Helicopter Crash Resistance Seats Market: Strategic Outlook for 2026 Decisions

PW Consulting today releases a forward-looking industry briefing derived from our comprehensive Helicopter Crash Resistance Seats Market report. As organizations plan capital allocation and product roadmaps for 2026, this analysis synthesizes macro growth trajectories, regulatory inflection points, supply-chain realities, and competitive dynamics to inform high-consequence decisions. The briefing intentionally surfaces the practical insights buyers, OEMs, Tier-1 suppliers, and defense planners need — while preserving the granular segmented datasets for report subscribers.

Helicopter Crash Resistance Seats Market

Executive snapshot

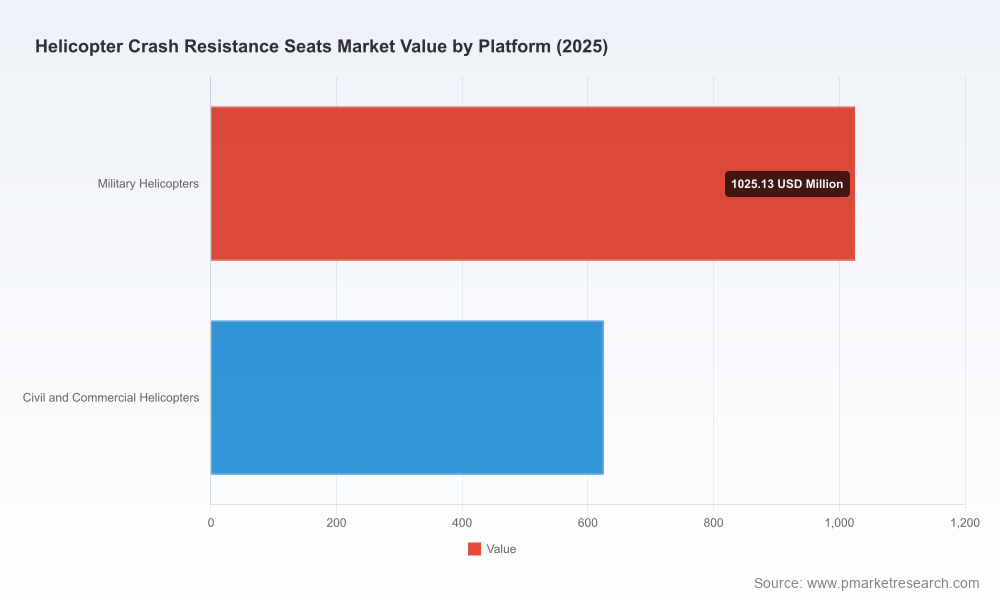

After reviewing five years of historical performance and running scenario-based forecasts through 2032, we find the crash-resistance seating market at a pivotal juncture. The global market reached approximately USD 1,650.45 Million in our base year (2025). Our forecast indicates steady expansion at a compound annual growth rate (CAGR) of 5.06% across the 2026–2032 period, culminating in an expected market size of roughly USD 2,331.65 Million by 2032 under the base case. Market concentration is moderate-to-high: the top three players hold nearly half of the market by revenue, and the top five account for over sixty percent — a structure that shapes bargaining power, innovation diffusion, and aftermarket dynamics.

Helicopter Crash Resistance Seats Market

Why this matters for 2026 planning

- Predictable growth, differentiated risk: A mid-single-digit CAGR creates room for steady investment, but the returns differ sharply by product positioning — retrofit kits, certified OEM systems, and lightweight composite-enabled seats each follow distinct commercialization timetables.

- Regulatory gating items: Certification dynamics (FAA, EASA, and MIL standards) remain the principal barriers and opportunities. Firms that front-load certification programs and STC strategies can convert regulatory complexity into competitive advantage.

- Supply-chain tightness: Raw material volatility and specialized manufacturing capacity will influence time-to-market and margins. Strategic sourcing and alternative material qualification are no longer optional.

Market dynamics distilled

Our analysis identifies three structural forces shaping the market through 2026 and beyond:

Helicopter Crash Resistance Seats Market

- Standards-driven demand: Dynamic crash requirements and evolving occupant injury criteria drive technology adoption cycles. Compliance with FAA 14 CFR §27.562, EASA CS-27/29 dynamic test expectations, and military crashworthiness specifications is a persistent procurement threshold for both civil and defense buyers.

- Technology substitution: Advances in cellular composite energy absorbers and carbon-fiber structural integration are enabling meaningful weight reductions while preserving or improving impact performance. These materials also shift value from raw material sourcing to design and validation capability.

- Aftermarket modernization: Retrofit and STC-based upgrade markets are accelerating as operators extend platform service life and prioritize occupant survivability. Speed-to-certify and ease-of-installation are key commercial levers.

Competitive landscape — what differentiates winners

The market comprises established aerospace seating specialists, materials innovators, and agile aftermarket integrators. From our company-level review, several competitive archetypes emerge:

- Heritage OEMs with deep certification pedigree: Companies with long-standing certifications and military program experience are advantaged when platforms require rigorous compliance frameworks. Their strengths are multi-tier program management, integrated systems experience, and proven energy-absorption architectures.

- Materials and subsystem innovators: Suppliers focused on energy-absorbing composites and cellular structures provide disruptive component-level improvements (lower weight, controlled stroke, repeatable attenuation) that incumbent seat manufacturers increasingly integrate through partnerships or acquisition.

- Aftermarket retrofit specialists: Firms delivering Supplemental Type Certificates (STCs) and field-proven upgrade kits capture value in the installed base. Their route to market depends on a tight coupling of certification know-how and service network reach.

Representative players across these archetypes include long-tenured seat manufacturers and materials firms who are actively shaping today’s product roadmaps and certification pipelines. Recent notable developments underscore the momentum: aftermarket STCs for mainstream rotorcraft, defense contracts for next-generation absorbers, and ongoing validation programs with service branches. These moves reflect a market where certification progress and demonstrable field performance materially influence tender outcomes.

Regulatory and materials context — constraints and levers

Three regulatory and materials realities should be central to 2026 strategies:

- Certification timelines are strategic timelines: Meeting dynamic crash test criteria is resource- and time-intensive. Program slippage often stems from late-stage test failures or incomplete documentation. Firms that invest in pre-test simulation fidelity and early engagement with authorities reduce time-to-field and mitigate cost overruns.

- Raw material pressure: Aerospace-grade aluminum honeycomb and high-modulus carbon fiber have experienced price movements and capacity constraints. While composites offer weight advantages — enabling up to a quarter of structural weight reduction in some seat architectures — supply risk and tooling costs must be factored into total lifecycle economics.

- Military standards maintain a premium: Meeting MIL-STD crash thresholds demands heavier-duty solutions and extended qualification cycles. Suppliers that can modularize military performance into scalable products for civil markets will capture cross-segment synergies.

What the report contains — practical chapters for decision-makers

Our full report is organized as an operational playbook for 2026 decisions. Key actionable sections include:

- Market sizing and base-case/alternative forecasts through 2032, with sensitivity to material prices and fleet utilization assumptions.

- Regulatory roadmap and certification stress tests — mapping timelines, typical failure modes, and mitigation strategies for FAA, EASA, and MIL frameworks.

- Supply-chain heat maps — identifying single-source risks, lead-time drivers, and alternative material qualification pathways.

- Competitive benchmarking — capability matrices that assess certification capacity, program delivery track record, and aftermarket penetration.

- Go-to-market frameworks for OEMs and aftermarket providers — including pricing playbooks, retrofit channel economics, and licensing/STC strategies.

- Investment decision tools — NPV and risk-adjusted returns for common product strategies (certified OEM seat lines, retrofit kits, materials R&D partnerships).

Each section combines quantitative scenario outputs, primary interviews with program managers, and validation against recent certification and contract events. Importantly, the full dataset behind our segmentation and model runs is accessible in the report; this briefing highlights the strategic takeaways while reserving the proprietary tables and regional/application-level breakdowns for subscribers.

Strategic recommendations for 2026

Based on our analysis, PW Consulting recommends differentiated actions depending on organizational role:

- OEMs and Tier‑1 suppliers: Prioritize modular architectures that decouple energy-absorbing elements from platform-specific interfaces. This reduces per-model certification overhead and accelerates aftermarket retrofit programs. Establish dual-sourcing for critical absorber cores and invest in high-fidelity pre-test simulation to shorten certification cycles.

- Aftermarket specialists: Scale STC pipelines by standardizing installation interfaces and developing turn-key field-support packages. Partnerships with seat OEMs for co-branded upgrade solutions can unlock fleet-level procurements.

- Materials innovators: Target collaborative validation programs with seat OEMs and military labs. Demonstrating repeatable, test-verified attenuation in live certification events is the fastest path from lab to contract.

- Procurement & defense planners: Incorporate lifecycle cost modelling that weighs certification cadence, retrofit scalability, and survivability benefits. For modernization programs, require modularity clauses to enable future materials upgrades without full-seat recertification.

Decision support for 2026 — what to look for next

As firms calibrate budgets and R&D roadmaps for 2026, watch for three high-leverage signals:

- Acceleration of STC approvals for mid-size platforms — this foreshadows aftermarket conversion velocity.

- Large-scale composite absorber qualification milestones — these indicate when weight-driven total-cost-of-ownership advantages become realizable.

- Shifts in supplier concentration or vertical integration moves among top players — such changes affect bargaining power and access to certified subassemblies.

Conclusion and how to access the full analysis

PW Consulting’s full Helicopter Crash Resistance Seats Market report consolidates proprietary forecasts, supplier scorecards, certification trackers, and decision tools designed to inform 2026 capital and program choices. The market’s mid-single-digit CAGR and moderate consolidation create attractive opportunities — but success depends on mastering certification complexity, mitigating material supply risk, and aligning product modularity to fleet realities.

To review the detailed segment tables, regional forecasts, and model assumptions that underpin these insights, please visit our official report page. The downloadable report and accompanying datasets provide the granular inputs and scenario models teams need to build executable 2026 strategies.

For detailed analysis of this topic, please visit the official page:Helicopter Crash Resistance Seats Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com