Laser Hair Removal In Dubai Best Areas For Treatment

Other |

2026-05-11 11:07:14

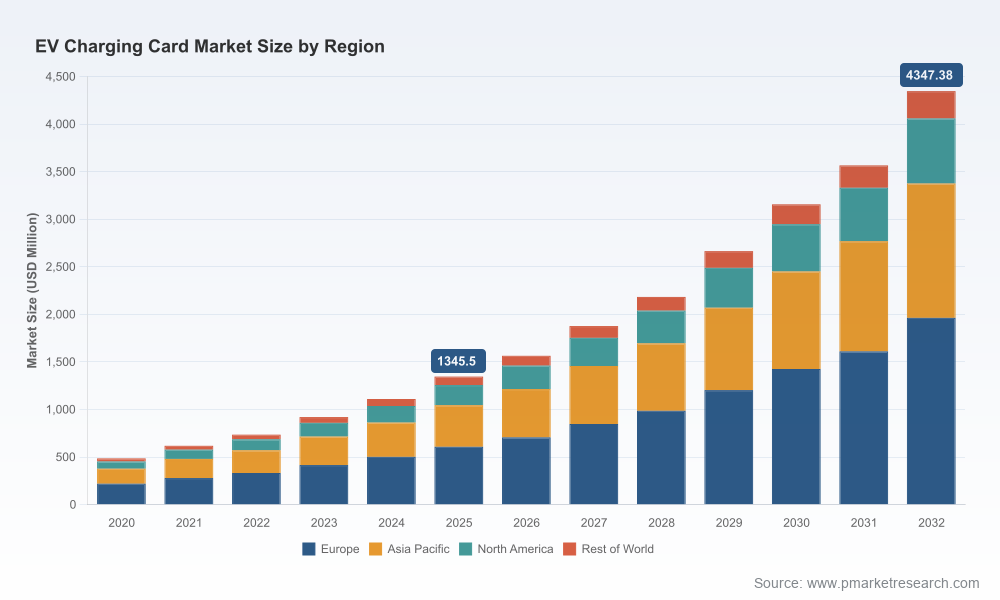

PW Consulting’s latest industry brief on the EV Charging Card market synthesizes five years of historical dynamics and a seven‑year forecast horizon to deliver a single strategic truth: access and payment credentials are no longer a commodity accessory to charging infrastructure—they are a strategic control point in the EV ecosystem. The market, which we estimate at USD 1,345.5 Million in 2025, is forecast to expand at a compound annual growth rate (CAGR) of 18.24% through 2032, reaching an estimated USD 4,347.38 Million. For executives making 2026 investment, partnership and product decisions, this report reframes charging cards as a multi‑dimensional lever that affects customer acquisition, roaming economics, data monetization and regulatory compliance.

Ev Charging Card Market

Acceleration window: 2026 is the inflection point where infrastructure rollouts (public and commercial) meet mass vehicle compatibility, creating a higher elasticity of demand for frictionless authentication and billing.

Ev Charging Card Market

Strategic leverage: credentials—whether RFID, NFC or cloud tokens—are increasingly used to lock in customer journeys across hardware, software and billing stacks. Early positioning yields disproportionately large downstream returns in customer lifetime value and network utilization.

Ev Charging Card Market

Regulatory convergence: regional rules on charger placement and interoperability are pushing common access frameworks; organizations that align with these constraints early avoid expensive retrofits and unlock roaming revenue sooner.

Market sizing & trajectory: rigorous top‑down and bottom‑up estimates covering 2020–2025 historical performance and 2026–2032 forecasts, plus sensitivity scenarios tied to vehicle penetration and public charging deployment rates.

Commercial playbooks: go‑to‑market blueprints for OEMs, charge point operators (CPOs), utilities and payment processors. These include partner archetypes, contract models (subscription vs. pay‑per‑use), pricing frameworks and margin breakpoints tailored to scale.

Technology decision framework: a vendor‑agnostic evaluation matrix comparing RFID, NFC, proprietary tokenization and app‑first approaches across cost-to-implement, security posture, user experience, and roaming compatibility.

Integration & operations toolkit: implementation checklists for credential issuance, provisioning, OTA updates, reconciliation workflows and fraud controls, plus sample API/settlement flows and test cases to accelerate pilot-to-scale transitions.

Commercial negotiation templates: term sheets and SLA clauses that reflect industry norms for roaming, invoicing cadence and liability—designed to protect cash flows during network scaling and to assign responsibility for charge session disputes.

Decision maps for onshoring and supply‑chain resilience: scenario analyses showing when to favor domestic card manufacturing or local chip provisioning to meet Buy America / local content rules without compromising unit economics.

Competitive and partner heatmaps: curated matrices identifying where incumbent CPOs, energy retailers and automotive OEMs are competing or cooperating across ownership, issuance and settlement roles.

The competitive field combines proprietary OEM initiatives, networked CPO platforms and energy retailers enabled by payments and roaming specialists. Key players profiled in our brief include Tesla, EVgo, Shell Recharge, ChargePoint, Blink Charging, Octopus Energy, ABB, Siemens, Fortum Charge & Drive, Radius, Tata Power and E‑Flux.

Tesla: continues to leverage a closed but high‑value credential proposition integrated with its Supercharger network—prioritizing a seamless customer experience for its installed base while selectively opening interfaces to non‑Tesla vehicles in targeted markets.

EVgo: is expanding protocol support and fast‑charging footprints in North America, coupling physical network growth with credential solutions that emphasize quick, predictable authentication for high‑turnover DC fast‑charging sites.

Shell Recharge & ChargePoint: these networked providers focus on scale, interoperability and broad roaming partnerships; their cards and account models are designed as neutral access layers that promote multi‑brand usage and consolidated billing.

Energy retailers (e.g., Octopus Energy) and utilities: are positioning charging cards as an extension of customer energy products—bundling access with tariffs and demand‑response signals, and using credentialing to smooth grid integration.

Hardware incumbents (ABB, Siemens): market charging hardware with integrated access options—targeting commercial and public buyers seeking turnkey solutions where card issuance and reader compatibility are packaged together.

Regional champions (Tata Power, Fortum, Radius, E‑Flux, Blink): their propositions emphasize market‑specific needs—local roaming agreements, consolidated invoicing and simple tap‑to‑charge options designed for quick consumer adoption.

Network protocol alignment: recent deployments of cross‑connector protocols and increased NACS compatibility in non‑Tesla networks accelerate the need for credentials that can operate across heterogeneous station fleets.

Product launches in emerging markets: new RFID card products tailored for tap‑to‑go behavior are lowering the adoption barrier in high‑growth geographies, creating first‑mover advantages for local CPOs.

Consolidation of access roles: leading CPOs and energy retailers are negotiating roaming and settlement layers that aim to control end‑user relationships while outsourcing hardware operations—forcing OEMs and software vendors to clarify where they capture value.

The market is still consolidating: the top three firms capture a meaningful share of industry revenue, with the top five representing a clear majority of market control. That concentration creates both threats and opportunities—incumbents can set de‑facto interface standards, while challengers can exploit niche verticals (fleet, workplace, multi‑network bundles) to scale rapidly. Our brief provides concentration metrics and strategic playbooks for both market leaders and emerging challengers.

Interoperability mandates: rules requiring standardized charging corridors and minimum charger densities are forcing interoperability considerations into procurement and product roadmaps; credentials that ease roaming will reduce stranded investment risk.

Infrastructure expansion: a rapid increase in fast‑charging ports and large‑scale public deployments means that authentication workflows must prioritize speed, reliability and minimal user friction to sustain throughput economics.

Onshoring and trade policy: supply‑chain incentives and local content requirements in key markets are reshaping procurement strategies for card manufacturing and chip sourcing—our brief quantifies break‑even points for local manufacturing vs. imported components.

Installation economics: with DCFC installations commanding large capex outlays, credentialing is a relatively low‑cost lever with outsized impact on utilization and revenue per site—making cards a high‑ROI area for marginal investment.

Define credential strategy as a product decision, not an IT project. Establish ownership—marketing, payments, or product—then align margins and KPIs (activation, session start latency, roaming success rate).

Adopt hybrid issuance: deploy durable physical cards for low‑complexity mass adoption alongside tokenized mobile credentials for premium or enterprise clients to balance cost and experience.

Negotiate roaming and settlement terms that protect cash flow during growth phases: prioritize predictable invoicing cycles, dispute resolution SLAs and clear liability for failed sessions.

Invest in telemetry and reconciliation tooling early: audit trails for credential use drive fraud controls, subscription enforcement and granular utilization analytics—these data streams become monetizable assets.

Plan for regulatory alignment: bake compliance checks and certification milestones into procurement and pilot timelines to avoid slowdowns when standards mature.

Pursue partnership experiments with OEMs and fleet operators: bundled credential offerings reduce churn and accelerate adoption in high‑value segments; pilot programs with clear exit criteria enable rapid scaling.

Our brief converts market movement into executable options. We combine quantitative forecasting (historical trajectories and an 18.24% CAGR through 2032) with granular commercial templates and technical integration guides so that leaders can reduce time to outcome. For product, commercial and M&A teams preparing budgets and pilots in 2026, the report shows where to prioritize capex, where to pursue partnerships and where to defer scale until protocol clarity emerges.

This release is designed as a strategic primer. It exposes the high‑level growth story, competitive dynamics and the operational levers that will decide winners in the next 18–36 months, while reserving the granular segment tables, region‑by‑region splits, and downloadable commercial templates for the full report. Companies that act on the insights outlined here—aligning credential strategy to commercial model, investing in reconciliation and negotiating smarter roaming terms—will convert the market’s projected expansion into defensible revenue growth.

For the full dataset, proprietary segment analysis and plug‑and‑play implementation tools, access our complete Ev Charging Card Market report on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Ev Charging Card Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com