Liquid Dairy Products Market — Strategic Preview for 2026: Actionable Intelligence from PW Consulting

PW Consulting’s latest market brief on Liquid Dairy Products synthesizes macro trajectories, competitive positioning, regulatory shifts, and near-term operational levers that will determine winners and laggards in 2026. This preview explains why executives, investors, and supply-chain leaders should treat the report as a decision-support toolkit for next-year planning — while preserving select proprietary segment-level granularity to encourage direct access to the full study.

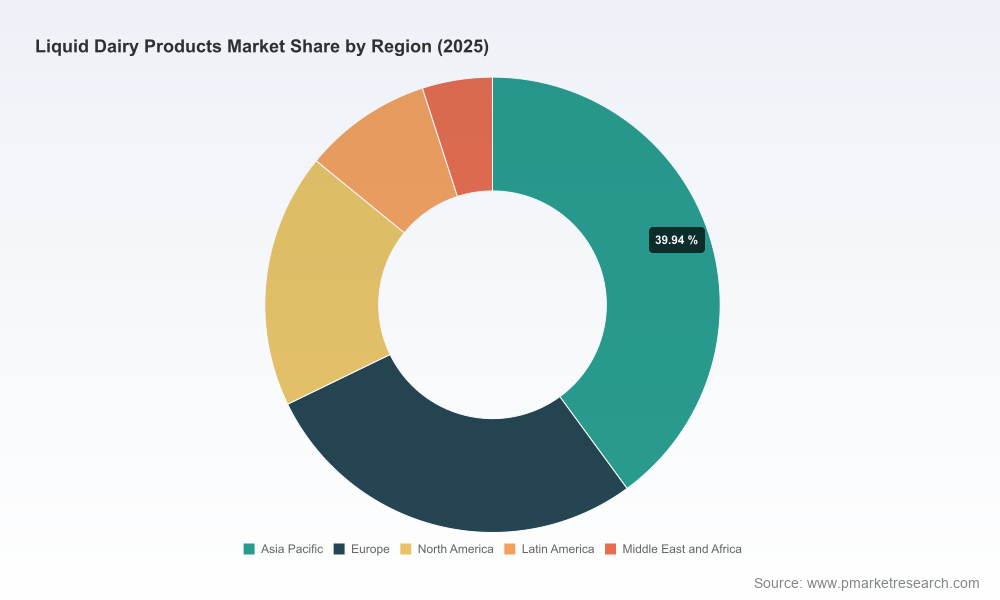

Liquid Dairy Products Market

Market Snapshot: Size, Growth, and Structure

The global liquid dairy products market reached an estimated USD 373.6 Billion in our base year 2025 and is forecast to advance to roughly USD 392.5 Billion in 2026, with a compound annual growth rate (CAGR) of approximately 4.51% across the 2026–2032 forecast window. By the end of the outlook period the market is projected to approach the half-trillion-dollar threshold, underscoring the category’s resilience despite periodic commodity pressure and shifting consumer preferences.

Liquid Dairy Products Market

Concentration metrics confirm a mid-fragmented industry: the leading three firms account for just over one-fifth of the market and the top five capture roughly a third, leaving substantial room for regional champions, co-operatives, and acquisitive challengers to scale. This competitive topology rewards scale around manufacturing efficiency, route-to-market density, and differentiated product platforms (e.g., functional, lactose‑free, premium UHT and drinking yogurts).

Liquid Dairy Products Market

Why This Matters for 2026 Decisions

- Portfolio prioritization: With steady overall growth but uneven margin pressure across formats and channels, 2026 is a year to accelerate rationalization of low-yield SKUs and reallocate capital toward higher-margin, innovation-led subsegments.

- Cost and procurement strategy: A modest global milk supply uptick is creating short-term downward pressure on raw milk prices — a window for buyers to negotiate forward contracts and secure capacity at favorable rates.

- Channel investments: E-commerce and convenience channels continue to reshape assortment and packaging requirements; selective capex for flexible filling lines and cold-chain partners will be decisive.

- Regulatory and food-safety readiness: Recent policy moves and food-safety events underscore the need for rigorous compliance playbooks and real-time traceability investments.

Actionable Content — What the Full Report Delivers

PW Consulting’s full report is built for operational and board-level use. Key deliverables include:

- Forward-looking market sizing and scenario models with base-year validation and alternate demand scenarios tied to price shocks, consumption shifts, and policy actions.

- Commercial playbooks for channel optimization — including SKU rationalization matrices, margin-by-channel benchmarks, and retailer negotiation frameworks that translate macro growth into retailer-specific tactics.

- Supply-chain playbooks covering raw milk sourcing strategies, plant utilization roadmaps, and capital-allocation models for line flexibility vs. scale investments.

- Regulatory and safety risk matrices with remediation checklists and communication templates for multistakeholder incident response.

- Competitive battlecards for the leading global and regional players (profiles, capacity positioning, likely moves), plus an M&A heatmap highlighting attractive targets by capability and geography.

We intentionally do not disclose secondary segmentation numbers here; the full dataset and micro-level splits are available in the subscription report package and include granular, useable figures for board-level scenario planning and commercial budgeting.

Competitive Landscape: Strategic Profiles and Implications

The industry’s front-runners combine scale, integrated supply chains, brand equity, and increasing downstream innovation. Key firms to watch and how they influence market dynamics:

- Lactalis (Laval, France): As the world’s largest dairy company by revenue, Lactalis’ global processing footprint and capacity flexibility make it a price-maker in several exporting corridors. Their approach to procurement and global SKU rationalization sets benchmarks for cost efficiency.

- Nestlé S.A. (Vevey, Switzerland): With strength in branded nutritional and flavored beverages, Nestlé emphasizes portfolio premiumization and cross-category innovation (e.g., nutrition-enhanced milks), representing a template for driving value beyond commodity milk volumes.

- Dairy Farmers of America (Kansas City, USA): The cooperative model remains a powerful force in North American supply stability and farmer alignment; DFA’s strategic posture influences domestic fluid-milk flows and value-added beverage launches.

- Danone (Paris, France): Danone’s emphasis on drinking yogurts and premium dairy beverages — and its ongoing capacity buildouts for regional exports — illustrates a balanced growth strategy across mature and emerging markets.

- Yili Group (Hohhot, China) & Bright Dairy (Shanghai, China): China’s domestic champions continue to expand both inward and outward, prioritizing brand loyalty, premiumization, and UHT innovation for distribution beyond refrigeration-centric channels.

- Arla Foods, FrieslandCampina, Fonterra, Saputo, Meiji, Amul: These cooperatives and multinational processors each play differentiated roles — from organic and lactose-free leadership to regional logistics and export specialization — and are pivotal in shaping category access and pricing dynamics.

For market entrants and incumbents, the practical lesson is clear: scale buys optionality, but targeted differentiation and channel mastery can defeat raw scale — especially in local markets with strong incumbent co‑operatives.

Recent Industry Movements and Structural Signals

- Packaging and innovation investments: Tetra Pak’s new Product Development Center in Texas (groundbreaking in March 2026) signals an industry focus on rapid prototyping for packaging and processing that supports longer shelf-life formats and sustainability claims.

- Capacity expansion for regional supply: Danone’s investment to increase output in Kazakhstan underlines a trend to localize production for export corridors, reducing freight sensitivity and improving freshness economics.

- Distribution enhancement: FrieslandCampina’s new distribution infrastructure in Malaysia broadens last-mile capabilities for chilled assortments across Southeast Asia.

- Product innovation in response to demand shifts: Regional launches such as lactose-free variants in Egypt exemplify tactical portfolio moves to capture emerging consumer health trends.

Market Dynamics, Risks, and Early-Warning Signals for 2026

Three categories of dynamics will dominate boardroom attention in 2026:

- Commodity and margin pressure: Global milk production rose in 2025, generating supply-side easing and downward price pressure into 2026. Buyers and processors must monitor raw-milk pricing curves and use hedging, contract diversification, or value fabrication (e.g., ingredient extraction) to protect margin.

- Regulatory and policy shifts: Country-level decisions continue to reshape permissible production techniques and school-meal content. Notably, a prohibition on rBST in Argentina and expanded milk options in U.S. school programs illustrate how policy shifts can both constrain practices and create demand pockets. Firms should maintain active policy-tracking and scenario playbooks to respond rapidly.

- Food safety and reputational risk: Ongoing foodborne investigations — including recent multi-state outbreaks tied to unrelated dairy products — demonstrate how rapidly consumer confidence and trade flows can be affected. Preparedness requires traceability, plant-level sanitary improvements, and clear recall contingencies.

How to Use This Report in 2026 Planning Cycles

Executives and strategy teams should treat the PW Consulting study as a decision-enabling asset across four use cases:

- Budgeting and CAPEX prioritization: Use the market scenarios to stress-test capacity investments and time phasing, aligning line flexibility investments to the most resilient channels in our channel playbooks.

- M&A and partnership screening: Apply the M&A heatmap and competitive battlegrounds to identify bolt-on targets that produce step-change in distribution, private-label capabilities, or high-growth subsegments.

- Commercial transformation: Implement our retailer playbooks and SKU rationalization matrices to lift gross margins within 12 months without material revenue sacrifice.

- Risk management: Integrate the food-safety and compliance checklists into enterprise continuity planning, and use real-time supplier scoring to prioritize secure raw-milk sourcing.

Next Steps and Access

This briefing is designed to provide senior stakeholders with a rigorous orientation for 2026. The full PW Consulting Liquid Dairy Products Market report contains the proprietary, downloadable datasets, fine-grained segmentation, and benchmarking tools you need to convert insight into action. To preserve the report’s commercial integrity we have withheld certain granular segment tables and ranked component numbers from this public preview — these are included in the subscriber package together with interactive scenario models and implementation templates.

Inquiries from senior executives, corporate development teams, and investor groups are prioritized. PW Consulting’s advisory desk is available for custom briefings, tailored scenario workshops, and due‑diligence support that translate the report’s findings into a 90‑day action plan for your organization.

For detailed analysis of this topic, please visit the official page:Liquid Dairy Products Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com