender pipelines. Recent activity includes Tianhe’s 2026 catalog and YK-160 product positioning, and Changzhou Yibu’s exhibiting at ACHEMA 2024—signals that OEMs continue to refresh product portfolios and pursue international validation channels.

Strategic implication: buyers will increasingly evaluate OEMs not only on machine throughput but on documentation quality, spare-part logistics and a supplier’s ability to support validation protocols. For OEMs, elevating service offerings—validation packs, digital monitoring and performance SLAs—translates into defensible margins in a cost-volatile environment.

Procurement & Manufacturing Implications for 2026

Operational and procurement leaders should consider the following actions this year:

- Hedge the capital-outlay: front-load procurement or negotiate long-lead contracts with material-surcharge clauses if your BOM is steel- or alloy-intensive. Our TCO model shows timing can materially change lifecycle costs under current commodity cycles.

- Prioritize cGMP-ready designs for products destined for pharmaceutical applications. Machines engineered with SS316/316L contact surfaces, CIP-compatible geometry and validated cleanability reduce qualification cycle time and down-market risk.

- Lock in aftermarket commitments. Service uptime is often the decisive procurement factor—shorter mean-time-to-repair and local spare stocks justify premium pricing.

- Assess retrofit pathways. Many operators can extend asset life and capacity through sensorization and motor-control upgrades that improve granule uniformity and reduce manual oversight.

Risks, Opportunities and Tactical Moves

Risk profile:

- Commodity shocks and tariffs can rapidly inflate machine costs and elongate lead times.

- Regulatory non-compliance remains a persistent fail condition for pharmaceutical suppliers—poor supplier documentation or inadequate material traceability creates commercial exposure.

- Technological obsolescence where legacy equipment cannot be economically upgraded to digital monitoring or hygienic cleaning standards.

Opportunity map:

- Service-led growth: aftermarket, spare parts and qualification services are under-monetized levers for OEM margin expansion.

- Mid-market consolidation: CR metrics show room for regional champions to scale through targeted acquisitions and by standardizing validation documentation to win larger tenders.

- Green and energy-efficient retrofits: lower energy consumption and reduced solvent losses in wet granulation offer both regulatory and cost advantages.

How PW Consulting Can Support 2026 Decisions

This briefing is a prelude to actionable engagements that PW Consulting offers. Our services include competitive supplier due-diligence, procurement negotiation support, TCO and scenario modeling, M&A advisory for strategic buyers and bespoke validation playbooks for cGMP buyers. The full Swing Granulator Market report includes downloadable datasets, supplier scorecards, and the granular segmentation tables that underpin the analyses summarized here—available through our report landing page.

For capital planning, procurement sequencing or to identify acquisition targets that fit a 2026 roll-up strategy, our tailored advisory packages convert the report’s insights into measurable outcomes—reduced procurement lead-times, improved uptime, and a clearer path to service-led margin expansion.

Conclusion — The Strategic Takeaway for 2026

As demand for precise, compliant granulation solutions grows through 2032, the 2026 planning window is a critical inflection point. Buyers must reconcile commodity-driven cost pressures with an imperative to comply with higher-quality standards. OEMs and investors should prioritize service monetization, validation-ready product sets and selective consolidation. Our report equips decision-makers with the models, templates and supplier analysis required to act decisively—while preserving the proprietary segmentation and data tables that will be essential to detailed execution. Access to the full dataset and supplier-level intelligence is available on the PW Consulting report page.

For detailed analysis of this topic, please visit the official page:Swing Granulator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com