Dental Tooth Removal In Dubai: Cost Breakdown

Health |

2026-04-27 06:32:05

PW Consulting today releases a strategic preview of our forthcoming Road Crash Attenuator Market report (base year 2025, forecast 2026–2032). This briefing outlines the report’s strategic value for corporate decision-makers preparing plans and capital allocation strategies for 2026. It highlights the macro growth trajectory, near-term market dynamics, competitive posture, and the practical, action-oriented deliverables included in the full study — while preserving the proprietary segment-level tables and transaction-ready datasets that drive tactical execution.

Road Crash Attenuator Market

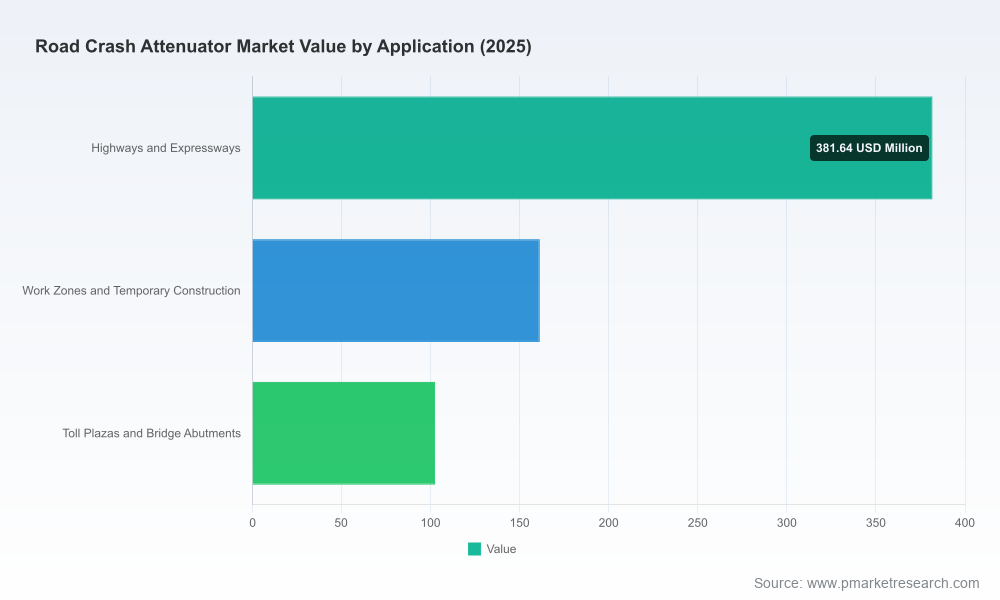

Road crash attenuators are moving from a niche safety component to a portfolio-level priority for highway authorities, major contractors, and OEMs. Our analysis shows the global market expanded from approximately USD 485 million in 2020 to USD 645.5 million in 2025. Under a base-case outlook, the market is forecast to continue to expand to about USD 977 million by 2032, representing a compound annual growth rate (CAGR) of roughly 6.09% during the 2026–2032 forecast window. That steady expansion is driven by the twin forces of infrastructure renewal programs and evolving safety regulations that raise minimum performance and deployment expectations.

Road Crash Attenuator Market

For executive teams, 2026 is a decision inflection point: procurement cycles initiated this year set product adoption patterns for the next five to seven years. The strategic questions for 2026 are therefore existential — which technologies to prioritize, how to hedge raw-material exposure, and where to concentrate commercial and R&D resources to capture the next wave of growth.

Road Crash Attenuator Market

Regulatory uplift and specification rigour. Governments and highway authorities are consolidating safety standards. In the U.S., federal-aid eligibility hinges on products complying with AASHTO MASH or legacy NCHRP 350 TL-3 performance criteria as assessed by FHWA. In Europe, EN 1317 test standards and the ASI A performance class remain decisive for high-speed installations. These regulatory baselines are continuing to push purchasers toward MASH- and EN-certified systems and to favor modular, repairable solutions that minimize lifecycle cost.

Raw-material and input volatility. Steel remains a primary component for many attenuator frames and mounting structures. U.S. hot-rolled coil (HRC) prices were reported in the region of USD 1,002–1,118 per short ton in early 2026 — a level that materially affects margins on steel-intensive systems. Procurement teams must build steel-price pass-throughs and alternative-material plans into contract templates for 2026 projects.

Product innovation concentrated around deployability and lifecycle cost. Market momentum is coalescing around features that lower downtime in work zone environments: rapid deploy/stow TMAs, modular crash cushion elements for expedited repairs, and speed-adaptive attenuation technologies that optimize energy absorption across vehicle classes. These technical differentiators are increasingly decisive at specification and RFP stages.

Moderate market concentration. The market exhibits a mid-level concentration profile: the top three players capture a meaningful share of commercial activity, and the top five together represent a majority presence. That structure creates both competitive pressures on margins and opportunities for nimble challengers to claim localized advantage through service models and specification partnerships.

Our competitive review focuses on incumbents and fast-follow innovators that will influence procurement decisions in 2026 and beyond. The companies assessed in the full report include global and regional players with complementary strengths in product engineering, certification experience, and channel reach.

Lindsay Corporation (Omaha, Nebraska) — Lindsay brings a broad portfolio spanning reusable redirective systems and anchorless, water-filled options, plus a growing line of truck-mounted attenuators. Recent launches (notably a next-generation Road Runner TMA with sub-30-second deploy/stow capability in early 2026 and a wider TAU-M system introduced in late 2025) underscore a go-to-market strategy that emphasizes rapid deployment and simplified maintenance — attributes that map directly to the procurement priorities of municipal and state highway agencies.

TrafFix Devices (San Clemente, California) — TrafFix remains a technology leader in redirective, non-gating crash cushions and compact TMAs. Its family of products that achieve high-performance eligibility under contemporary test standards is positioned to capture customers who prioritize compact deployment footprints and full-width protection in temporary work zones.

Hill & Smith (part of Hill & Smith Holdings) — The Smart Cushion product line exemplifies an engineering-led differentiation rooted in speed-dependent, self-restoring behavior that optimizes deceleration across vehicle weights and speeds. Such feature-led differentiation is likely to be a decider in agency-level competitive tenders that award based on lifecycle performance metrics rather than initial capex alone.

Valtir, LLC / Energy Absorption Systems — A broad portfolio, from QuadGuard systems to truck-mounted solutions and compact storage TMAs, positions Valtir and its heritage brands to serve cross-segment needs. Productized operational features (e.g., 180° tilt TMAs for compact storage) address fleet utilization economics — an important angle for large contractors and rental fleets.

Saferoad (Europe) — Saferoad’s modular CrashGuard line, certified for high-speed installations and conforming to EN 1317 standards with ASI A classification, highlights the premium segment in European markets where performance classes and CE marking materially influence spec selection.

Collectively, these firms illustrate two operational archetypes that will dominate 2026 procurement outcomes: (1) feature-first innovators who drive specification changes, and (2) scale-first incumbents who leverage certification breadth and service networks to win large framework contracts.

The full Road Crash Attenuator Market report is structured to be a practical playbook for executives and procurement leaders. Key deliverables include:

Verified market-sizing model. Time-series revenue estimates (historical 2020–2025 and forecast 2026–2032) with transparent assumptions and sensitivity ranges. The model supports scenario planning (base, upside, downside) and allows users to pivot assumptions on infrastructure spending, regulatory adoption, and unit price trajectories.

Regulatory and specification matrix. A consolidated guide to national and regional standards, test-level equivalencies, and practical compliance pathways for product certification — designed to accelerate time-to-eligibility for specification on major projects.

Strategic supplier landscaping and due-diligence templates. Comparative profiles, capability heatmaps, and an M&A target screening framework that identifies assets with strategic fit by technology, certification portfolio, and channel footprint.

Procurement playbook. RFP scoring templates, service-level contracting clauses to mitigate raw-material price exposure, and adoption roadmaps for pilots and scaled rollouts tailored to national procurement cycles.

Product and innovation roadmap guidance. Technology prioritization matrices that reconcile R&D spend with near-term ROI — for example, investments in rapid-deploy TMAs and modular repairability that directly shorten work zone downtime and lower lifecycle spend.

Commercial intelligence for sales acceleration. Account prioritization algorithms and tender-win playbooks that help suppliers structure bids to win long-term framework agreements.

Based on our analysis, PW Consulting recommends the following priority actions for companies and procurement bodies planning for 2026:

Lock in supply and hedges for steel-intensive components. Given recent HRC price levels and their impact on margin, include indexed clauses and alternative-material options in multi-year supply contracts.

Prioritize MASH/EN certification pipelines now. Certification timelines can be multi-quarter. Products not aligned with AASHTO MASH or EN 1317 pathways face limited eligibility for major projects; accelerate test programs where necessary.

Invest in rapid-deploy and modular repair features. Demonstrable reductions in work zone downtime and maintenance cycles convert directly into procurement preference — and are a defensible premium in tender scoring.

Win through service and fleet economics. For suppliers, build rental and maintenance propositions that minimize total cost of ownership for large contractors and state agencies; for buyers, quantify fleet utilization gains from compact-storage TMAs and faster repairability.

Use scenario-based capital planning. Incorporate the PW Consulting market model into capex prioritization: compare base-case revenue growth (6.09% CAGR to 2032) against specific agency pipeline commitments to stress-test investment decisions.

This preview provides senior leaders with the strategic context necessary to make informed choices in 2026. The full PW Consulting Road Crash Attenuator Market report contains the detailed segment-level datasets, regional demand models, and supplier-specific unit economics required to operationalize the recommendations above. We deliberately reserve those granular tables and segment breakouts for the full publication to preserve the integrity of our proprietary analysis and to enable you to act with the complete dataset in hand.

For organizations preparing procurement strategies, product investment cases, or M&A diligence in 2026, the full report will convert the directional insights presented here into executable plans, with spreadsheet-ready models and templated contracting language that shorten time to value.

PW Consulting is a strategy advisory and industry research firm specializing in infrastructure safety systems and transportation technologies. Our advisory services combine rigorous market analytics, regulatory expertise, and hands-on procurement experience to help clients translate market dynamics into confident decisions.

To access the complete Road Crash Attenuator Market report, including the full set of segment tables, supplier profiles, and actionable templates, please visit our report page or contact your PW Consulting representative.

For detailed analysis of this topic, please visit the official page:Road Crash Attenuator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com