Satellite Control Service Market — Strategic Imperatives for 2026 (PW Consulting Preview)

Executive snapshot

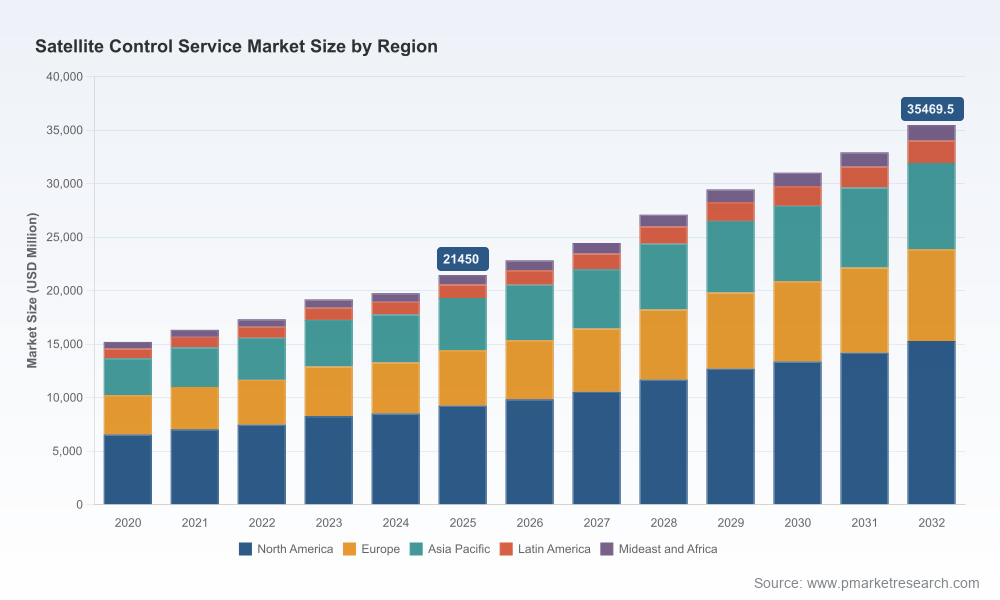

PW Consulting’s latest Satellite Control Service Market report frames a rapidly maturing segment that is becoming central to broader satellite value chains. After expanding from roughly USD 15.2 billion in 2020 to an estimated USD 21.45 billion in 2025, the market is forecast to grow at a compound annual growth rate (CAGR) of 7.45% over the 2026–2032 forecast window. By 2032, our model projects an addressable market north of USD 35 billion (USD Million basis). These headline figures underline structural demand for telemetry, tracking & command (TT&C), station-keeping, maneuvering and payload management services across commercial, government and scientific missions.

Satellite Control Service Market

Why this matters to 2026 decision-makers

- Budget prioritization: Mid-sized operators and new constellation entrants must reconcile steep ground-infrastructure CAPEX with service-level expectations; GSaaS (Ground-Station-as-a-Service) models are now a mainstream mitigation option.

- Market positioning: The market exhibits moderate consolidation — the top three suppliers control a meaningful share and the top-five share is a majority — creating differentiated bargaining power and partnership opportunities.

- Regulatory timing: A flurry of rule changes and legislative proposals in late 2025/early 2026 materially alters licensing, spectrum access and infrastructure timelines; the window for shaping implementation and entry strategy is short.

- Operational resilience: Multi-orbit operations, automated mission control, and resilient TT&C chains are emerging as minimum requirements for both revenue-bearing and safety-critical missions.

Market dynamics shaping the 2026 agenda

Several dynamics converge to make 2026 a pivotal year for satellite control services. First, the steady increase in satellite launches and multi-orbit architectures (LEO constellations, MEO systems, continued GEO relevance, and cusp-period HEO/lunar missions) amplifies demand for flexible, software-driven control services. Second, high initial CAPEX for antennas, RF chains and control software remains a defining barrier; shared and on-demand GSaaS approaches are being adopted to reduce capital lock-up and accelerate operational start-up.

Satellite Control Service Market

Third, regulatory shifts are compressing timelines and expanding addressable opportunities. In late 2025 the U.S. FCC advanced proposals to streamline licensing and potentially unlock tens of thousands of MHz for satellite broadband; in January 2026 a bipartisan legislative proposal sought to standardize foreign system market access and impose longer-term license parameters. Concurrently, EU and UK regulatory actions accelerated infrastructure approval flows and coexistence rules for direct-to-device services. For executives, this is a synchronous change cycle — windows for spectrum certainty, permitting and contractual terms will emerge quickly in early 2026 and be decisive for network rollout and procurement cadence.

Satellite Control Service Market

Finally, technology and operational shifts — cloud-native mission control, digital twins for satellite operations, automation in TT&C handovers, and hardened cybersecurity for command links — are eroding historical differentiation in raw infrastructure, shifting competition toward software, service-level guarantees, and integrated lifecycle support.

Competitive landscape — signals from the market leaders

The competitive map is diverse: ground-network specialists, legacy satellite operators, large systems integrators and defense primes, and cloud-native GSaaS entrants all jockey for position. The market’s concentration metrics indicate that the top three suppliers control a substantial portion of spend, while the top five control a majority — a balance that enables scale players to protect margin but still leaves scope for specialized and regionally-focused entrants.

- KSAT (Kongsberg Satellite Services) — Reinforcing its high-reliability ground-network credentials, KSAT’s continued network expansion supports multi-orbit and lunar missions. Strategy implication: partnership opportunities for operators seeking robust TT&C redundancy and rapid onboarding of non-native payloads.

- SES, Intelsat, Eutelsat, Telesat — Large fleet operators offer integrated flight-ops and lifecycle services; Telesat’s recent financial updates signal operational stability and a focus on managed services. Strategy implication: incumbents leverage fleet control and bundled services to defend share; challengers must outcompete on cost-per-contact and SLA agility.

- Viasat — The firm’s five-year contract renewals for managed connectivity demonstrate defense and government stickiness; managed-network credentials translate well into end-to-end control propositions. Strategy implication: target dual-use contracts and position TT&C offers as mission-enabling, not transactional.

- System integrators and defense primes (Lockheed Martin, Airbus Defence and Space, Kratos, L3Harris, General Dynamics, RTX) — These players bring deep mission-systems expertise and often sit at the intersection of government procurement and complex commercial missions; they are natural partners for high-assurance or classified control environments.

- GSaaS and ground-network newcomers (Atlas Space Operations, Leaf Space, RBC Signals, and others) — These entrants prioritize API-first, on-demand access and global coverage via partner ground-station footprints. Strategy implication: incumbents must defend margins by modularizing offerings and competing on integration speed and developer experience.

- Infrastructure deployments and market signals — Recent infrastructure deployments by key gateway operators underscore continued investment in ground capacity and redundancy; contract renewals with defense customers signal long-term revenue streams for providers oriented to managed services.

Operational playbook — seven actions for 2026

- Re-evaluate ownership vs. outsourcing: Run a 3–5 year cash-flow analysis comparing in-house ground infrastructure to GSaaS subscriptions, factoring in regulatory timing, spectrum risk and SLA exposure.

- Design for multi-orbit control: Mandate TT&C architectures that support rapid re-tasking across LEO/MEO/GEO and common ground APIs to lower integration cycles.

- Prioritize automation and AI ops: Invest in automated anomaly detection, automated handovers between ground nodes, and predictive fuel/propellant modeling to reduce operations costs and mission risk.

- Embed security-by-design: Command-link hardening, cryptographic key management and operating-environment segregation must be procurement prerequisites for any control service contract.

- Engage regulators early: Use the compressed policy windows of 2026 to shape spectrum and licensing outcomes; coordinate consortium responses where possible to reduce time-to-market uncertainty.

- Pursue modular partnerships: Combine strengths across hosts (antennas), software, and managed services to deliver tailored, SLA-backed packages without full-capex exposure.

- Prepare M&A and JV playbooks: With market concentration favoring scale, prepare transaction templates for tuck-ins that extend global coverage, software IP, or classified-capable operations.

What the PW Consulting report delivers (practical intelligence)

This report is built for hands-on decision-making. Core assets include:

- A transparent market model (historical 2020–2025 and forecast 2026–2032) with scenario-tested sensitivities for launch cadence, GSaaS adoption rates and regulatory timelines.

- Vendor scorecards and sourcing guidance that evaluate reliability, geographic reach, SLA history, security posture and commercial terms.

- Go-to-market playbooks for operators, prime contractors and ground-service specialists, including commercial templates, contract negotiation levers and recommended KPIs for TT&C and payload operations.

- Operational blueprints for multi-orbit mission control, automation adoption roadmaps and cybersecurity checklists tailored to command-and-control chains.

- M&A and partnership diligence checklists, plus a short-list of tuck-in capabilities that accelerate market access in 12–24 months.

- A regulatory timeline and stakeholder map reflecting the late-2025 and early-2026 rule movements that materially affect licensing, spectrum and infrastructure deployment windows.

Note: this preview purposefully omits granular segment-level tables and regional/application splits. The full report contains the complete dataset, detailed segment revenues, and per-company benchmarking that are essential for transaction-level decisions.

Implications for investors and corporate leaders

Investors should treat the satellite control services market as a growth market with durable tailwinds but execution-sensitive returns. Regulatory acceleration and defense contract stickiness reduce certain market risks; the primary value-at-risk is operational execution (on-time ground deployments, software reliability) and the ability to secure spectrum and licensing windows. For corporate leaders, the immediate 2026 priority is constructing an operating model that balances ownership of mission-critical control functions with scalable, third-party services for non-core contacts.

Conclusion — how to use this preview

2026 is a strategic inflection point for companies operating in or adjacent to satellite control services. PW Consulting’s market analysis provides the operating guidance, vendor assessments and regulatory context needed to make pragmatic choices: where to invest, what to outsource, which partners to prioritize, and how to structure commercial terms that protect margins while enabling scale. For detailed segment-level forecasts, vendor benchmarking matrices and transaction-ready diligence materials, access to the full report and dataset is required — this preview demonstrates the type of actionable insight you will receive and where to focus your near-term strategic moves.

PW Consulting — strategic counsel for executives shaping the future of satellite operations. Contact our research desk to request the full Satellite Control Service Market report and model (subscription required).

For detailed analysis of this topic, please visit the official page:Satellite Control Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com