India R-134a Refrigerant Market Growing at 3.3% CAGR Through 2032

Other |

2026-06-27 13:29:41

PW Consulting’s latest market research on Multiaxial Optical Position Sensors offers a focused playbook for executives planning capital allocation, product roadmaps, and M&A strategies in 2026. Built on a base year of 2025 and a seven‑year forecast horizon through 2032, the report quantifies a clear expansion trajectory: the global market grew from approximately USD 325 million in 2020 to USD 450 million in 2025 and is forecasted to expand at a compound annual growth rate (CAGR) of 6.7% during the 2026–2032 period. By 2032, our baseline projection places the market at roughly USD 709 million. These headline numbers frame a structurally growing market that remains both specialized and strategically consequential for automation, semiconductor, aerospace, and mobility ecosystems.

Multiaxial Optical Position Sensor Market

Systems integration is accelerating. As factories, vehicles, and critical infrastructure demand more precise multi‑axis positioning, optical sensors have moved from component status to system enabler—embedding optics, electronics, and software to deliver deterministic motion control.

Multiaxial Optical Position Sensor Market

Regulatory and safety mandates are amplifying demand. Tighter automotive safety standards and expanded environmental monitoring requirements are increasing the need for certified, high‑reliability position sensing.

Multiaxial Optical Position Sensor Market

Supply chain and geopolitical frictions are real. Shortages in high‑purity silica and germanium and an intensified focus on sourcing resilience are already reshaping supplier strategies and capex plans—especially across key production hubs in Asia‑Pacific.

Forecast models and scenario analysis: interactive demand models covering the 2026–2032 window with upside/downside scenarios tied to semiconductor cycles, industrial automation adoption, and regulatory changes.

Technology roadmaps: comparative evaluation of lateral‑effect photodiode approaches, quadrant designs, CMOS/image‑sensor architectures and emerging direct Time‑of‑Flight (dToF) implementations—aligned to expected product lifecycles and system‑level ROI.

Procurement and supply‑risk playbook: supplier scorecards, lead‑time stress tests, and recommended contracting constructs that mitigate exposure to critical raw‑material shortages.

Competitive and investment heatmaps: capability matrices and acquisition targets that highlight where to invest organically versus where to consider inorganic consolidation.

Go‑to‑market and integration templates: pricing models, total cost of ownership (TCO) calculators, and validation protocols tailored to factory automation, semiconductor OEMs, aerospace/defense, and mobility customers.

The sector combines specialty sensor manufacturers, diversified component houses, and automation vendors. The market shows a moderate degree of concentration—our analysis identifies a trio of leading players commanding a meaningful share of industry revenues, with the top five firms accounting for a clear majority of market influence. This structure creates a two‑tiered dynamic: incumbent strengths in channels, certification, and ruggedization, alongside nimble challengers that push innovation in optics, CMOS integration, and software‑defined sensing.

Micronor Sensors Inc. (Camarillo, California) brings proven fiber‑optic solutions for extreme and EMI‑rich environments. Its positioning in absolute fiber‑optic rotary sensors makes it a preferred supplier where immunity and longevity are priorities—critical for nuclear, medical, and some industrial niches.

SICK AG (Waldkirch, Germany) combines deep channel reach in factory automation with broad optical sensing portfolios, enabling rapid integration into production lines and machine tools. Their strength is systems‑level sales and application engineering.

AK Industries (France) focuses on precision encoders and draw‑wire measurements—appealing to OEMs requiring compact, mechanical‑to‑optical conversion in constrained form factors.

Honeywell International Inc. (Charlotte, North Carolina) leverages multi‑domain credentials in aerospace and industrial controls to bundle position sensing into higher‑margin control solutions and avionics subsystems.

ams‑OSRAM AG (Premstaetten, Austria) is a key component innovator, advancing high‑precision optoelectronics and recently showcased direct Time‑of‑Flight (dToF) capabilities that accelerate system miniaturization and range performance.

TE Connectivity (Schaffhausen, Switzerland) targets transport and harsh‑environment applications with ruggedized optical encoder platforms and global manufacturing scale.

Keyence Corporation (Osaka, Japan) is a go‑to for laser displacement and high‑accuracy optical positioning in manufacturing, differentiating through rapid deployment and application engineering support.

Recent product activity underscores a market pivot toward higher integration and range‑capable sensing: in 2025 Panasonic launched a targeted multi‑axial sensor line for industrial automation, while ams‑OSRAM and STMicroelectronics have advanced dToF‑based products, signaling that component‑level innovation is converging with system demands.

Raw materials: High‑purity silica and germanium supply constraints are a near‑term risk to APAC production capacity and could push lead times and component costs upward in 2026 unless firms secure diversified sources or invest in substitution strategies.

Regulation and certification: Escalating certification requirements in automotive and aerospace will favor suppliers with established test‑labs, documented change‑control, and designtime support—raising market entry barriers for new entrants.

Geopolitics and localization: Our region‑level analysis highlights that diversified sourcing and nearshoring are increasingly not optional—companies are advised to revisit supplier footprints, implement dual‑sourcing, and build buffer capacity for critical components.

Prioritize supply resilience: Immediately audit exposure to high‑purity silica and germanium, secure multi‑year contracts with tier‑1 suppliers, and evaluate material‑substitution pilots where feasible. Consider modest capex to localize critical assembly in lower‑risk jurisdictions.

Move up the stack: Differentiate through system integration—combine optics with edge compute and sensor fusion to sell higher‑value subsystems rather than components.

Invest in dToF and CMOS capabilities: Given recent launches and component trajectories, allocate R&D budget to time‑of‑flight and image‑sensor architectures that enable range and multi‑axis resolution improvements.

Adopt a portfolio approach to market entry: Use partnerships and targeted acquisitions to fill capability gaps quickly—particularly in calibration, software, and certification where time‑to‑market matters.

Align procurement with the forecast cadence: Use our 2026–2032 CAGR to inform inventory targets and procurement windows; the expected steady expansion supports staged capacity investments rather than large one‑off bets.

Prepare for consolidation and channel shifts: With a moderate concentration among top players, smaller firms should prioritize niche specialization or partner with larger integrators to maintain access to OEM channels.

Board and investment committees: Use the report’s scenario outputs to stress‑test capex requests and M&A propositions against alternative demand paths and raw‑material scenarios.

R&D and product management: Translate technology roadmaps into prioritized development sprints—target dToF/CMOS proof‑of‑concepts and system‑level interoperability tests in 2026 pilot programs.

Procurement and supply chain: Implement supplier performance KPIs and contingency playbooks informed by our supplier stress tests; execute dual‑sourcing where concentration risk is highest.

Sales and go‑to‑market: Reposition offerings around system reliability, lifecycle cost, and regulatory compliance to capture higher margin opportunities in regulated end markets.

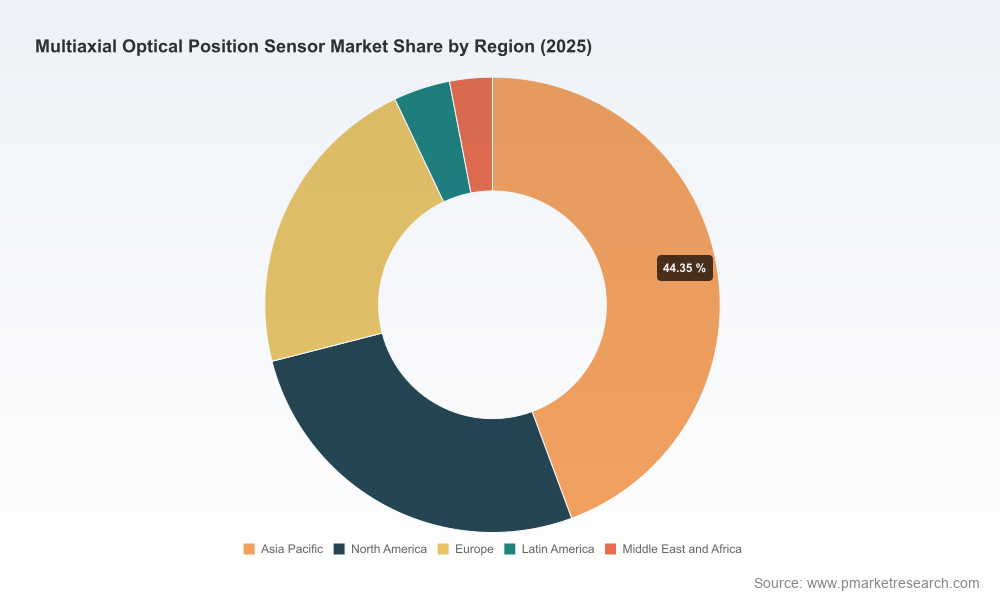

To preserve the integrity and commercial value of the full analysis, this summary omits detailed regional and application split figures, granular unit‑price trajectories, and line‑by‑line company revenue breakdowns. Those data, along with downloadable model files, supplier scorecards, and acquisition target dossiers, are available in the full PW Consulting report and online resource pack.

As optical position sensing evolves from component innovation to system differentiation, 2026 is a pivotal year for re‑setting strategies. The market’s projected steady growth (CAGR 6.7% through 2032) combined with material supply tensions and accelerating regulatory requirements creates both opportunity and risk. PW Consulting’s Multiaxial Optical Position Sensor Market report translates these dynamics into actionable choices: where to invest, what to insource, whom to partner with, and how to protect margins. For executives crafting resilient growth plans and defensible product roadmaps, the full report is the operational intelligence layer that converts market direction into executable strategy.

Access the full analysis, interactive models, and supplier dossiers on our website to obtain the detailed segmentation, granular forecasts, and tactical tools required for decisive 2026 planning.

For detailed analysis of this topic, please visit the official page:Multiaxial Optical Position Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com