Commercial Food Dehydrators Market: Strategic Imperatives for 2026 — PW Consulting Executive Brief

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive preview of our latest market study on Commercial Food Dehydrators. This briefing highlights the practical intelligence senior leaders will need to steer investment, product and operational decisions in 2026 — while preserving the granular segment-level intelligence for the full report.

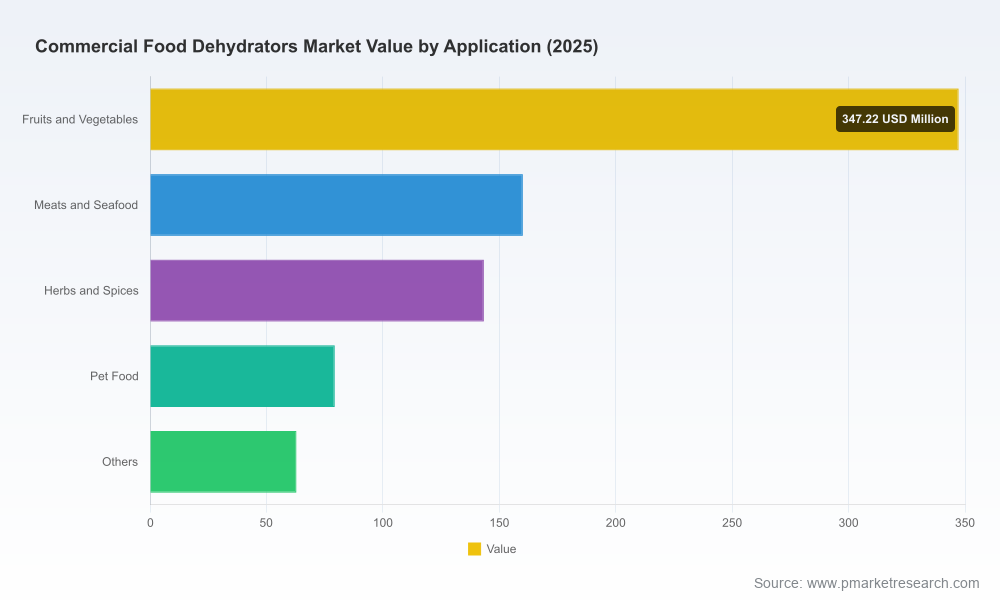

Commercial Food Dehydrators Market

Executive snapshot

- The commercial food dehydrators market reached approximately USD 792.7 Million in our 2025 base year.

- Under our base-case modeling the market is expected to expand at a compound annual growth rate (CAGR) of 5.8% over the 2026–2032 forecast window, moving toward roughly USD 1.18 billion by 2032.

- Market concentration is moderate: the top three players account for under one-third of revenue, and the top five under half — indicating room for consolidation and differentiated growth strategies.

Why this matters for 2026 decision cycles

- Capital allocation: Manufacturers and investors must reconcile rising product demand with increasing input and operating costs. Our models quantify how energy and stainless-steel cost dynamics compress margins across typical commercial SKUs and where premiumization still preserves price realization.

- Product strategy: Technology choices (e.g., heat pumps, horizontal vs. vertical airflow designs, digital controls and HACCP-ready features) materially affect both unit economics and end-user total cost of ownership. The right technology selection determines whether a new model competes on price, efficiency, or serviceable performance.

- Regulatory and food-safety compliance: USDA and FDA guidance increasingly governs pre-processing, cooking and moisture monitoring practices. Compliance-ready product features are not optional for commercial channels — they are a commercial differentiator.

Market dynamics shaping near-term strategy

- Cost inflation in energy and raw materials: Electricity costs in many key markets have increased significantly since 2020, and commercial units commonly consume between 15–30 kWh per batch. Concurrent volatility in stainless-steel pricing has implications for BOM composition, lead-times, and margin planning for premium stainless models.

- Technology transition: Heat-pump dehydration and integrated digital process controls are shifting the value equation from pure throughput to energy efficiency and batch traceability. Manufacturers that productize energy performance and validation features capture both OEM and end-user willingness to pay.

- Channel expansion and product adjacencies: Growth in decentralized food processing — from co-packer services to specialty snack producers and pet food verticals — is broadening demand beyond traditional institutional buyers. New entrants and adjacent equipment suppliers view dehydrators as leverage into broader processing ecosystems.

- Regulatory pressure and food safety practices: Agencies such as USDA and FDA emphasize pre-cook thresholds and moisture control for pathogens. Products that facilitate validated cook-and-dry workflows reduce operator risk and liability exposure, accelerating adoption in regulated facilities.

Competitive landscape — what to watch

The market contains a mix of specialized legacy brands, small-batch domestic makers, and industrial-scale OEMs. Our company-level benchmarking evaluates product breadth, proprietary technologies, warranty and service models, supply-chain exposure, and go-to-market channels. Notable players in our coverage include:

Commercial Food Dehydrators Market

- Excalibur Dehydrator (Sacramento, CA) — Known for patented Hyperwave technology and Parallex horizontal airflow solutions that aim to optimize uniform drying for food processors.

- NESCO (Metal Ware Corporation) (Two Rivers, WI) — A broad-range supplier with commercial and “Snackmaster” series, emphasizing variable temperature control and scalable models for higher-volume users.

- Tribest Corporation (California) — Focused on advanced sequential temperature-timer (TST) technologies and stainless construction, with recent new-tray offerings to improve throughput flexibility.

- Commercial Dehydrators America (Alvarado, TX) — A premium-focused manufacturer offering large-tray counts and multi-year commercial warranties, targeting industrial foodservice and co-packers.

- Advanced Food Dehydrators (Methuen, MA) — Batch dehydrator specialists with features tailored to jerky makers and operators needing lethality cook cycles for food safety validation.

- Nyle Systems, LLC (Brewer, ME) — Heat-pump and industrial dehydration solutions that emphasize energy efficiency and reduced thermal load.

- LEM Products (Ohio) — Strong in meat-processing applications, offering heavy-duty stainless units favored by jerky producers.

- IKE Group (Guangdong IKE Industrial Co., Ltd.) (Foshan, China) — A large manufacturer leveraging heat-pump designs and competitive manufacturing scale for export markets.

Recent product activity validates our thesis of technology-driven differentiation: Tribest’s 2025 Sedona Express and Excalibur’s 2025 Performance Digital series both introduced enhanced tray counts, digital controls and airflow innovations. These launches illustrate how vendors are converging on features that address efficiency, process validation and operator ergonomics.

Commercial Food Dehydrators Market

What the PW Consulting report delivers — practical, operational tools

This study is built as a decision-support toolkit, not just a descriptive narrative. For commercial leaders evaluating investments in 2026, the report provides:

- Robust market-sizing and scenario forecasts across multiple adoption curves, stress-tested for energy and raw-material volatility.

- CapEx/Opex templates and lifecycle TCO calculators that let procurement teams model alternative technology choices (heat pump vs. resistive heating; horizontal vs. vertical airflow) with customizable electricity and stainless-steel price inputs.

- Vendor benchmarking scorecards covering performance, warranty, after-sales service, regulatory readiness and supply-chain risk exposures.

- Regulatory compliance checklist and process-validation playbook aligned to USDA and FDA expectations for meat and poultry processing.

- Commercial go-to-market playbooks tailored to three buyer archetypes — industrial co-packers, specialty snack manufacturers, and meat/jerky processors — with channel strategies, pricing guidance and sample product roadmaps.

- M&A and partnership screening frameworks to identify attractive consolidation targets and technology licensing opportunities, informed by our concentration and fragmentation analysis.

Actionable recommendations for 2026

- Prioritize R&D and product roadmaps around energy efficiency and process validation. Units that materially lower energy per batch and integrate validated cook/dry cycles will command premium positioning and reduce total cost of ownership for buyers.

- Lock in supply-chain levers for stainless and key components. Given raw-material volatility, strategic supplier agreements or vertical integration options for high-grade materials will protect margin and delivery promises.

- Commercialize compliance features. Embed moisture and temperature logging, easy integration with HACCP systems, and user-guided process recipes that reduce operator variability and regulatory risk.

- Segment go-to-market by buyer economics, not by product alone. Tailor warranty, service and finance options for co-packers versus small-batch artisanal producers — these buyers value different risk transfer mechanisms.

- Consider selective consolidation or technology licensing. Moderate top-end concentration suggests meaningful upside for well-capitalized players to acquire scale in adjacent niches or consolidate aftermarket services.

Where this preview leaves you — and the value of the full report

This executive brief surfaces the strategic dimensions and operational levers that will define success in the commercial food dehydrators market through 2026. The full PW Consulting report contains the proprietary models, segment-level demand curves, regional and application splits, price elasticity matrices, and granular vendor scorecards that underpin the recommendations above. In keeping with our preview (“trailer”) approach, we intentionally withhold the detailed tables and downloadable tools — they are available through the report portal for clients and subscribers.

How to use the intelligence now

- Download the full dataset to run alternate energy-price and stainless-cost scenarios against your product roadmap.

- Use the TCO templates to price new SKUs for both utility and premium buyer segments.

- Engage our M&A screening team to fast-track diligence on acquisition targets that accelerate entry into priority channels.

For procurement, product or corporate development leaders preparing 2026 budgets: treat energy-efficiency and compliance capabilities as the top two determinants of product success. Market growth is healthy and durable, but margin pressure from input-cost volatility and higher energy tariffs will reward providers who convert technical innovation into demonstrable operating savings and validated food-safety outcomes.

Contact PW Consulting to request access to the full Commercial Food Dehydrators Market report, model license, or a custom briefing tailored to your company’s strategic questions.

For detailed analysis of this topic, please visit the official page:Commercial Food Dehydrators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com