Polyurethane Adhesive for Shoes Market — Strategic Outlook for 2026: PW Consulting Perspective

Executive summary

PW Consulting’s latest market study on Polyurethane Adhesive for Shoes (base year 2025) delivers a practical, decision-ready blueprint for executives planning 2026 actions. The global market reached approximately USD 1,795 million in 2025 and — under our baseline scenario — is projected to expand to roughly USD 2,673 million by 2032, reflecting a compound annual growth rate (CAGR) of 5.85% over the forecast window (2026–2032). Market concentration is meaningful but not prohibitive: the three- and five-firm concentration ratios indicate incumbent suppliers command a significant share while leaving room for regional specialists and technology challengers.

Polyurethane Adhesive For Shoes Market

Why this report matters for 2026 decision-making

- Translates macro trends — raw material volatility, regulatory tightening, and rapid product innovation in footwear — into actionable procurement and R&D priorities.

- Combines a quantitative growth model with scenario stress tests (tariffs, isocyanate price shocks, accelerated sustainability adoption) so leadership can quantify margin and capex impacts before committing resources.

- Provides operational playbooks for converting production lines to water-based or hot-melt PU adhesive systems, including labor, energy and CAPEX implications.

- Benchmarks supplier capabilities and sustainability credentials to accelerate supplier selection, qualification and onboarding cycles.

Key market dynamics shaping footwear adhesive strategies in 2026

- Raw material price volatility. Prices for primary isocyanates (MDI, TDI) and polyols remain sensitive to crude oil swings and geopolitical shocks. Our model quantifies margin erosion at different feedstock price trajectories and recommends hedging and contract structures that preserve gross margin through 2026.

- Regulatory push toward low-VOC and water-based systems. REACH updates and decarbonization initiatives tied to the European Green Deal are accelerating footwear makers’ shift away from solvent-based adhesives. This structural trend is compressing the window for legacy solvent formulations and reshaping R&D pipelines.

- Sustainability as a procurement filter. Adoption of bio-based polyols and certifications (low-VOC, hydrolysis resistance, eco-labels) is rapidly moving from “nice-to-have” to commercial procurement prerequisites for major brands. Suppliers with demonstrable bio-content and life-cycle data are gaining faster adoption in brand-spec programs.

- Trade and tariff risk. Recent changes in tariffs on polyols and isocyanates in several markets have raised landed costs for certain formulations. Our regional risk matrix highlights which sourcing strategies and localization moves materially reduce landed cost volatility.

- Technology and process shifts. Hot-melt polyurethane (PURHM) and advanced waterborne PU dispersions are being used to reduce production steps, energy consumption and labor on high-volume sports and performance footwear lines — creating both CAPEX demand and a supplier competitive edge.

Competitive landscape — what leading suppliers are signaling

The market features a mix of global chemical majors, specialty formulators, and regional innovators. Established players are leveraging portfolio breadth and R&D scale to push waterborne and hot-melt solutions, while regional specialists compete on hydrolysis resistance, cost-to-apply, and local service. Recent vendor moves illustrate strategic themes investors and OEMs should track:

Polyurethane Adhesive For Shoes Market

- Portfolio modernization: Global adhesives leaders continue to highlight hot-melt and water-based PU systems that reduce production steps and energy use, emphasizing suitability for complex modern footwear substrates.

- Sustainability differentiation: Several firms have extended bio-based TPU and lower-VOC product lines, using both formulation innovation and certification to shorten procurement cycles with major brands.

- Regional positioning: Experienced regional manufacturers are reinforcing supply chains and product-fit with local OEM practices — an advantage where tariff or logistics risk favors near-sourcing.

- Product launches and positioning: Recent activity includes thermoplastic polyurethane (TPU) lines for solvent-based adhesives, bio-based TPU for hot melt, and market positioning by thermoplastic specialists — indicating an increasingly nuanced competitive set where materials innovation matters as much as price.

PW Consulting’s full report contains vendor scorecards and a strategic heatmap that aligns capability, innovation momentum and commercial risk for the market’s leading suppliers.

Polyurethane Adhesive For Shoes Market

What the PW Consulting report delivers (practical scope)

- Quantified market sizing and forecasts (historical 2020–2025; forecast 2026–2032) with scenario overlays for raw material shocks, accelerated sustainability adoption and tariff changes.

- Supply-chain and margin sensitivity models that allow users to run custom inputs for MDI/TDI/polyol price moves and see impacts on gross margin, required price increases and payback for process conversion investments.

- Regulatory impact analysis mapping REACH and other regional rules into compliance costs and recommended formulation roadmaps.

- Go-to-market playbooks for formulators and adhesive manufacturers: product roadmap sequencing, pilot line conversion checklists, and industrial validation protocols aligned to footwear OEM qualification cycles.

- Commercial tools — supplier shortlists, RFP templates, and procurement negotiation strategies designed to secure multi-year supply at predictable terms.

- Competitive benchmarking, including technology positioning, sustainability credentials, and near-term product pipeline intelligence (company-level profiles and recent developments summarized).

Actionable priorities for 2026 — 90-day and 12-month checklists

- For adhesive manufacturers and formulators

- 90 days: Run the PW Consulting sensitivity model with your supplier contracts to identify immediate margin at-risk and prioritize raw-material hedges or fixed-price extensions.

- 12 months: Deploy a pilot water-based or PURHM line and secure two anchor brand trials targeting reduced VOC/spec-improvement claims.

- For footwear brands and OEMs

- 90 days: Issue updated material specifications favoring low-VOC and bio-based claims; begin supplier pre-qualification on sustainability metrics.

- 12 months: Consolidate to a smaller set of strategic adhesive suppliers with joint NPD roadmaps that reduce total cost-of-assembly and environmental footprint.

- For raw-material suppliers

- 90 days: Assess product conversion feasibility to bio-based polyols and quantify expected uplift in OEM procurement preference.

- 12 months: Invest in small-scale, rapid-qualification programs that shorten customer adoption cycles and reduce technical objections tied to hydrolysis and flexibility performance.

- For investors and M&A teams

- 90 days: Use concentration and capability maps to identify regional specialists with strong brand relationships and eco-certified portfolios as potential bolt-on targets.

- 12 months: Target assets that combine process IP (e.g., hot-melt application specialization) with established OEM approvals to accelerate roll-up synergies in a market growing at mid-single-digit CAGR.

How to put the model to work

PW Consulting delivers an interactive Excel-backed model and a cloud dashboard that let you stress-test assumptions: change raw material price paths, simulate rapid regulatory tightening or fast-track sustainability adoption, and see how those inputs alter revenue, margin and break-even timing for conversion investments. The modeling suite is deliberately built to support board-level decision cycles and procurement negotiations in 2026.

Next steps — where to find the granular intelligence

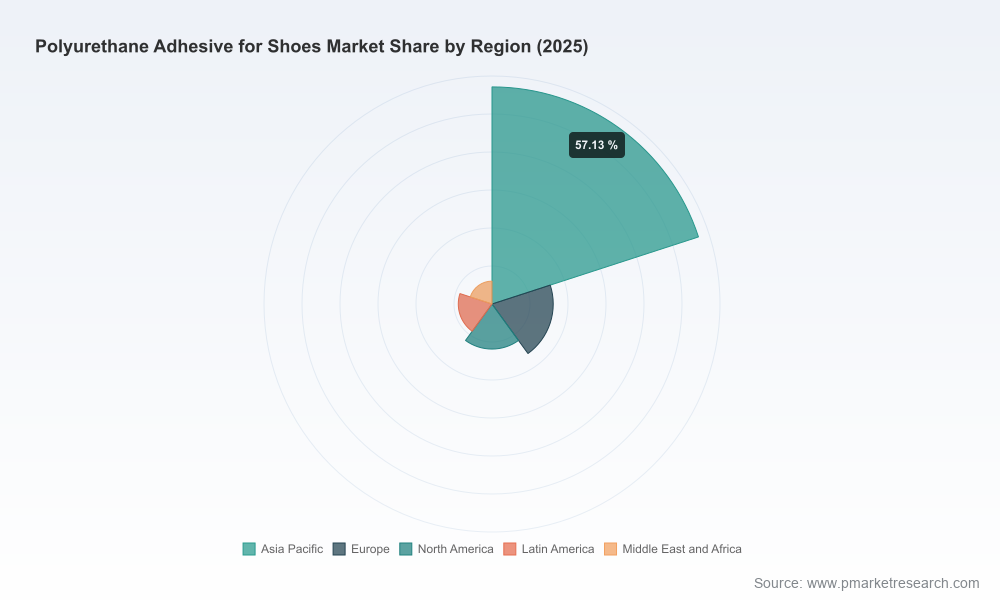

This release outlines the strategic implications and core tools included in PW Consulting’s full market study. In order to preserve proprietary commercial utility and to honor primary-source confidentiality, the press summary intentionally omits detailed regional, type and application splits — the very segmentation data and company-level financials that procurement, R&D and M&A teams rely on for operational decisions. The complete report includes the full dataset, downloadable models, granular regional and application splits, supplier scorecards and raw material price-path scenarios.

To assess how the 2026 landscape will affect your sourcing, product development and capital plans, download the full Polyurethane Adhesive for Shoes Market report and the interactive model from PW Consulting’s research portal. The full deliverable equips leadership with the quantitative and tactical resources required to convert 2026 market dynamics into defensible commercial advantage.

For detailed analysis of this topic, please visit the official page:Polyurethane Adhesive For Shoes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com