Disposable Hemoperfusion Cartridge Market: Strategic Intelligence Briefing for 2026 Decision-Makers

Executive summary

PW Consulting’s new market intelligence brief on the Disposable Hemoperfusion Cartridge Market delivers actionable guidance for executives, investors, and clinical leaders preparing strategic moves in 2026. Built on a 2020–2025 historical foundation and a 2026–2032 forecast horizon, the study quantifies a resilient market trajectory (a compound annual growth rate of approximately 9.02%) and translates that growth into pragmatic choices around product portfolios, regulatory pathways, manufacturing scale-up, and go-to-market models.

Disposable Hemoerfusion Cartridge Market

Why this market matters in 2026

Disposable hemoperfusion cartridges sit at the intersection of acute critical care, nephrology, and organ-support therapeutics. Accelerating clinical interest in cytokine modulation, expanded use cases in sepsis and perioperative cardiac care, and renewed regulatory attention to sorbent technologies have collectively pushed disposable hemoperfusion from a niche adjunct to an investable, strategic product line for device manufacturers and hospital systems. Our analysis shows a market that has expanded materially since 2020 and is expected to continue growing across the forecast period—creating opportunities for incumbent consolidation and new entrants who can demonstrate clinical differentiation and supply reliability.

Disposable Hemoerfusion Cartridge Market

What PW Consulting’s report delivers

- Quantified market sizing and scenario forecasts (base year 2025; historical 2020–2025; forecast 2026–2032) with sensitivity testing for regulatory and reimbursement inflection points.

- A competitive landscape that profiles global leaders, regional champions, and specialized innovators—covering product portfolios, manufacturing footprints, regulatory status, and commercialization strategies.

- Commercial playbooks: targeted go-to-market options by hospital segment, distributor strategies, and tender/contracting approaches for public and private systems.

- Regulatory and HTA roadmaps: stepwise pathways for U.S. De Novo/PMA strategies, EU conformity and notified-body considerations, and country-level reimbursement levers in priority markets.

- Technical and clinical adoption frameworks: evidence generation plans, trial design advice for perioperative and sepsis indications, and bundling strategies with continuous renal replacement therapy (CRRT) and extracorporeal circuits.

- Manufacturing and supply-chain playbook: capacity planning templates, risk-mitigation strategies for critical resin suppliers, and audit-ready production checklists for cleanroom expansion.

Macro picture: growth, concentration, and what it implies for strategy

The disposable hemoperfusion market has demonstrated steady expansion through 2025 and is projected to grow at roughly a mid-single- to high-single-digit CAGR into the early 2030s. This trajectory reflects a combination of organic clinical adoption, expanding indications (from intoxication and renal failure adjuncts to cytokine and intraoperative applications), and iterative regulatory clarity in several jurisdictions.

Disposable Hemoerfusion Cartridge Market

A relatively concentrated supplier landscape—where a small group of firms account for the majority of revenue—creates both barriers and levers. For incumbents, concentration supports margin preservation and scale advantages in clinical evidence generation. For challengers, targeted clinical niches, differentiated chemistry or pore-size control, and partnership models with perfusion/device OEMs create viable paths to rapid scale without competing head-on across every indication.

Competitive dynamics: profiles and strategic implications

Our report examines the full competitive set, from global medical device multinationals to specialty sorbent specialists and regional cartridge manufacturers. Highlights from the company-level analysis:

- Jafron Biomedical: A vertically integrated player with a broad HA series portfolio and automated production lines. Their resin-based approach with defined pore-size distributions (product family variants targeted at different molecular-size ranges) and large-scale manufacturing capacity are core strategic advantages—enabling rapid supply response and competitive pricing in volume markets. Their recent regulatory progress in North America signals a deliberate push beyond established regional strongholds.

- CytoSorbents Corporation: A technology-led competitor focused on polystyrene-divinylbenzene sorbents with substantial clinical adoption in Europe and investigational programs in the U.S. Recent moves—such as multi-cartridge usage (HotSwap), distribution renewals in key European markets, and active regulatory engagement for device de novo pathways—underscore a strategy to expand both clinical indications and procedural settings (cardiac surgery, organ perfusion).

- Foshan Biosun, Baihe, DiaCare Solutions and other regional specialists: These firms combine sterile single-use product designs with cost-competitive manufacturing and regional distribution strengths. Their play often centers on pairing with dialysis providers and leveraging local procurement channels to capture high-volume hospital business.

- Large diversified medical groups (e.g., Baxter, Toray/Asahi Kasei, Kaneka): These companies bring legacy adsorbent/carbon expertise, established relationships in acute care, and integrated delivery propositions—particularly attractive for hospital systems seeking vendor consolidation across blood purification modalities.

Regulatory and clinical dynamics shaping competitive advantage

Regulatory nuance is a strategic factor. Ongoing dialogues with U.S. regulators around reclassification for certain sorbent device use-cases, coupled with jurisdictional differences in evidence requirements, mean that targeted regulatory strategies can materially alter time-to-market and reimbursement potential. For instance, polymyxin B immobilized fiber cartridges (PMX) and other endotoxin-targeted devices follow different evidentiary paths than broad-spectrum cytokine adsorbers—necessitating bespoke clinical programs and HTA tactics.

Clinical adoption is likewise conditional on evidence that connects device use to meaningful outcome improvements or clear process efficiencies (reduced ICU days, transfusion avoidance, decreased vasoactive drug use). Our fieldwork shows that hospital purchasing committees weight robustness of randomized or registry evidence, operator training burden, and disposables cost per case—factors that must inform pricing and clinical trial investment decisions.

Practical recommendations for 2026 strategic moves

- Prioritize indication-anchored commercialization. Select one or two clinical settings (e.g., cardiac perioperative hemostasis/antithrombotic-removal or severe septic shock cytokine modulation) for concentrated evidence generation rather than broad, unfunded indication expansion.

- Design regulatory playbooks that de-risk the U.S. timeline. Early pre-submission engagement, targeted pivotal endpoints aligned with FDA expectations, and staged market entry strategies (EU first, then U.S., with parallel real-world evidence collection) shorten commercialization cycles.

- Invest in interoperable systems and clinician training. Products that integrate cleanly with CRRT circuits or perfusion sets and require minimal operator change are adopted faster and face fewer reimbursement headwinds.

- Harden supply chains now. Sorbent resin quality and cleanroom manufacturing are non-trivial to replicate—strategies should include secondary sourcing of key polymers, contractual capacity with regional manufacturers, or incremental investment in automated cleanroom expansion.

- Consider strategic partnerships over internal build when appropriate. Distribution alliances, OEM supply agreements with CRRT vendors, or co-development relationships with academic centers can de-risk market entry while preserving upside through licensing or co-commercialization terms.

Report use cases: how executives should apply the analysis

Executives can extract concrete value from the report across four immediate uses:

- M&A screening: Use the report’s market maps and company profiles to target acquisition candidates whose clinical evidence and manufacturing footprint fill specific gaps in a buyer’s portfolio.

- R&D prioritization: Align product development trade-offs (pore-size engineering, cartridge geometry, duration-of-use) with modeled revenue outcomes under multiple reimbursement scenarios.

- Commercial investments: Allocate sales force, KOL engagement, and registry funding to the indications that maximize near-term ROI according to our scenario outputs.

- Operational planning: Calibrate capacity expansions and supplier contracts to manageable ramp profiles that match forecasted demand in our base and upside scenarios.

Data confidentiality and where to find the full intelligence

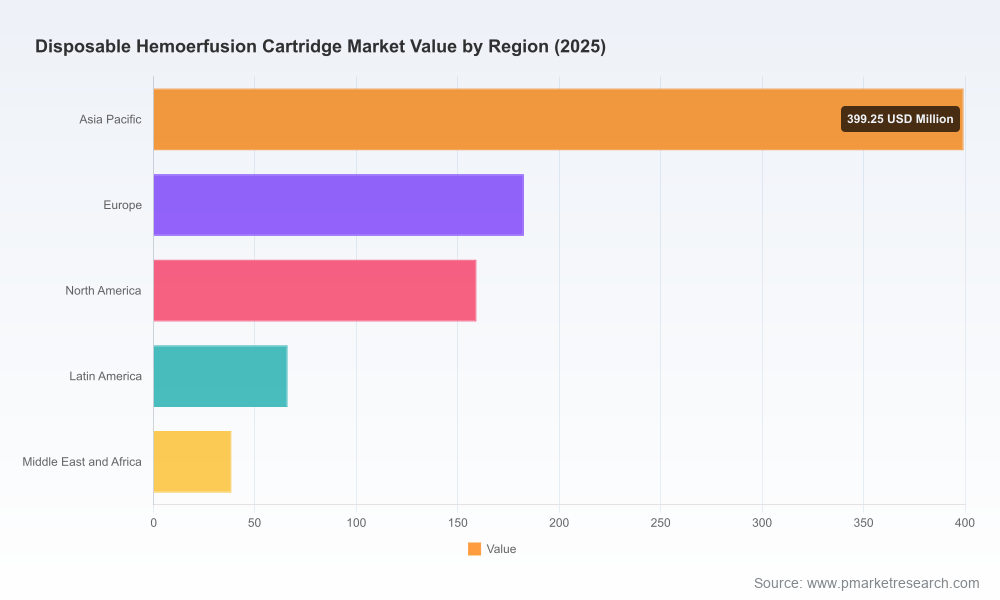

This briefing intentionally presents the strategic contours and actionable guidance while withholding granular segment-by-segment revenue tables and precise regional/application splits—information that our clients rely on for transaction diligence and competitive maneuvers. The full report contains detailed breakdowns by region, material type, and clinical application, plus downloadable financial models and vendor scorecards. Interested parties are encouraged to access the complete dataset and appendices via the PW Consulting research portal.

Closing perspective

By 2026, disposable hemoperfusion cartridges present a higher-stakes, lower-latency opportunity relative to many adjacent consumable markets. The combination of solid market growth, concentrated incumbency, and definable regulatory inflection points creates a strategic window for firms that can combine clinical validation with manufacturing reliability. PW Consulting’s report equips decision-makers with the scenario-tested insights, commercial playbooks, and regulatory roadmaps they need to act decisively while maintaining optionality across the forecast horizon.

For detailed analysis of this topic, please visit the official page:Disposable Hemoerfusion Cartridge Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com