Natural Food Colors Market Witnesses Rising Adoption in Processed Foods

Other |

2026-05-19 09:10:50

PW Consulting's latest market study on T Dodecyl Mercaptan (TDM) synthesizes quantitative projection and qualitative intelligence to equip executives for high-stakes decisions in 2026. Our analysis anchors on an industry base year of 2025, a validated compound annual growth rate (CAGR) of 4.21% for the forecast window 2026–2032, and a full market model that traces the market from 2020 through 2032. The total market is projected to expand from approximately 585.5 Million USD in 2025 to roughly 781.44 Million USD by 2032 under the baseline scenario.

T Dodecyl Mercaptan Market

Producers, buyers, and investors face a narrow decision-making window in 2026. Several dynamics—feedstock cost inflection, tightening chemical safety regulations across major jurisdictions, and selective capacity moves by specialist producers—converge to make supplier positioning, contract structuring, and grade strategy materially influential to margins and time-to-market over the next seven years. Our report identifies tactical moves that can realize disproportionate upside or prevent downside exposure if implemented before year-end 2026.

T Dodecyl Mercaptan Market

The market’s baseline trajectory reflects steady end-use demand growth driven by polymer chain-transfer applications and lubricant additive requirements. A 4.21% CAGR to 2032 implies predictable volume expansion but also underscores the need for disciplined operational and commercial strategies rather than opportunistic short-term selling. For strategic planners, this profile suggests two priorities: (1) capacity and product-mix optimization to capture incremental polymerization demand; and (2) robust procurement and hedging mechanisms against volatile feedstock inputs.

T Dodecyl Mercaptan Market

Baseline growth: Market value rises from mid-2025 levels to a materially larger market by 2032 under our central case.

Volatility vector: Feedstock price swings, particularly for propylene-derivative intermediates, create episodic margin pressure that can erode profitability if not managed through contracting or backward integration.

Concentration risk: The TDM market exhibits high supplier concentration among a small set of specialized producers—creating both supply security advantages for incumbents and risks for buyers reliant on short-term spot purchases.

Key demand drivers include continued use of TDM as a chain-transfer agent in styrenic and butadiene-based polymers and targeted requirements in lubricant additives and select fine-chemical syntheses. On the supply side, the feedstock pathway—principally the addition of hydrogen sulfide to propylene tetramer (dodecene)—links TDM costs closely to upstream naphtha, propane, and propylene markets. Notably, propylene tetramer feedstock costs rose in Q3 2025 in several producing regions, a development that is already influencing contract pricing strategies heading into 2026.

Regulatory tightening under frameworks such as REACH in Europe and TSCA in the United States is reshaping compliance cost structures for sulfur-based intermediates. Expect requirements for enhanced labeling, stricter handling protocols, and greater emissions controls. For manufacturers and downstream formulators, this translates into capital expenditure needs for containment and monitoring, higher compliance overheads, and potential lead-time implications for product registration and market access.

The market is dominated by established chemical houses and specialist producers. Key players profiled in our study include Chevron Phillips Chemical Company, Arkema S.A., ISU Chemical Co., Ltd., Sanshin Chemical Industry, and Palica Chem. Each brings distinct strategic assets:

Chevron Phillips Chemical Company (The Woodlands, Texas, USA) — a major North American capacity holder and commercial brand presence with Sulfole® 120 TDM, focused on polymer applications and large-scale supply agreements.

Arkema S.A. (Colombes, France) — integrates TDM within a broader thiochemicals portfolio, serving polymer and mineral-processing collectors, with strengths in global chemicals distribution channels.

ISU Chemical Co., Ltd. (Ulsan, South Korea) — positions on high-purity grades with strict quality control; announced a capacity expansion in May 2025 to meet rising polymer and specialty-chemical demand.

Sanshin Chemical Industry Co., Ltd. (Japan) — niche supplier specializing in ultra-high-purity TDM for polymer emulsions and fine chemicals with high-selectivity grades.

Palica Chem — focused on precise molecular-weight control in emulsion polymerization and logistical flexibility via packaging options such as 200L barrels and ISO tanks.

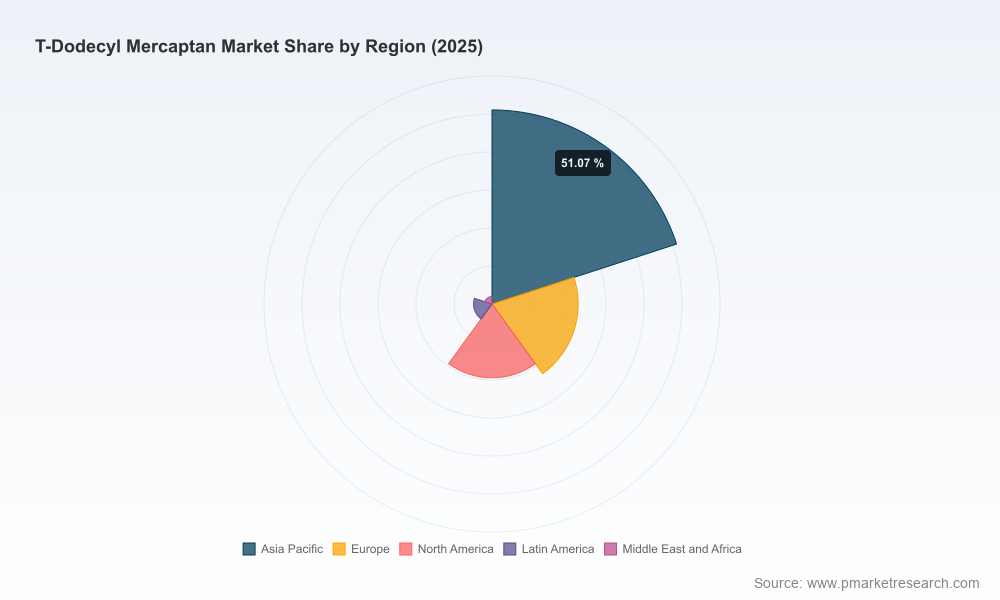

Market concentration metrics further illustrate the competitive structure: the top three suppliers account for a large share of the market, and the top five exert an even stronger aggregate control—an important consideration for contract negotiators and antitrust-conscious M&A teams.

Our full report synthesizes macro forecasting with practical tools designed for immediate operational use. Highlights include:

Scenario-based demand model (2026–2032) with sensitivities to key polymer end-use trajectories and feedstock price bands.

Supply-side tracker with capacity maps, recent plant investments, and anticipated commissioning timelines to assess physical availability risk.

Price driver analysis that quantifies the pass-through from propylene tetramer and other upstream cost inputs into TDM contract pricing under multiple contract tenors.

Regulatory impact framework mapping REACH and TSCA compliance requirements to capex and OPEX implications by production region.

Commercial playbooks — procurement strategies, preferred contract clauses, and supplier scorecards — tailored to buyers, tollers, and integrated producers.

Competitor deep dives and capability matrices allowing rapid benchmarking on purity grades, packaging, and service models.

We deliberately withhold granular regional and application-level split tables from this release to protect proprietary modeling assumptions and to guide readers to the full dataset available in the report.

Executives should translate the report's insights into a prioritized action agenda for 2026. Our headline recommendations are:

Secure multi-year off-take arrangements with tier-one suppliers to lock in volume and mitigate spot-exposure to feedstock-driven price spikes; include feedstock-indexed collars where available.

Implement dual-sourcing strategies where feasible, combining regional incumbents with specialist high-purity suppliers to balance cost and technical performance.

Accelerate product-differentiation investments for high-purity grades and tailored packaging/logistics solutions—areas where premium recognition and margin resilience are highest.

Advance regulatory preparedness programs—invest in labeling, emissions controls, and third-party testing to reduce market access friction under REACH and TSCA updates.

Stress-test supply chains for feedstock dislocations; consider strategic hedges or upstream partnerships for propylene tetramer to reduce feedstock margin volatility.

For potential acquirers: prioritize targets that offer unique high-purity assets, strong regional distribution, or integrated feedstock positions to accelerate scale and margin capture.

Procurement leaders seeking to redesign supply agreements and implement hedging for 2026–2028.

Commercial teams that must set price trajectories and negotiate with concentrated suppliers.

R&D and technical managers evaluating grade and formulation strategies to capture premium segments.

Corporate development teams prioritizing M&A or brownfield expansion targets within a concentrated competitive landscape.

PW Consulting recommends a phased decision framework for 2026: (1) rapid diagnostic (Q1) to identify exposure and supplier concentration; (2) tactical mitigation (Q2–Q3) such as contracting or spot inventory buys ahead of seasonal feedstock pressure; (3) strategic moves (Q4) including capital allocation or M&A to secure desired capabilities for the 2027–2030 horizon.

This release is designed as a strategic preview: it highlights validated macro trajectories, competitive dynamics, and operational levers that will matter in 2026, while intentionally withholding proprietary segment-level datapoints and detailed tables that are included in the full report package. For teams preparing budgets, negotiating supplier agreements, or evaluating strategic investments in 2026, access to the complete dataset and modelling logic will materially improve decision quality.

Contact PW Consulting to obtain the full T Dodecyl Mercaptan Market report, download sample model outputs, or commission a bespoke briefing tailored to your company’s position in the value chain.

For detailed analysis of this topic, please visit the official page:T Dodecyl Mercaptan Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com