Earth Observation Market Expands Remote Sensing Services

Other |

2026-02-24 06:31:45

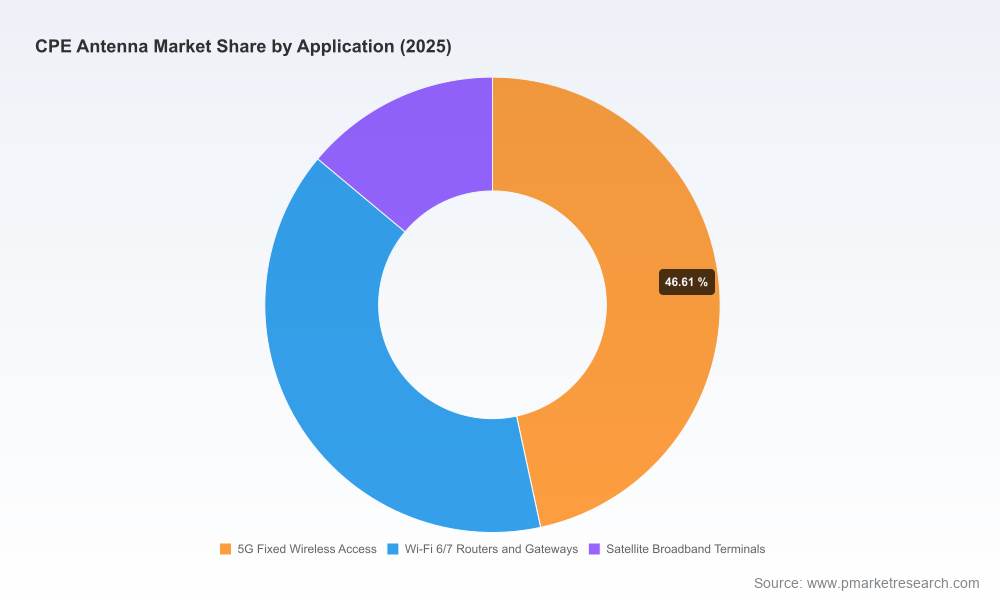

As service providers, device OEMs and infrastructure investors rework capital plans for the coming 24 months, antenna performance and CPE architecture will be decisive vectors of competitive differentiation. PW Consulting’s new Cpe Antenna Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides the scenario-driven intelligence executives need to translate network opportunity into durable value. Our modelling shows the addressable CPE antenna market expanding from roughly USD 1.58 billion in 2025 to an expected USD 2.76 billion by 2032 — a compound annual growth rate of 8.27% across the forecast horizon. This preview explains why that growth matters for boardroom decisions in 2026, what levers will determine winners, and how to use the full report to convert insight into action.

Cpe Antenna Market

Prioritizing CapEx and R&D: With mid‑band spectrum releases and next‑generation Wi‑Fi rollouts accelerating, antenna choices now materially affect network economics. Our analysis quantifies how design choices (integrated vs. external, high‑gain vs. multi‑element AI arrays) change TCO for FWA and carrier‑grade CPE across multiple deployment scenarios.

Cpe Antenna Market

Supplier and design selection: Hardware procurement decisions made in 2026 will lock in compatibility and upgrade paths for several years. The report’s supplier benchmarking and technology scorecards let procurement teams short‑list partners with the highest probability of meeting throughput, reliability and lifecycle requirements.

Cpe Antenna Market

Regulatory risk management: Recent regulatory activity — from spectrum repurposing proposals to shifts in service classification — can reframe spectrum economics. Our regulatory scenarios translate policy shifts into quantifiable impacts on coverage economics and vendor roadmaps.

Investment screening: For corporate development and private equity teams, the report converts product wins and IP strength into differentiated valuation indicators, isolating which companies are positioned to capture disproportionate share as the market consolidates.

5G Fixed Wireless Access (FWA) maturation: Operators are increasingly treating FWA as a strategic broadband anchor rather than a stopgap. Advances in CPE antenna arrays and beam management are extending cell reach and improving spectral efficiency, which raises the addressable market for higher‑performance CPE.

Wi‑Fi evolution at the edge: Wi‑Fi 6/7 inside home gateways and next‑generation fiber gateways demand embedded antenna designs that balance throughput with radiated efficiency. Design wins with tier‑one gateway OEMs are creating multi‑year revenue streams for antenna specialists.

Spectrum and regulation: Policy developments — including proposals to repurpose mid‑band spectrum and renewed spectrum auction authority — are increasing available mid‑band capacity for commercial wireless use. These changes create a practical imperative for mid‑band‑optimized antenna solutions.

Product innovation and integration: AI‑driven beamforming, multi‑element indoor arrays and modular external enclosures are reducing installation friction and improving in‑field performance, expanding addressable use cases (from dense urban FWA to long‑haul point‑to‑point bridging).

Resiliency and OEM consolidation: Buyers are gravitating toward suppliers that can demonstrate field‑proven IP, test capabilities and multi‑region production resilience — dynamics that will continue to shape market concentration.

The market exhibits a moderate level of concentration: the top three firms represent a meaningful, but not overwhelming, share of the market, while the top five further consolidate supplier influence. That structure creates room for both global platform leaders and specialised innovators to win.

Vantiva (France) — Strength: high‑performance indoor 5G arrays. Vantiva’s third‑generation Indoor5G™ 8Rx system (mid‑band boosters and patented techniques that improve gain and efficiency) exemplifies how differentiated antenna IP can translate into superior spectrum utilisation in dense FWA scenarios. Strategy implication: Network operators and home gateway manufacturers should prioritise design discussions where mid‑band performance is mission‑critical.

ZTE Corporation (China) — Strength: end‑to‑end platform integration. ZTE’s G6 family, including AI‑enabled Indoor solutions and outdoor Sub‑6/mmWave CPE, demonstrates the power of combining radio, firmware and antenna innovation. Strategy implication: OEMs seeking rapid product cycles will favour partners that can deliver vertically integrated CPE platforms.

Poynting (South Africa) — Strength: ruggedised outdoor CPE enclosures and wideband antennas. Poynting is a clear option where weather‑hardened performance and broad frequency coverage are priorities for rural and enterprise deployments.

TP‑Link, Huawei, and other high‑volume OEMs — Strength: scale and distribution. These manufacturers pair portfolio breadth with strong route‑to‑market capabilities for consumer and SOHO segments. Expect them to compete aggressively on integrated and detachable antenna options for mainstream deployments.

Specialists and ODMs (Kenbotong, Shenzhen Keesun, Ameison, VLG Tech, M.gear US, Antenna Products Corporation) — Strength: niche product engineering and manufacturing agility. These suppliers will remain critical for OEMs seeking rapid, low‑risk customisations and localised supply footprints.

Airgain (USA) — Strength: embedded antenna IP and design wins with gateway OEMs. Recent multi‑year design awards for Wi‑Fi 7 gateways underscore the strategic value of embedded antenna expertise in premium broadband equipment.

Vantiva’s March 2026 Hawk 5G FWA Gateway introduces a third‑generation Indoor5G™ 8Rx antenna system with patented mid‑band boosters that materially improve combined gain and efficiency — a clear signal that antenna IP will be a gating factor in dense FWA rollouts.

ZTE’s product debut at MWC Barcelona 2026 (G6 Ultra and G6 Max) underscores a push to couple AI‑enhanced antenna solutions with outdoor CPE for both Sub‑6 and mmWave FWA applications.

Airgain’s H2‑2026 design wins in Wi‑Fi 7 fiber gateway platforms validate the long tail of embedded antenna opportunity within fixed broadband gateways.

Market sizing and scenario modelling (conservative, base, upside) across 2026–2032 with sensitivity to spectrum policy and device price erosion.

Supplier benchmarking matrix covering IP depth, manufacturability, test capabilities, anechoic‑chamber validation and multi‑region production resilience.

Technology deep dives: antenna architectures (integrated arrays, external high‑gain, modular panel systems), performance trade‑offs, and field case studies illustrating real‑world coverage and throughput impacts.

TCO and procurement playbooks: lifecycle cost models, upgrade pathways and contract clauses to protect upgradeability and interoperability.

Regulatory scenario analysis: quantifying the coverage and capacity impact of mid‑band repurposing, alternative FCC outcomes and cross‑jurisdictional policy divergence.

M&A and partnership screening: ready‑to‑use scoring templates highlighting strategic fit, defensibility and integration risk.

Risk heatmap and mitigation actions covering supply shocks, component commoditisation and rapid obsolescence from network upgrades.

Network operators: Convert spectrum and policy shifts into concrete FWA pilots that prioritise mid‑band‑optimised CPE; require measurable antenna performance SLAs tied to coverage and throughput guarantees.

Gateway OEMs: Invest selectively in embedded antenna IP or secure multi‑year design partnerships with specialist vendors; favour modular designs that facilitate field upgrades as spectrum and use cases evolve.

Component and chipset vendors: Align RF front‑end roadmaps with antenna vendors to accelerate turnkey CPE designs that reduce BOM complexity and installation time.

Investors and M&A teams: Prioritise targets with proven design wins, defensible patents and multi‑region manufacturing footprints; treat embedded antenna IP as a material value driver, not a commoditised accessory.

Enterprise and public sector buyers: Demand full‑stack test results (radiated efficiency, gain across operational bands, real‑world throughput) as part of procurement, and require upgrade pathways for mid‑band re‑allocation scenarios.

Executives should use the report to underpin three critical board actions in 2026: (1) validate capital allocation to CPE and gateway roadmaps using scenario‑based NPV and TCO models; (2) define sourcing strategies that balance IP access with supply resilience; and (3) formalise regulatory contingency plans that preserve deployment pace if auction or classification outcomes shift. The report includes ready‑to‑run slides and executive briefs tailored for board presentations and investment committees.

In this preview we deliberately present the macro trajectory and strategic conclusions while withholding granular segment tables and discrete regional/application splits to preserve the full commercial utility of the dataset. The complete report contains the detailed breakdowns, vendor share matrices and downloadable models that enterprise teams use to execute procurement, integration and M&A decisions. Those core segmented datasets are available through PW Consulting’s report portal and include the empirical inputs and assumptions used for our modelling.

For procurement teams, product leaders and investment committees preparing for 2026, the full PW Consulting Cpe Antenna Market report is designed to be immediately operational — not merely descriptive. Contact PW Consulting to obtain the complete dataset, scenario models and vendor scorecards that will enable your team to convert the projected USD 1.58 billion-to‑USD 2.76 billion market trajectory into a concrete competitive playbook.

For detailed analysis of this topic, please visit the official page:Cpe Antenna Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com