Revision Gynaecomastia Surgery in Dubai: Correcting Previous Results

Health |

2026-05-06 07:47:13

PW Consulting’s latest market study on the Oil Fired Water Heater market—anchored on 2025 as the base year with historical analysis spanning 2020–2025 and a forward-looking forecast covering 2026–2032—translates incremental growth into actionable strategy. The market demonstrates steady expansion from roughly USD 403 million in 2023 to USD 420 million in 2025 and is projected to reach about USD 486 million by 2032, implying a compound annual growth rate of approximately 2.12% over the forecast window. For executives preparing budgets, product roadmaps, and M&A pipelines in 2026, this report converts modest growth into concrete decision levers across product, channel, and regulatory risk management.

Oil Fired Water Heater Market

The market’s steady growth—measured across a multi-year historical run and a 2026–2032 forecast—conceals several inflection points that matter to strategy teams. First, regulatory regimes in large markets are increasingly central to product viability. U.S. federal energy conservation standards for oil-fired storage water heaters (≤50 gallons) already prescribe minimum uniform energy factor requirements under an established formula (for example, legacy formulations that adjust with unit volume), and Canada enforces input-rate thresholds for household oil-fired water heaters. These frameworks raise the compliance bar for new product introductions and make retrofitting and aftermarket service a revenue priority.

Oil Fired Water Heater Market

Second, the absence of ENERGY STAR requirements for oil-fired water heaters in the U.S. (as of the latest federal guidance) creates a mixed incentive environment for manufacturers: product differentiation must rely on efficiency claims validated by regulation and customer economics rather than an industry-wide label. Third, the segment’s low penetration relative to alternative fuel sources—historical shipments indicate residential oil-fired storage units numbered in the low thousands in recent years and remain a small fraction of gas-fired appliance shipments—means the market is concentrated among specific customer cohorts (legacy rural, off-grid, or specialty commercial applications), which in turn shapes distribution and service models.

Oil Fired Water Heater Market

Oil price dynamics materially influence replacement cycles and the economics of high-efficiency upgrades. PW Consulting’s sensitivity models show that near-term reductions in heating oil cost reduce short-term conversion economics to high-efficiency condensing units, delaying some retrofit investment decisions, while prolonged price increases can accelerate conversions and create immediate aftermarket opportunity. For example, government and independent forecasts pointing to a lower winter heating oil price in 2025 relative to prior seasons moderate retrofit incentives—an input that should be baked into 2026 procurement and channel incentives.

The competitive landscape is mixed: a small set of legacy players maintains strong brand recognition in key markets while a broader tier of regional and niche manufacturers addresses specialized applications. Market concentration metrics indicate a moderate leader set (top 3 firms control roughly 38.5% of the market; top 5 account for about 52.1%), leaving meaningful share for challenger strategies and consolidation plays.

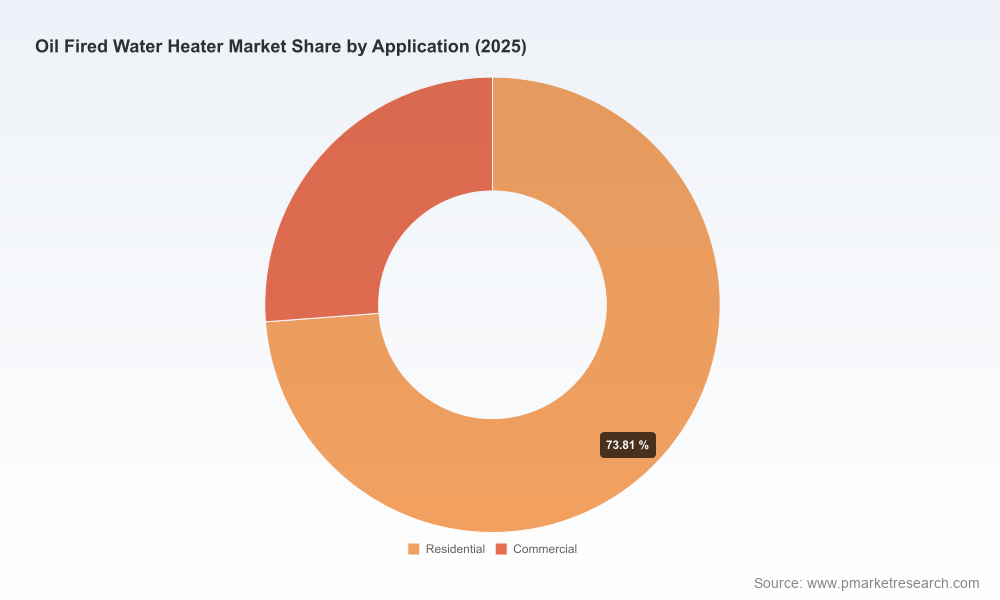

Our analysis segments the market by product architecture (conventional vs. high-efficiency condensing), by application (residential vs. commercial), and by region. Rather than publishing proprietary split numbers in this briefing, PW Consulting highlights directional dynamics that matter to strategists:

For readers seeking granular split tables, regional demand curves, and channel-level margin benchmarks, the full dataset and interactive dashboards are available on the PW Consulting portal.

Based on the market outlook and competitive moves, PW Consulting recommends a prioritized set of actions for 2026:

The full report combines strategic narrative with operational tools tailored for 2026 execution, including:

These deliverables are intentionally modular so that commercial teams, product managers, and corporate development groups can extract the components they need for board presentations and investment memos.

The study is grounded in a combination of primary interviews with OEMs, distributors, and large contractors; longitudinal shipment and pricing data; regulatory filings; and commodity-price scenarios from independent agencies. Base-year accounting is 2025, and the forecast horizon is 2026–2032. Revenue measures throughout the report are expressed in USD (Million) to maintain comparability across geographies and product classes.

Oil-fired water heaters are a mature, niche market with tactical pockets of opportunity. The PW Consulting report translates steady market growth (from roughly USD 403 million in 2023 to USD 420 million in 2025 and forecast to roughly USD 486 million by 2032 at a ~2.12% CAGR) into a clear set of 2026 choices: protect legacy economics through aftermarket and service, selectively invest in higher-efficiency platforms where regulation or economics justify, and use consolidation dynamics to optimise channels and parts ecosystems. Leaders who combine regulatory foresight with pragmatic product and service economics will convert a modest market expansion into sustainable margin growth.

For the full datasets, regional models, and the operational playbook referenced above, please consult the PW Consulting Oil Fired Water Heater Market report and interactive web dashboard.

For detailed analysis of this topic, please visit the official page:Oil Fired Water Heater Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com