How 3D Printing Is Transforming Modern Manufacturing

Other |

2026-06-09 11:31:02

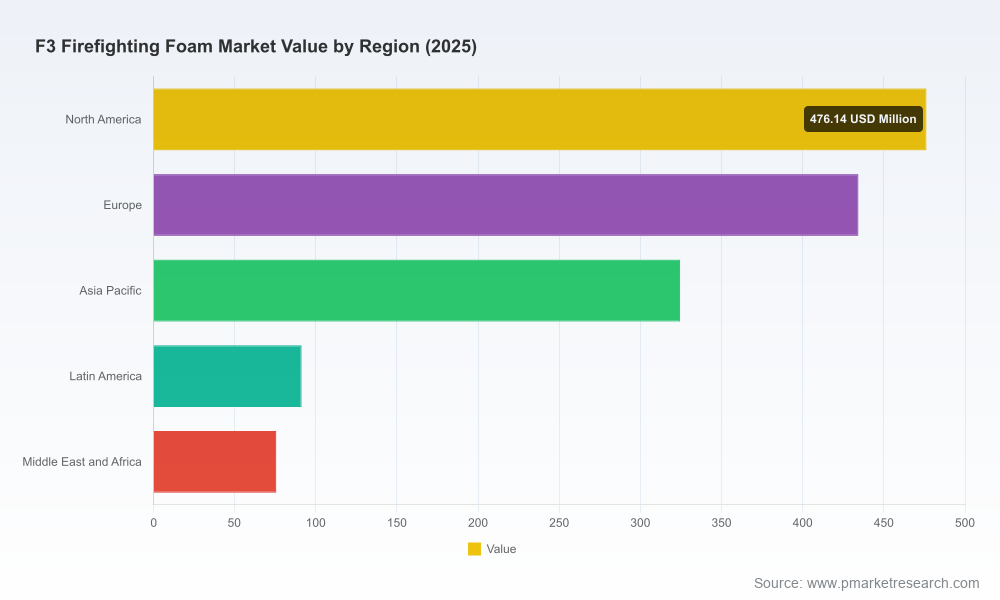

As regulatory urgency, certification milestones, and buyer migration converge, F3 (fluorine-free firefighting foam) has moved from niche alternative to procurement imperative. PW Consulting’s new F3 Firefighting Foam Market Report (base year 2025; forecast 2026–2032) distills the operational intelligence that corporate safety, procurement, R&D and M&A teams need to make defensible decisions through 2026 and beyond. Our model shows the global market expanding from roughly USD 810 million in 2020 to about USD 1.40 billion in 2025, with a near-term projection into 2026 and a compound annual growth rate (CAGR) of 11.24% across the forecast window — reaching an expected market size that approaches USD 3.0 billion by 2032. This release is designed as a decision-making tool: deep, practical, and intentionally selective in public granularity so readers must engage with the full report for the complete dataset and strategic templates.

F3 Firefighting Foam Market

Regulatory inflection points are creating time-bound windows for action. Military, aviation, maritime and national regulators have issued deadlines and prohibitions that materially affect legacy AFFF inventories and future procurement specifications. The downstream consequences include compliance-driven replacement cycles, changes to training and testing regimes, and new capital planning requirements for fixed systems.

F3 Firefighting Foam Market

Certification is now the critical axis of commercial differentiation. Recent product approvals and first-to-market listings are shortening procurement timetables for institutions that require MIL or ICAO equivalence. Buyers are prioritizing vendors with both laboratory performance and field-validated approvals.

F3 Firefighting Foam Market

Market scale and growth dynamics make F3 transition a programmatic challenge — not a single-vendor decision. With the overall market roughly doubling in five years and continuing strong growth, supply chain resilience, inventory conversion strategies, and lifecycle cost modeling are central to minimizing operational risk.

Executive summary and actionable decision tree for 12–24 month implementation plans.

Proprietary market-size and forecast model (2020–2032) with scenario stress tests—baseline, accelerated regulatory adoption, and technology-displacement scenarios.

Certification and standards map linking product types to procurement requirements across military, aviation, maritime, industrial and municipal buyers.

Vendor heatmap and scorecard: performance, certification breadth, biodegradability credentials, supply footprint, and commercial readiness.

Procurement playbooks: RFP templates, acceptance testing protocols, supplier risk clauses, and contract language for inventory buy-backs and warranties.

Operational integration blueprints for fixed systems, ARFF (aircraft rescue and firefighting), hydrant networks and portable systems, with CAPEX/OPEX modelling templates.

Environmental and PR risk matrices, including regulatory timelines, disposal pathways for legacy agents, and stakeholder communication frameworks.

M&A and partnership pipeline: prioritized targets and diligence checklists for corporates seeking rapid capability or geographic scale.

Three quantitative signals should be part of every boardroom discussion in 2026:

Scale and acceleration: The market has expanded materially across the 2020–2025 period and is forecast to sustain double-digit growth through the medium term. That trajectory creates both procurement demand and supplier opportunity.

Concentration metrics: The market exhibits moderate concentration among established global vendors, with the top three and five suppliers accounting for meaningful shares of commercial supply. This structure implies that a small set of qualification wins can meaningfully shift regional procurement outcomes and that competitive dynamics will center on certification timing, supply assurance, and lifecycle cost claims.

Certification as a gating factor: Recent approvals and firsts have demonstrable commercial impact — vendors who secure MIL, ICAO, FM and UL/ULC equivalencies are being included in accelerated supplier lists, especially for airports, defense sites, and critical infrastructure.

The competitive set combines legacy foam incumbents, fluorine-free pioneers and regional specialists. Our vendor analysis synthesizes performance claims, certification breadth, and go-to-market posture to produce a pragmatic purchaser’s shortlist.

Established F3 pioneers: Companies that invested early in fluorine-free R&D now benefit from demonstrable product families with multiple certifications. Their strength is validated performance and breadth of applications, particularly where legacy AFFF replacements must meet stringent standards.

Certification-first market leaders: Vendors achieving recent approvals for fixed systems and sprinkler compatibility have opened new commercial channels in hangars and storage facilities. Such certifications are a near-term competitive differentiator for institutional buyers.

Regional and sector specialists: Firms with targeted offerings for marine, aviation or petrochemical segments complement global players by providing localized service models, training, and retrofit capabilities—important where rapid site-level conversion is required.

Representative market moves underline these dynamics: in 2026 a leading supplier achieved a first-in-class approval for fixed sprinkler systems, directly enabling their entry into previously closed procurement channels; another high-profile vendor introduced the first UL/ULC-listed 1% AR product for hydrocarbon fires, materially shifting the performance-versus-dosage debate. PW Consulting’s vendor dossiers weave these developments into supply-risk scores and recommended procurement templates.

Immediate (0–6 months): Conduct an inventory and exposure audit. Map which sites are governed by defense, airport, maritime or state-level prohibitions and quantify mitigation cost drivers (decontamination, disposal, testing). Use our checklist to establish an urgent conversion prioritization.

Near-term (6–18 months): Run certification-aligned pilots with two vendors (one global leader, one regional specialist). Require third-party verification, include exchange/return terms for legacy stock, and embed service-level agreements for system retrofits and training.

Medium-term (18–36 months): Lock multi-year supply arrangements with capacity guarantees, align asset replacement with capital cycles, and consider bolt-on acquisitions to secure channel access or specialized formulation IP.

Procurement: Leverage RFP templates and the supplier heatmap to shorten qualification timelines and standardize acceptance tests tied to certifications.

Operations & Safety: Use retrofit blueprints and performance benchmarks to plan system downtime, training, and live-fire verification without interrupting critical services.

Legal & Compliance: Employ regulatory roadmaps and disposal pathways to reduce legal exposure from legacy PFAS inventories and to structure supplier indemnities.

Finance & M&A: Apply our scenario models to stress-test cashflow impacts of staged replacements and to prioritize acquisition targets that close capability gaps.

In keeping with our “trailer” approach, this release demonstrates the depth and prescriptive value of our analysis while omitting the granular segmentation tables and contract-level templates that operational teams require to execute. The full report contains the complete regional and application breakdowns, time-phased adoption curves, vendor scorecards with scoring details, and downloadable procurement instruments. These deliverables are essential for any team executing conversions or evaluating supplier integrations and are available through our report portal and bespoke advisory engagements.

2026 is a year for disciplined transition planning. Organizations that treat F3 adoption as a strategic program — aligning procurement, operations, compliance and stakeholder communications — will avoid costly reactive conversions and position themselves to capture efficiency gains from lower-dosage formulations and modern foam-system integrations. PW Consulting’s F3 market model and operational playbooks convert regulatory pressure into a structured program with measurable milestones.

For senior leaders preparing capital budgets, safety directors validating supplier claims, or corporate development teams sizing acquisition opportunities, our report is a practical, evidence-based toolkit. Visit our report page to access the full dataset, vendor scorecards, scenario model files and downloadable procurement templates, or contact PW Consulting for a tailored executive briefing and hands-on implementation support.

For detailed analysis of this topic, please visit the official page:F3 Firefighting Foam Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com