How Music Libraries Power Modern Audio Experiences in Dallas

Other |

2026-05-28 10:06:50

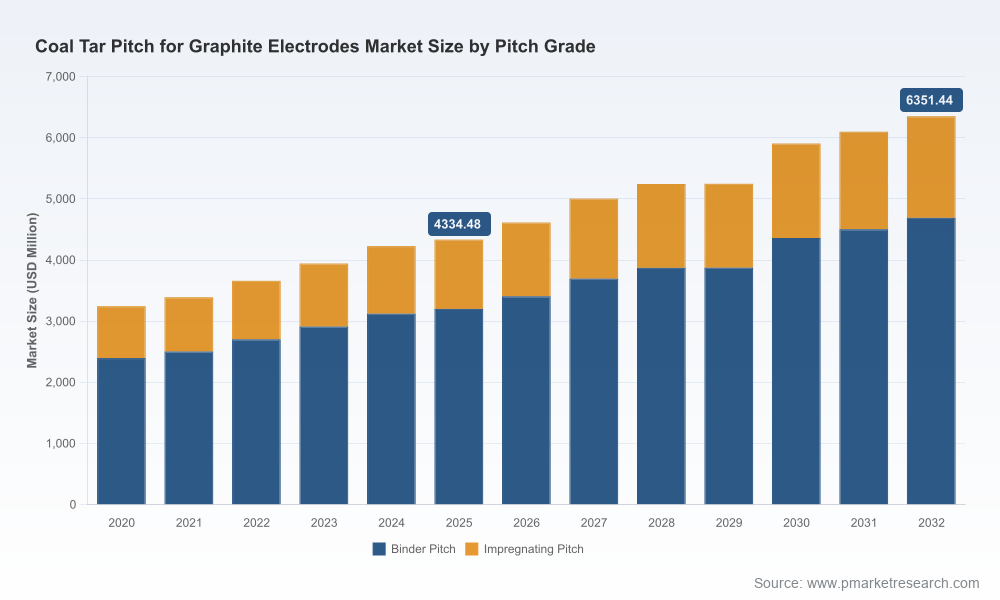

PW Consulting’s latest market research on Coal Tar Pitch for Graphite Electrodes is designed as an executive-grade decision aid for leadership teams planning capital allocation, supply-chain repositioning, and commercial strategy in 2026. The market has followed a steady expansion curve through the early 2020s and—based on our modelling—moves from a global market size of approximately USD 4,334.5 Million in 2025 to an estimated USD 6,351.4 Million by 2032, corresponding to a compounded annual growth rate (CAGR) of roughly 5.61% over the forecast horizon. These headline figures frame the investment context: demand trajectories are healthy, but value capture will be defined by supply reliability, product-grade specialization, and regulatory compliance.

Coal Tar Pitch For Graphite Electrodes Market

Signal clarity in an expanding market — Boards and investment committees need to understand where incremental tonnes and margin uplift will come from as overall market size increases. Our report translates macro growth into three strategic decision paths (capacity expansion, premiumization, and supply diversification) that are actionable in 2026.

Coal Tar Pitch For Graphite Electrodes Market

Timing for capital deployment — With a visible multi-year growth runway, the window to secure feedstock, retrofit emission controls, or greenfield new-builds has a finite lead time. The report models payback scenarios under different price and regulation assumptions to prioritise capex tranches for 2026 approvals.

Coal Tar Pitch For Graphite Electrodes Market

Regulatory and trade risk incorporated — Recent and ongoing regulatory moves (EU Industrial Emissions Directive updates, US Clean Air Act implications for coal tar pitch handling, and China’s export licensing on related graphite materials) materially shift required compliance spend. The research quantifies likely compliance cost bands and identifies low-friction mitigation strategies for 2026 execution.

Our longitudinal dataset (2020–2025) and forecast (2026–2032) reveal a market that has recovered and rebalanced after pandemic-era dislocations and is now growing on the back of increased electric-arc furnace (EAF) steelmaking and aluminium anode demand. The growth profile is not linear—there are step changes driven by episodic capacity investments and regulatory-driven retrofits. For 2026 decision-makers, the salient implications are twofold: first, aggregate demand growth affords opportunities to scale production; second, differentiation — whether through specialty impregnation grades or low-PAH offerings — will deliver outsized margin improvement compared with pure volume plays.

Raw material dynamics are a near-term operational factor. Coal tar feedstock prices firmed toward the end of 2025 (reported indicatives around USD 463–465/MT in major markets), tightening margins for low-value producers and pressuring players without feedstock hedges or integrated upstream positions. Our scenario work shows that a 10–15% movement in feedstock cost can swing EBITDA materially for commodity-grade suppliers, whereas higher-purity or specialty product lines exhibit lower sensitivity.

Compliance is now a strategic differentiator. EU IED obligations, US EPA constraints under the Clean Air Act, and tighter controls over PAHs increase the cost of doing business in core markets. The report provides a compliance-impact matrix that maps likely capital, OPEX, and timeline implications for different production vintages and geographies, enabling CFOs to budget for 2026–2028 retrofits without derailing growth plans.

In tandem, customer-facing ESG expectations (from major graphite electrode consumers) create a two-speed market: buyers increasingly prefer suppliers with verified low-emission footprints and documented PAH controls. For executives, this converts compliance spend from a regulatory checkbox into a commercial investment that can unlock premium contracts and long-term offtake agreements.

The market remains moderately concentrated (CR3 ~38.5%; CR5 ~54.1%), indicating room for regional champions and a handful of global players to shape supply conditions. Our competitive framework evaluates producers on three vectors: feedstock position and integration, product-grade breadth (binder vs. impregnation), and regulatory/ESG standing. Key strategic observations include:

Integrated incumbents with upstream raw-material access or diversified carbon portfolios are best positioned to protect margins during feedstock volatility and to support large, long-term EAF customers.

Specialist producers with approvals from global graphite manufacturers and proprietary high-purity grades capture premium pockets and face lower direct price competition—an attractive path for mid-sized players looking to avoid capacity-centric price wars.

Regional distributors and service-oriented suppliers play a critical role in shortening lead times and mitigating logistics risks for end-users, a transactional advantage during volatile periods.

Without disclosing dataset-level splits in this public summary, the report includes company scorecards that translate these general observations into decision-ready intelligence for frontline teams. Among the recent market movements we track: a major capacity expansion commencement in India by a global player in mid-2025 and the first-time export of liquid coal tar pitch by a leading Indian manufacturer to the Middle East in late 2025—both developments that underscore the shifting balance between local supply build-out and export-led market strategies.

We designed the report as a pragmatic playbook, not just a descriptive survey. Deliverables include:

Actionable demand scenarios and a modular forecasting engine calibrated to EAF adoption, aluminium anode cycles, and substitution risk — enabling rapid “what-if” stress tests for procurement and commercial teams.

Supply-risk mapping and a supplier-qualification rubric that incorporates feedstock access, production vintages, emission controls, and logistics resilience. The rubric is built for procurement to run supplier audits and scorecards in 2026 supplier tenders.

Capex decision templates with IRR, NPV, and payback sensitivity bands reflecting different compliance scenarios (baseline regulation, accelerated-stringency, and low-regret retrofit options) to inform board-level approvals.

M&A and partnership screening tools—filters for target identification based on technology, market access, and regulatory exposure—along with an integration checklist that shortens post-merger value capture timelines.

Commercial playbooks for negotiating offtakes and long-term contracts, including standardised clauses for quality, liability, and force majeure tied to trade controls or export licensing turbulence.

Compliance and ESG implementation roadmaps with recommended timelines and CAPEX prioritisation for environmental controls, enabling management to phase investments to match 2026 budget cycles.

We recommend three immediate uses of this report for 2026 planning cycles:

Procurement: Run a supplier consolidation pilot using the supplier-qualification rubric to reduce single-source exposure and secure two-tiered back-up sourcing for critical grades within 6–9 months.

Capital planning: Use the capex decision templates to prioritise one “low-regret” retrofit and one strategic expansion so that board approvals and permitting can be synchronised to optimise financing terms in 2026.

Commercial & Product: Launch a specialty-grade product roadmap pilot with a selected electrode customer to validate premium pricing and co-development timelines; the report contains negotiation playbooks and sample technical acceptance criteria to accelerate trials.

Consistent with the “prequel” intent of this release, this commentary surfaces the analytical frame, strategic implications, and top-line market trajectory while deliberately omitting granular subsegment percentages and tranche-level revenue tables. The full report contains the complete datasets, regional and application-level splits, and the interactive forecast model that corporate teams use for direct planning and tendering. Access to the full package also unlocks the supplier scorecards and the downloadable capex templates referenced above.

Executives preparing for 2026 should regard the coal tar pitch market for graphite electrodes as a growth market with clear differentiation opportunities. The strategic questions that leadership must answer this year are simple in form but complex in execution: will we compete on scale, on specialty, or on resilience? The correct answer may be a hybrid—selective capacity investments hedged by targeted premiumization and underpinned by compliance-first capex sequencing. Our report provides the decision tools, scenario analyses, and operational playbooks to convert that strategy into measurable 2026 outcomes.

For strategy teams, supply-chain leaders, and investors preparing board-ready proposals in 2026, PW Consulting’s full Coal Tar Pitch for Graphite Electrodes Market report is designed to be the operational backbone of those decisions. The public preview above highlights the core takeaways and strategic levers; the full report delivers the granular models and company-level intelligence necessary to execute.

For detailed analysis of this topic, please visit the official page:Coal Tar Pitch For Graphite Electrodes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com