Gallium Nitride Semiconductor Device Industry Growth Accelerated by Advanced Power Electronics and Next-Generation Communication Technologies by 2031

Other |

2026-04-07 10:44:57

PW Consulting’s latest High Precision Copper Foil Market study provides a practice-oriented, decision-ready vantage for corporate leaders preparing strategic moves in 2026. Anchored on a detailed base year analysis of 2025 and a seven-year forecast (2026–2032), the report synthesizes macro trajectories, supply-chain stress points, and competitive dynamics into a focused playbook for procurement, product planning, and M&A. This release previews the report’s most consequential insights — demonstrating our depth while reserving the granular segment matrices and price curves for the full study.

High Precision Copper Foil Market

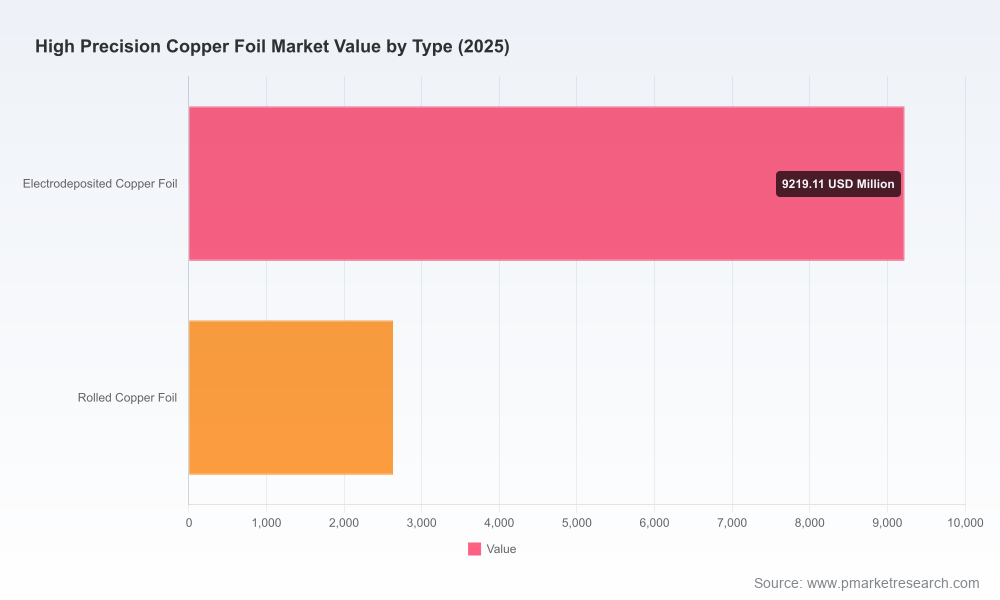

The market for high precision copper foil has transitioned from steady electronic-industry demand to a multi-driver growth story. Our base-year assessment for 2025 places the global market at approximately USD 11.85 billion, reflecting the recovery and reinvestment cycles across electronics, batteries and advanced interconnects. Looking forward, PW Consulting projects the market to expand at a compound annual growth rate (CAGR) of 8.64% through 2032, crossing roughly USD 21.17 billion by the end of the forecast horizon. The underlying momentum is supported by structural drivers — miniaturization in high-density interconnects, battery-grade foil for electrified mobility, and specialized low-roughness foils for high-frequency and AI-accelerator applications.

High Precision Copper Foil Market

Historical context matters: between 2020 and 2025 the market more than doubled in scale, underscoring both cyclical recovery and structural reallocation of materials into higher-value, precision applications. That same dynamism is the source of both opportunity and operational risk for 2026 planners.

High Precision Copper Foil Market

The high precision copper foil arena is led by a mix of legacy metallurgical groups and specialized technology players. Market concentration indicators show a meaningful share held by top firms while leaving room for agile challengers to carve niches. Key companies profiled in our analysis include established Japanese producers known for proprietary surface technologies, European and North American rolled-foil specialists with strict surface and dimensional controls, and several Asian players that combine scale with rapid product customization.

Recent commercial moves illustrate the evolving dynamic: supplier price adjustments in early 2026 and capacity increments announced in late 2025 signal a market where demand-pull and cost-push forces are colliding. Our report includes an actionable competitive scorecard and scenario plans outlining likely competitor reactions to different price and demand scenarios.

Two raw-material realities are shaping 2026 strategy. First, copper cathode prices reached historic peaks in early 2026, creating immediate margin pressure for foil producers and prompting supplier price actions. Second, countervailing pressures upstream — including low smelter treatment and refining charges — are complicating supply economics and may constrain incremental capacity in some regions.

Geopolitical and regional concentration factors further complicate planning. The global distribution of production capacity is skewed, making exports, tariffs, and domestic operating rates decisive variables. Environmental policy — notably in countries with aggressive decarbonization roadmaps — is already raising operating costs for electrolytic production and accelerating adoption of recycled copper and renewable energy inputs.

In keeping with our “trailer” principle, the report demonstrates PW Consulting’s analytical depth and provides sample outputs; however, detailed regional and application segment matrices, the full set of supplier price curves, and the interactive financial models are reserved for subscribers and clients who download the complete document.

For executives whose 2026 playbooks hinge on securing advanced interconnect performance, battery-grade materials, or margins in a cost-volatile environment, our High Precision Copper Foil Market report is structured to convert industry knowledge into executable strategy. By combining market-scale projections, supplier intelligence, and operationally focused recommendations, PW Consulting equips leaders to prioritize investments, protect margins and move quickly when market windows open.

To access the full dataset, supplier price curves and the interactive scenario models that underpin these conclusions, please download the complete report from PW Consulting’s market research portal or contact our advisory team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:High Precision Copper Foil Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com