Waterproof Industrial PCs Market to Reach US$3.63 Billion by 2032 at 8.8% CAGR, Outlook 2026-2034

Other |

2026-06-09 08:00:04

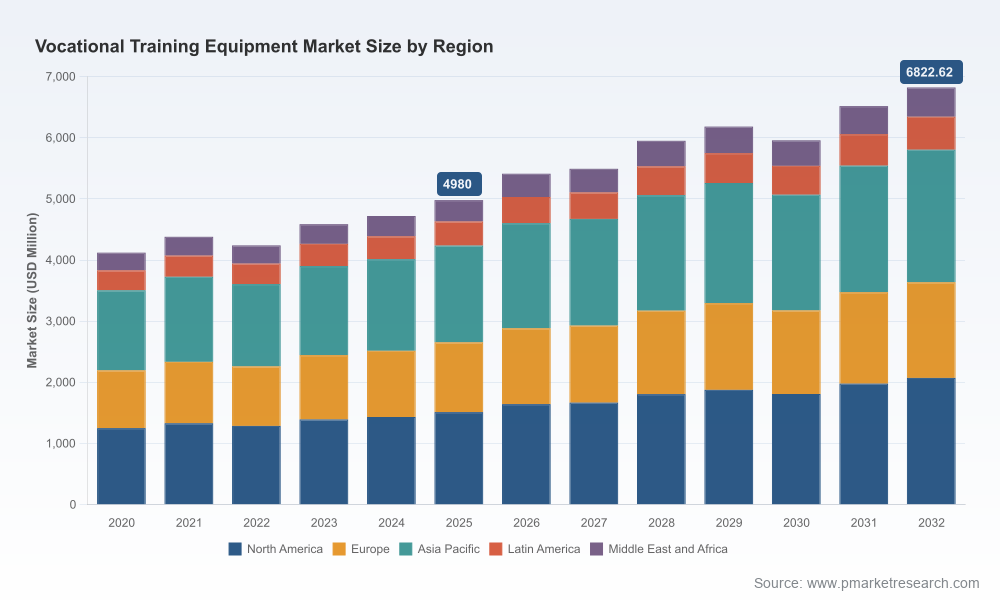

PW Consulting today publishes an executive preview of its forthcoming Vocational Training Equipment Market report — a practitioner-focused briefing designed to shape capital allocation, procurement strategies, and market-entry plans for 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study quantifies a market that expanded from the low‑billions in 2020 to roughly USD 5.0 billion in 2025 and is projected to grow at a steady 4.6% CAGR through the forecast period, crossing well into the mid‑single‑digit billions by the early 2030s. This preview highlights the strategic takeaways that matter to executives today while preserving the granular segmentation and vendor metrics exclusively for report subscribers.

Vocational Training Equipment Market

Timing and momentum — 2026 is a pivot year: public and private investments in technical and vocational education are accelerating, even as cost pressures and supply‑side frictions force buyers to rethink sourcing and lifecycle costs. Our study translates market momentum into operational signals — where demand is accelerating, where modularization and digitalization are winning, and where procurement teams must adapt tender language and TCO models.

Vocational Training Equipment Market

Actionable risk intelligence — beyond headline growth, the report maps the principal risk vectors that will shape vendor selection and capital planning in 2026: tariff regimes, raw‑material inflation, safety standard updates, and OEM partnerships that alter supplier bargaining power.

Vocational Training Equipment Market

Vendor playbooks for buyers and investors — we convert competitive analysis into clear, tactical implications: selection criteria for partner vendors, service and warranty standards, retrofit vs full‑replacement thresholds, and financing structures tailored to institutional buyers and public TVET programs.

Confluence of digital and hands‑on: Buyers are demanding integrated learning paths that combine traditional bench trainers and hand tools with simulation, automation, and digital assessment. Solutions that enable blended learning (lab + simulator + LMS integration) are rapidly becoming procurement must‑haves.

Service economics trump sticker price: With tighter capital discipline, institutions prefer equipment that minimizes downtime and maximizes modular upgradeability. Service, spare parts availability, and remote diagnostic capabilities now materially influence purchasing decisions and lifetime ROI.

Policy and materials: Trade policy shifts and raw‑material volatility are compressing manufacturer margins and creating price pass‑through risks for buyers. Buyers and vendors need contingency playbooks to manage sudden cost inflation and tariff changes, including localized sourcing and material substitution strategies.

Safety and compliance as competitive differentiator: New and updated standards for stationary training equipment are raising the bar for product certification and lab accreditation. Vendors who embed compliance, testing documentation, and simpler audit trails into their offers will unlock institutional preference.

Robust market model: A market sizing model calibrated to 2020–2025 historicals and stress‑tested across macroeconomic scenarios for 2026–2032, with mid, upside and downside pathways and clearly documented assumptions.

Segment playbooks: Tactical guidance for prioritizing product lines, customer segments, and procurement levers — including distributor network strategies, aftermarket service models, and training partnerships for curriculum alignment.

Vendor scorecards and sourcing matrix: Comparative assessment of leading vendors across product breadth, digital readiness, price positioning, global footprint, and service capabilities. Scorecards are designed for direct insertion into RFP evaluation templates.

CapEx and TCO tools: Ready‑to‑use templates and quick calculators that translate equipment specs into lifetime costs, break‑even horizons for retrofits, and sensitivity tables around tariff and raw‑material shocks.

Procurement & policy playbook: Standardized RFP language, warranty and service‑level templates, compliance checklists referencing the latest industry safety standards, and recommendations to de‑risk cross‑border acquisitions.

Case studies & deployment blueprints: Field-validated lessons from recent institutional rollouts covering training center design, instructor upskilling, and student assessment approaches tied to employability outcomes.

Our competitive analysis synthesizes company profiles, product roadmaps, and partnership activity to delineate three pragmatic vendor archetypes that will shape 2026 procurement: global systems integrators and OEMs focused on industrial automation and robotics; specialist didactic manufacturers with deep curriculum alignment; and regional cost‑competitive producers catering to price‑sensitive institutional buyers.

Global automation OEMs and integrators (example players): These firms leverage their automation portfolios to bundle hardware, simulation environments, and certified curricula — an increasingly attractive proposition for advanced manufacturing programs. Their strengths are in brand, scale, and close industry links, which also open pathways to long‑term service contracts and OEM certified learning outcomes.

Didactic specialists (example players): Vendors with deep pedagogical expertise and modular lab systems continue to lead in markets that prioritize curriculum alignment and hands‑on learning fidelity. Their differentiation is measured in instructor resources, assessment tools, and turnkey lab designs for institutional rollout.

Regional manufacturers and exporters (example players): Competitive on price and distribution, these suppliers are improving quality and aftersales, increasingly forming partnerships with local training bodies. Their role will expand where cost and lead times are decisive factors.

Market concentration metrics indicate a moderate consolidation trend: the top three players capture a meaningful share of the addressable market while the top five approaches a majority position. This dynamic favors strategic alliances and selective M&A for firms seeking rapid capability or geographic expansion.

Strategic partnerships between automation OEMs and specialist measurement or tool providers are accelerating integrated learning offers. These alliances shorten buyer evaluation cycles but raise integration expectations for smaller vendors.

Flagship software launches from major automation suppliers are shifting value from pure hardware to subscription‑based training ecosystems. Institutions must now evaluate software roadmaps, data portability, and vendor lock‑in risks as part of procurement.

Large-scale national training initiatives underscore the scale opportunity, but also increase scrutiny on outcomes and equipment standardization. Vendors that can demonstrate measurable employability impact will gain priority in public tenders.

Tariff and trade policy volatility: Elevated import duties on metal products and derivative tariffs implemented in recent policy cycles have materially increased the direct landed cost of metal‑intensive training rigs. Buyers and vendors must bake tariff scenarios into procurement models and consider local assembly or alternative material strategies.

Input cost inflation: Steel and commodity price swings have increased unpredictability in manufacturing costs, compressing vendor margins and leading to more frequent price adjustments. Long‑dated fixed price contracts should include indexed adjustments and clear dispute mechanisms.

Standards and compliance: The emergence of updated safety and test standards for stationary training equipment elevates certification burden. Procurers should require compliance documentation up front and prioritize vendors with pre‑tested modules to avoid retrofit costs.

Adopt a modular procurement approach: Prioritize modular lab architectures and upgradeable simulators to extend useful life and protect against obsolescence.

Substitute CapEx with outcome‑linked financing where possible: Structured financing or service contracts that tie payments to uptime and learning outcomes reduce upfront capital strain for institutions.

Formalize supplier risk metrics: Include tariff exposure, local content, spare parts lead time, and software update cadence as weighted criteria in vendor scorecards.

Invest in instructor enablement and digital assessment: Training equipment without trained instructors and validated assessment frameworks yields low ROI — budget at least 10–15% of equipment spend for sustained instructor and curriculum support.

Negotiate for data portability and standards alignment: Insist on open LMS connectors and documentation aligned to recognized safety/quality standards to avoid lock‑in and simplify accreditation.

Our full report is designed as an execution toolkit for decision‑makers: it contains downloadable TCO and scenario tools, vendor scorecards ready for insertion into RFPs, and granular segmentation that supports market prioritization by region, product type, and application. To preserve the commercial value of that granularity and to comply with client confidentiality, this preview intentionally omits the detailed breakdowns and numeric splits; subscribers receive the complete datasets, source tables, and model access.

For procurement leaders, investors, and strategy teams preparing budgets and go‑to‑market plans for 2026, PW Consulting’s Vocational Training Equipment Market report converts market visibility into operational playbooks. To access the full dataset, vendor assessments, and customizable financial models, visit the PW Consulting report page or contact our research team for a briefing.

For detailed analysis of this topic, please visit the official page:Vocational Training Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com