Serums For Skincare Hydration And Advanced Skin Care Routines

Other |

2026-05-29 16:53:49

As organizations finalize budgets and revisit strategic roadmaps for 2026, the aluminum silicate ceramic value chain presents a mix of steady demand, supply-side repositioning, and regulatory acceleration that will shape near-term winner-takes-most moves and mid-cycle consolidation. PW Consulting’s latest market research—anchored on a 2025 base year and a 2026–2032 forecast horizon—provides a tactical playbook for executives, investors, and supply-chain leaders who need to convert market signals into high-confidence decisions.

Aluminum Silicate Ceramic Market

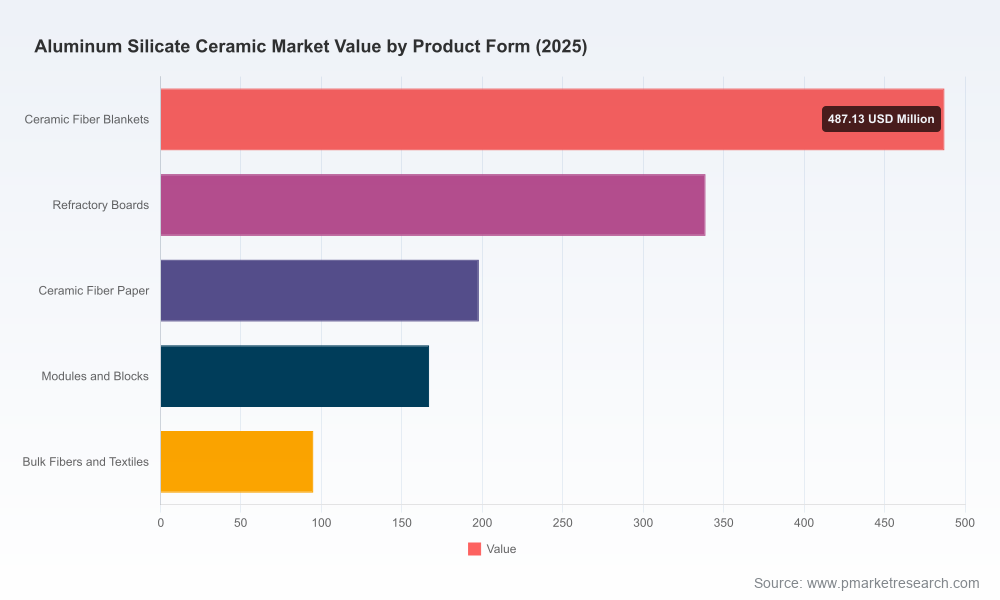

Our proprietary market model pegs the global aluminum silicate ceramic market at approximately USD 1.29 billion in 2025, with the market expected to grow to about USD 1.34 billion in 2026 and reach roughly USD 1.95 billion by 2032. The forecast period is underpinned by a compound annual growth rate of 6.12% (2026–2032). That growth profile signals a durable expansion that is large enough to justify strategic investments—but not so explosive as to remove the need for disciplined capital allocation, supplier selection, and operational excellence.

Aluminum Silicate Ceramic Market

For 2026 decision cycles this translates into two immediate imperatives:

Aluminum Silicate Ceramic Market

This release is intentionally a strategic "trailer"—we provide robust context, decision frameworks, and operational tools while withholding the granular proprietary tables reserved for the full report. Highlights include:

These deliverables are explicitly designed to be executable in 90–180 day sprints, enabling procurement, R&D, and corporate development teams to translate insight into measurable outcomes before the end of 2026.

The aluminum silicate ceramic market is characterized by a mix of global technical ceramics leaders and specialized regional manufacturers. Key participants include CoorsTek Inc., Saint-Gobain Ceramics & Plastics, Kyocera Corporation, Morgan Advanced Materials, CeramTec, and notable Chinese producers such as Luyang and Taisheng. Specialist U.S. and European firms—ranging from Advanced Ceramic Materials to C‑Mac International—remain important for custom, high-performance, or low-volume applications.

Strategically, this mix produces a market that rewards scale and specialized capabilities while still leaving niches where technical differentiation and customer intimacy drive premium margins. For 2026, expect to see more partnerships between global engineering ceramics majors and regional producers to optimize footings in high-growth end markets.

Producers of aluminum silicate ceramics depend on a narrow set of feedstocks, including kaolin, kyanite, and bauxite for synthetic mullite and related products. Our analysis identifies three structural supply-risk vectors that should inform 2026 procurement and investment plans:

Buyers and producers must therefore integrate commodity hedges, process-efficiency projects, and feedstock diversification into their 2026 plans to preserve margin upside.

Environmental regulations and decarbonization policies are more than compliance costs; they are demand drivers. PW Consulting’s regulatory tracker shows that policies targeting energy efficiency and emissions reduction are increasing demand for lightweight, high-temperature insulation—an area where aluminum silicate fiber products have a comparative advantage.

Concurrently, low-carbon binders and geopolymer technologies—based on alkali-activated aluminosilicates—offer significant lifecycle CO2 reductions versus traditional binders. These technologies are not just R&D curiosities; they are nearing commercially relevant scale and will be a critical differentiator for buyers seeking low-carbon construction and refractory solutions.

For executives preparing 2026 budgets and strategic plans, the value of PW Consulting’s research lies in converting noisy, often conflicting public cues into a clear set of prioritized actions. The combination of a validated market model (2020–2025 historical base and 2026–2032 forecasts), supply-chain maps, and playbooks means teams can take operational steps this quarter that materially change 2026 outcomes—without waiting for perfect visibility.

This release intentionally showcases strategic signal and practical frameworks while withholding proprietary segment tables, regional splits, and detailed product-form revenue breakdowns to protect the analytical integrity of the full report. Clients who require the full dataset—including detailed segmentation, concentration matrices, supplier-level profiles, and the complete appendix of primary interviews—can access the comprehensive report and downloadable models via PW Consulting’s report page.

In an industry at the intersection of materials science, decarbonization policy, and industrial demand cycles, clarity and speed of execution will determine the winners in 2026. PW Consulting’s Aluminum Silicate Ceramic Market report delivers both—grounded forecasts and tactical playbooks—so leaders can act decisively as the market evolves.

For detailed analysis of this topic, please visit the official page:Aluminum Silicate Ceramic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com