Global AI Plush Toys Market Growing at 52.0% CAGR Through 2032

Other |

2026-06-24 11:46:30

As offshore wind developers and their supply chains prepare for a decisive wave of project sanctioning in 2026, PW Consulting releases a compact strategic preview of our full Gravity Anchors For Offshore Wind Market report. This briefing sets out the implications of the market’s rapid expansion for board-level decisions, capital allocation and industrial strategy — and explains why a targeted intelligence playbook will be essential for any player seeking to capture value from gravity-anchor solutions over the next investment cycle.

Gravity Anchors For Offshore Wind Market

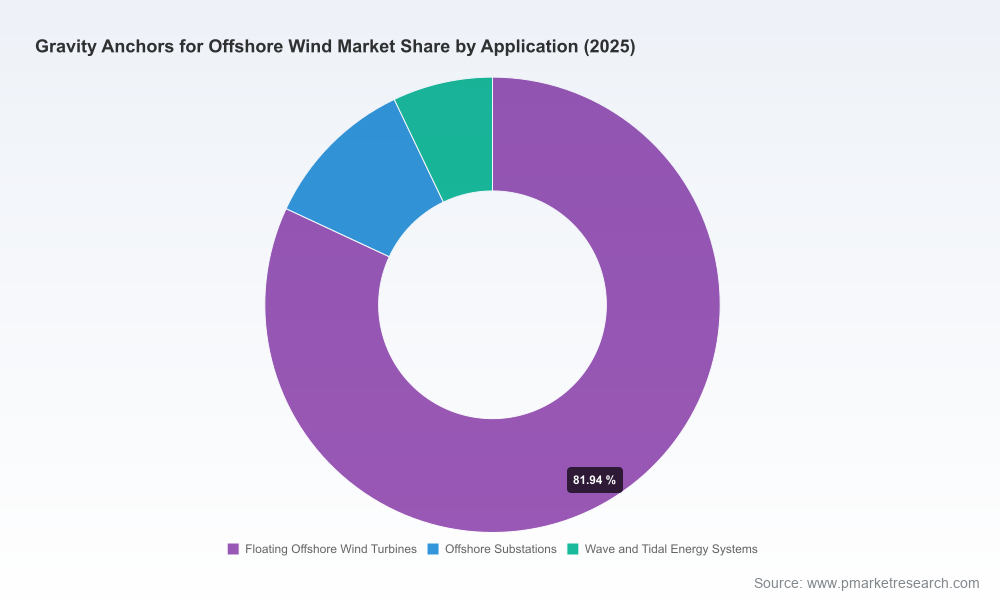

Gravity anchors — the deadweight solutions used to secure floating platforms and certain fixed-bottom structures — have moved from niche application to a material procurement category within the offshore wind value chain. Our analysis shows the global market for gravity anchors accelerating sharply: total market value rose from USD 175.4 Million in 2020 to USD 412.5 Million in the base year (2025), and is projected to approach USD 1,478.06 Million by 2032. That expansion equates to an approximate 20.0% compound annual growth rate across the 2026–2032 forecast window.

Gravity Anchors For Offshore Wind Market

Concentration metrics indicate an industry that is consolidating but still open: the top three suppliers account for roughly 42% of market revenues, while the top five capture close to 58% — a structure that favors scale players yet leaves room for technology-focused entrants, regional fabricators and specialized niche suppliers.

Gravity Anchors For Offshore Wind Market

Timing and scale: With the market expected to more than triple over the coming decade, procurement windows in 2026 will determine supplier ramps and capacity commitments through 2028–2030. Contractors and developers who lock in supply relationships early will influence lead times and cost curves for subsequent project phases.

Manufacturing siting and content rules: Tariff shifts and domestic-content regimes (notably revisions enacted in early 2025) materially affect landed cost and project compliance. Decisions about dual-track manufacturing footprints and near-market fabrication will be strategic, not tactical.

Technology selection and lifecycle economics: Choices between concrete-dominant designs, hybrid solutions and higher-density cast options carry different CapEx, GHG profiles and logistics footprints. Our models quantify these trade-offs and their sensitivity to material price shocks and shipping cost volatility.

Competitive positioning: Market structure data indicate the space is neither winner-take-all nor fragmented beyond repair. Strategic partnerships, IP capture (e.g., 3D printing, density-optimized alloys) and service bundling (EPC + mooring systems + installation) will determine who captures margin uplift.

The complete Gravity Anchors For Offshore Wind Market report is constructed as an operator’s toolkit rather than an academic exercise. It contains:

Forward-looking demand model (2026–2032) with scenario analysis that ties anchor volume and value to project sanction timelines, platform typologies and installation phasing.

Supply-side atlas mapping manufacturing capacities, typical lead times, and modularization opportunities across major industrial hubs — built to inform make-vs-buy and siting decisions.

Cost and carbon curves for competing anchor concepts, including sensitivity to steel and cement commodity swings, transport logistics, and localized fabrication strategies.

Procurement playbook for developers and OEMs: tender templates, performance specifications, inspection and testing regimes, and contractual risk allocation options optimized for gravity-anchor scopes.

Commercial risk matrix covering regulatory shifts, tariff impacts, material supply shocks, and seabed/geotechnical uncertainty — with mitigation levers prioritized by cost-efficiency and lead-time effect.

Financial models for investors: integrated CapEx/Opex schedules, payback analysis across anchor options, and scenario outputs for sensitivity to commodity and logistics inflation.

Executive-ready slides and a supplier short-listing tool that allow procurement teams to converge to a preferred panel within 90 days.

The gravity-anchor market already shows a mix of large engineering houses, specialized casting firms and technology innovators. Our qualitative assessment of the leading players highlights differing routes to scale and value capture:

Offshore Wind Design AS (Norway) — A platform engineering specialist that offers standardized gravity anchors as part of full EPC packages, including system engineering, geotechnical evaluation, manufacturing oversight and on-site delivery. Their strength lies in integration across platform and mooring scopes, which reduces interface risk for large projects and positions them well for bundled procurement strategies.

FMGC (Farinia Group, France) — A cast-iron specialist that optimizes density to reduce mass and transport penalties. Their value proposition is product-level optimization that reduces installation complexity and logistical overhead, which can be compelling where port handling and vessel time are cost drivers.

Sperra (RCAM Technologies, United States) — An emerging technology player applying 3D concrete printing to gravity-anchor production. Recent announcements show successful full-scale deployment at a demonstration site in Portugal (March 2026), illustrating the technology’s near-term potential to reduce concrete usage and enable near-site manufacturing strategies that may shorten supply chains.

Aubin Oceanatics (United Kingdom) — Developer of variable-density LiquiDense anchors using steel shells filled with high-density ballast. Their approach targets seabed agnosticism and deep-water adaptability, making it attractive where geotechnical variability raises embedding risk for other concepts.

Triton Anchor (United States) — Focused on low-cost, low-noise anchoring systems adaptable from catenary to tension-leg configurations. Their product set is positioned to compete on cost and ease of installation, especially in smaller-scale arrays or where acoustic impact constraints are critical.

These players illustrate two strategic vectors: integrated engineering houses that de-risk project interfaces, and technology specialists that aim to win on unit cost, manufacturability or installation efficiency. Our report maps each supplier’s strengths to project archetypes and procurement strategies, enabling buyers to assemble a supplier panel tailored to their project mix.

Materials shift: Industry studies and lifecycle assessments point to a move towards concrete-dominant designs where possible — not only for cost advantages but for lower embodied emissions. That said, density trade-offs and handling constraints mean hybrid designs and cast-iron solutions will remain important in deep-water or constrained-port scenarios.

Tariffs and localization: Revised duties on imported concrete and steel components implemented in early 2025 have already induced manufacturers to design dual-track production strategies. For buyers, this raises the value of suppliers with modularized, near-market fabrication capabilities or strong JV partners in target geographies.

Seabed and technical fit: Anchor selection remains highly site-specific. Gravity anchors are competitive for a subset of seabed types and water depths; other anchoring solutions retain relevance depending on geotechnical conditions. Our geotechnical decision matrix is designed to translate site data into a short-list of optimal anchor families.

Mitigate supply-side concentration: Given the observed market concentration, buyers should adopt a two-tier sourcing strategy: secure primary capacity with established suppliers while qualifying at least one alternative or local fabricator to reduce single-source exposure.

Lock logistics early: Gravity anchors are heavy and volume-intensive. Early agreements on load-out windows, vessel charters and port readiness materially reduce schedule and cost risk.

Value innovation judiciously: Emerging manufacturing methods (e.g., 3D concrete printing) present compelling cost and localization benefits, but deployment risk remains on ramping quality controls and certification pathways. Adopt staged acceptance criteria and pilot deployments within major projects’ early packages.

Factor carbon and financing: Low-carbon anchor designs improve access to green finance and can reduce the cost of capital. Incorporate embodied emissions metrics into tender scoring to differentiate suppliers aligned with corporate sustainability targets.

For executives and procurement leads, the report is intentionally action-oriented: it prioritizes decision-relevant outputs (procurement schedules, supplier short-lists, risk-mitigated cost curves, and scenario models) over exhaustive segmentation tables in the preview. The full dataset includes granular regional, material and application splits, buildable supplier scorecards, and downloadable model workbooks — essential for internal approvals and board-level investment cases.

We designed the deliverables to be operational on day one: a 90-day procurement acceleration plan, a manufacturing siting decision matrix, and an investor memo template that quantifies upside and downside across technology and policy scenarios.

Sperra’s March 2026 deployment of a full-scale 3D-printed concrete anchor at a Portuguese demonstration site demonstrates how additive manufacturing is moving from lab pilots to operational validation. This is the type of near-term technological shift that could alter local fabrication economics.

Industry publications throughout late 2025 reiterated gravity anchors’ role alongside suction, drag and pile systems, highlighting that economic viability is increasingly a function of port infrastructure, material pricing and seabed conditions.

This preview highlights the strategic questions that will shape gravity-anchor sourcing and design choices in 2026. To execute with confidence — whether you are a developer, OEM, investor or fabricator — you will need the full report’s models, segmented demand tables and supplier scorecards.

Access the complete Gravity Anchors For Offshore Wind Market report for the full datasets, downloadable financial models and our recommended procurement templates. The detailed segmentation and supplier-level data are intentionally housed in the full report to preserve the integrity of proprietary modelling and to support bespoke client workshops.

PW Consulting stands ready to run a tailored workshop to translate the report’s outputs into an executable 12–24 month procurement and manufacturing plan for your portfolio. Contact our industry team to schedule a briefing and to obtain the full report.

For detailed analysis of this topic, please visit the official page:Gravity Anchors For Offshore Wind Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com