Non-Invasive Intracranial Pressure Monitoring Devices: A Strategic Briefing for 2026 Decision-Making

Executive snapshot

The non-invasive intracranial pressure (ICP) monitoring market has moved decisively from a niche adjunct to an emerging standard of care in selected neurocritical and acute-care pathways. Our updated market baseline (2025) and forward-looking forecast (2026–2032) indicate sustained, double-digit momentum in developer activity, regulatory engagements and clinical adoption catalysts — underpinned by a 7.85% compound annual growth rate across the forecast window. For corporate leaders, investors and health-system strategists planning for 2026, this report provides an operationally actionable, risk-calibrated blueprint to align product pipelines, clinical validation programs, regulatory strategies and commercial go‑to‑market plans.

Non Invasive Intracranial Pressure Monitoring Device Market

Why 2026 is an inflection year

- Regulatory momentum has accelerated: Breakthrough device designations and multiple 510(k) clearances, together with professional consensus statements, are reducing adoption friction and creating a clearer pathway for reimbursement conversations.

- Clinical validation is maturing: Large-scale clinical publications and multicenter consensus (notably recent multimodal recommendations for traumatic brain injury) are creating standards by which vendors will be benchmarked.

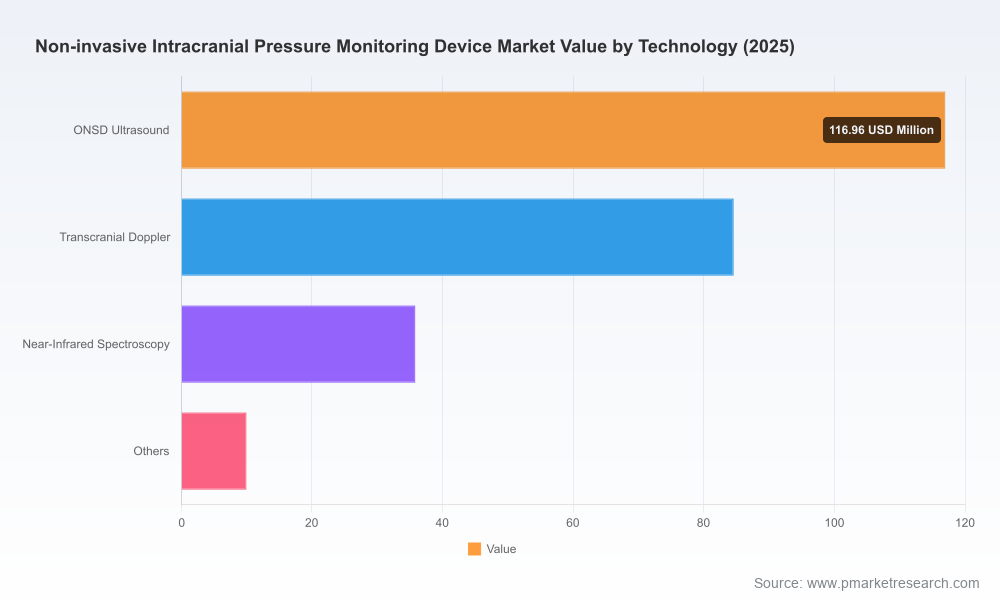

- Technology diversification: Ultrasound-, optics-, and skull‑expansion–based modalities are now cross‑validated against hemodynamic proxies, enabling developers to pursue differentiated claims (variation monitoring, absolute ICP estimation, long‑term telemetry).

- Commercial readiness: A cohort of established neurotechnology and medical-device incumbents is moving to bundle non‑invasive ICP capabilities into broader neurocritical-care portfolios, changing competitive dynamics and channel strategies.

Market trajectory: size, growth and concentration

PW Consulting’s model shows the market expanding from a defined mid‑market baseline in 2025 to materially larger scale by the end of the forecast window. This expansion is driven by widening clinical use-cases, amplified regulatory clarity and growing reimbursement receptivity for practical, bedside-friendly non‑invasive options. Market concentration remains moderate: the three largest firms account for a meaningful share of current revenues, and the five largest players command a clear majority — a profile that creates both opportunities for focused challengers and strategic risks for dispersed innovators.

Non Invasive Intracranial Pressure Monitoring Device Market

What the report delivers — practical content for 2026 actions

This study is structured for executives who need to translate market intelligence into executable agendas. It contains:

Non Invasive Intracranial Pressure Monitoring Device Market

- Market sizing and growth scenarios (base year 2025; forecast 2026–2032) incorporating sensitivity to reimbursement, regulatory timelines and clinical adoption velocity.

- Clinical validation matrix that maps device modalities against evidence tiers, endpoints (ICP variation, absolute estimation, long‑term trends), and recommended trial designs to achieve regulatory and payer objectives.

- Regulatory playbooks for jurisdictions with the most near-term commercial opportunity, including pre-submission strategies, comparators and data endpoints aligned to current standards.

- Reimbursement pathway templates: coding, evidence thresholds, and payer engagement timelines to accelerate coverage decisions and hospital procurement.

- Go‑to‑market frameworks for device vendors, new entrants and incumbent medtech firms—covering channel models, clinical champions, hospital economics and pricing benchmarks (scenario-based).

- Competitive benchmarking that profiles vendor technology types, clinical evidence, regulatory status, partnership footprints and commercialization maturity — with a focus on actionable gaps and white‑space opportunities.

- M&A and partnership scorecards identifying strategic targets, integration risks, and potential synergies for scale, distribution and clinical evidence acceleration.

Competitive landscape — tactical takeaways

The competitive set includes a mix of pure-play startups with novel sensing approaches and larger device manufacturers integrating non‑invasive ICP capabilities into broader neuromonitoring portfolios. Key tactical observations:

- Innovators with focused clinical evidence are leapfrogging on credibility. For example, a cranial expansion sensor system recently received regulatory clearance in a major market and published a large comparative study demonstrating strong performance on specific clinical endpoints. This combination of clearance plus peer‑reviewed evidence materially shortens sales cycles in critical‑care settings.

- Emerging ML‑driven forehead/photoplethysmography approaches are promising for portable, pre-hospital and emergency-department triage applications, but they commonly require larger, prospective validation cohorts before achieving broad clinical trust.

- Ultrasound-based systems maintain a strong position for acute detection of elevated ICP proxies, and transorbital/optic‑nerve sheath approaches are attractive where rapid, bedside assessments are needed; however, operator dependence and training requirements remain adoption bottlenecks unless mitigated by automation and workflow integration.

- Established neurotechnology vendors bring channel access and purchasing leverage, enabling bundling strategies that can accelerate hospital adoption—challengers must therefore build either clinical superiority or compelling economic cases to displace incumbents.

Regulatory and clinical dynamics to watch

- Standards and accuracy thresholds: Existing device standards and professional guidelines set specific accuracy expectations in clinical ranges; early validation data indicate variability among modalities, which vendors must address through targeted study design and model calibration.

- Consensus guidance on multimodal monitoring: Recent expert-driven recommendations favor multimodal non‑invasive approaches (combining at least two techniques) when invasive monitoring is unavailable. This raises the bar for single‑modality vendors but opens partnership and integration opportunities for multimodal solutions.

- Breakthrough pathways and telemetric long‑term monitoring: Regulatory innovations and breakthrough designations for telemetric systems indicate a parallel growth vector in chronic hydrocephalus and post‑operative monitoring that can alter revenue mix and clinical adoption curves.

Commercial and reimbursement strategy highlights

Our scenario modeling shows that reimbursement posture and hospital economics materially influence purchase decisions. For 2026, firms should prioritize:

- Evidence packages aligned to payer needs — short, high‑impact studies that demonstrate how non‑invasive monitoring reduces invasive procedures, length of stay or transfers to higher acuity units.

- Value-based pilots with integrated health systems to create local case‑studies and economic models that can be replicated regionally.

- Clinical education and workflow integration: delivering training, decision‑support and interoperability with electronic medical records reduces operational friction and accelerates adoption.

Investment and M&A implications

Investors and corporate strategists face three pragmatic choices in 2026:

- Buy: Acquire focused clinical‑validation assets to accelerate market access and obtain near‑term revenue streams — particularly attractive where buyers can immediately integrate technology into existing neurocritical portfolios.

- Build: Invest in rigorous, prospectively designed studies and regulatory conversion to obtain differentiated labeling claims; ideal for firms with clinical and reimbursement capabilities.

- Partner: License algorithms, co‑develop multimodal sensor fusion, or enter distribution agreements to marry innovative sensing with established commercial channels.

Risk map and mitigation

- Clinical risk: Inconsistent performance across patient subpopulations—mitigate with stratified clinical programs and transparent failure-mode analyses.

- Regulatory risk: Divergent regional evidence expectations—mitigate by early regulatory engagement and harmonized trial protocols.

- Commercial risk: Channel displacement by incumbents—mitigate with specialty KOL adoption, differentiated service offerings and outcome-based pilots.

How PW Consulting’s report supports 2026 boardrooms

PW Consulting’s market study is designed as a decision-making toolkit rather than an academic compendium. It combines market-size projection (anchored to a 2025 baseline and a 7.85% CAGR for the forecast period), competitor profiles and a playbook of validated operational tactics. The report translates clinical science into business tasks: regulatory milestones, trial designs, payer evidence, pricing scenarios and practical commercialization checklists. For executives preparing 2026 budgets, portfolio roadmaps or M&A mandates, the study provides prioritized actions and time-bound milestones to de‑risk investment and accelerate value realization.

Next steps: what to do now

- For product teams: Align clinical study endpoints to regulatory and payer expectations now; consider multicenter trials that support both labeling and cost‑effectiveness narratives.

- For commercial leaders: Pilot value‑based contracts with early adopter hospitals and embed clinical champions into rollout plans.

- For corporate development: Map acquisition targets and partnership candidates against the report’s strategic scorecards to identify fast-follow integration plays.

Access full intelligence

This briefing is an executive preview of the comprehensive PW Consulting report, which contains detailed scenario models, modality‑by‑modality evidence matrices, and granular go‑to‑market playbooks. Due to the strategic sensitivity of certain segmentation and financial detail, core data tables and company-level revenue splits are available exclusively in the full report. Contact PW Consulting to obtain the complete study and a tailored briefing for your 2026 strategy session.

For detailed analysis of this topic, please visit the official page:Non Invasive Intracranial Pressure Monitoring Device Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com