PW Consulting Strategic Brief: Fuel & Aircraft Fuel Oil Filters Market — 2026 Decision Playbook

Executive snapshot

PW Consulting today publishes a strategic briefing derived from our forthcoming market research on the Fuel & Aircraft Fuel Oil Filters market, providing a focused lens for executive decision-making in 2026. The market has expanded steadily over the past half-decade — from an estimated USD 142.35 Million in 2020 to USD 179.65 Million in 2025 (base year) — and our model projects growth to about USD 191.55 Million in 2026, extending to roughly USD 257.51 Million by 2032. That trajectory reflects a compound annual growth rate of approximately 5.25% over the forecast window (2026–2032). These aggregates underline both a durable aftermarket and recurring demand drivers across commercial, military and general aviation ecosystems.

Fuel Fuel Oil Aircraft Aerospace Filters Market

Why this briefing matters for 2026 corporate strategy

- Regulatory pressure and fuel composition shifts are accelerating product obsolescence cycles. The onset and ramp of SAF blending mandates — for example, the ReFuelEU Aviation initiative — materially change contamination profiles and filtration performance requirements. Buyers and suppliers must reconcile certification timelines with near-term fleet needs.

- Technological substitution is underway. Two-stage filtration expectations (as defined in industry standards such as EI 1581) and newer water-barrier and coalescer technologies require targeted R&D and qualification investments to avoid aftermarket share losses.

- Supply-side economics are tightening. Sustainable aviation fuel remains significantly more expensive than conventional jet fuel (sector studies indicate multiples often ranging from 2x to 5x), creating incentives for airlines and MROs to optimize lifecycle costs through filtration longevity, service contracts and parts standardization.

- Market concentration is meaningful. Our competitive concentration analysis shows the top three firms account for roughly 48.5% of market revenue, while the top five account for about 62.8%, signaling an industry where tier-1 suppliers influence OEM OEM qualification, standards alignment and aftermarket pricing.

- Operational risk is non-trivial. Contaminants such as Diesel Exhaust Fluid (DEF) have been flagged in safety alerts for causing crystallization and filter blockages; operators must prioritize contamination detection, supply-chain traceability and filter maintenance protocols.

What’s inside the full PW Consulting report (practical, operational content)

- Clear market sizing and trend analytics: historical reconciliations (2020–2025) and detailed forecasting (2026–2032) with scenario toggles for SAF adoption rates, fuel price shocks and regulatory acceleration.

- Actionable supplier diagnostics: scorecards that assess technology readiness, qualification timelines, capacity constraints and aftermarket service footprints for leading and niche players.

- Regulatory and standards playbook: a practical mapping of ReFuelEU implications, EI 1581 compliance checkpoints, qualification routes for SAF-compatible filters, and a timeline of certification risk exposures.

- Commercial playbooks for OEMs and suppliers: negotiation levers, bundling strategies (filters + services), PMA route-to-market considerations and sample commercial term language to protect margin during SAF transition periods.

- M&A and partnership roadmap: target archetypes, valuation drivers, integration checklists and a prioritized shortlist methodology for bolt-on acquisitions or strategic partnerships.

- Operational toolkits: Test matrices, contamination forensics protocols, inventory optimization templates, and supplier audit frameworks that translate findings into 90-day action items.

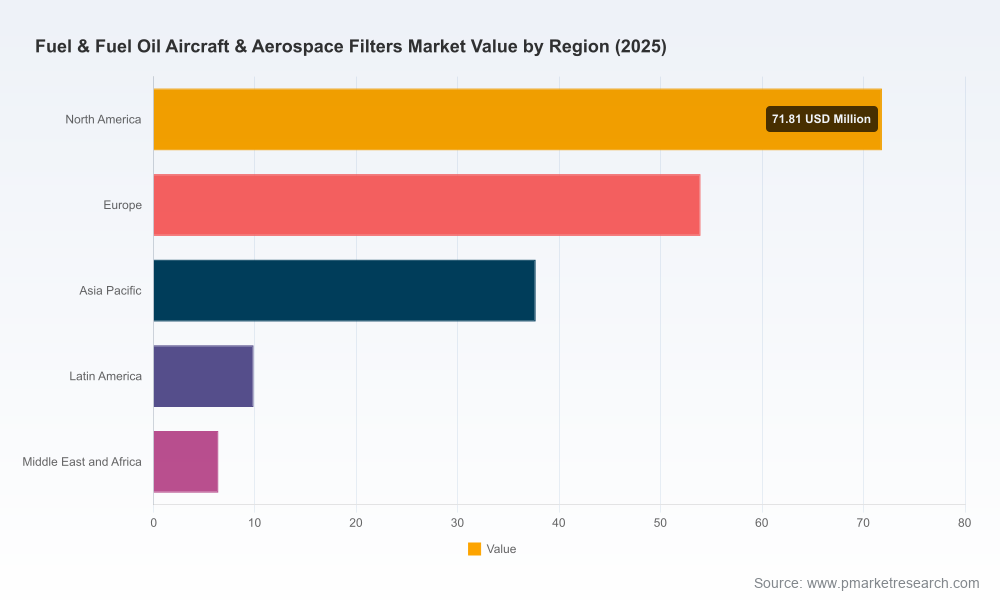

- Data annex and models: granular time-series datasets and editable financial models that allow clients to run customized forecasts and sensitivity analyses. (Note: the public brief omits detailed regional and application splits — those are included in the subscriber dataset.)

Competitive landscape — what incumbents and challengers reveal about strategy

The market displays a classic supplier-led evolution: established filtration specialists and aerospace conglomerates hold technical advantage and OEM relationships, while smaller niche vendors exploit PMA channels, aftermarket agility and cost plays. Noteworthy positions and recent moves provide strategic cues for 2026:

Fuel Fuel Oil Aircraft Aerospace Filters Market

- Parker Hannifin (Cleveland, Ohio) continues to be a technology leader in micron filtration and coalescer separations for aviation fuel handling. A recent product lifecycle decision — formal phase-out notices for legacy EI-qualified SAP monitors at the end of 2025 — signals an industry-wide migration to newer water barrier technologies and forces customers to accelerate migration plans.

- Donaldson Company (Minneapolis, Minnesota) has stepped up through inorganic expansion: completing the acquisition of Facet Filtration in May 2026 to broaden its mission-critical fuel and fluid filtration portfolio. This move highlights consolidation opportunities for players seeking scale in aviation-specific filtration and cartridge technologies.

- Pall Corporation (Port Washington, New York) remains embedded in OEM supply chains and fleet support programs; continued fleet-level contracts (e.g., recent supply continuity for large airlines) indicate that OEM endorsements and legacy relationships still drive a significant portion of demand.

- European OEMs and system integrators such as Safran and Eaton are leveraging integrated systems approaches, linking filtration with fuel management subsystems — a trend that favors suppliers capable of cross-domain integration and full-system warranties.

- Specialist suppliers (Porvair Filtration Group, Tempest Aero Group, Chase Filters & Components, Global Filtration, Norman Filter Company) are competing on customization, PMA credentials and aftermarket responsiveness — niches that become attractive acquisition targets or strategic partners for tier-1s seeking closer ties to MRO networks.

Immediate actions for executives — a 90-day operational playbook

- Conduct a SAF-readiness gap analysis across product lines: identify which filter families and coalescer designs require requalification for anticipated fuel blends; prioritize by fleet exposure and aftermarket revenue risk.

- Map certification timelines against fleet refurbishment schedules: build an adoption calendar that aligns filter qualification milestones with major MRO windows to avoid retrofit bottlenecks.

- Mitigate contamination risks now: deploy contamination forensics protocols at key supply nodes (tank farms, fuel trucks, refueling points) and institute rapid-response filter-change and inspection thresholds.

- Engage with strategic suppliers and OEMs: secure multi-year service contracts or co-development agreements to lock in supply and co-fund qualification testing for SAF compatibility.

- Reassess inventory and pricing models: account for extended SAF-related testing lead times and potential premium for certified SAF-compatible parts; revise service-level agreements and spares provisioning accordingly.

- Scan the M&A landscape: prioritize PMA-certified filter makers and coalescer specialists for potential acquisition to accelerate capability ownership and aftermarket capture.

Scenarios boards should model in 2026

- Baseline continuity: moderation in SAF adoption and steady 5.25% CAGR — plan for incremental R&D and targeted qualification spend to defend existing shares.

- Accelerated SAF adoption: if SAF uptake compresses certification timelines (driven by tougher regulation or airline procurement mandates), prepare for accelerated retrofit waves, creating opportunities for suppliers with validated SAF-compatible lines and for aftermarket service upsell.

- Supply-cost shock: a sustained widening of SAF-to-jet price differentials or disruption in filter media supply increases total cost of ownership pressure on airlines; value propositions tied to filter longevity, diagnostics and service become decisive.

How PW Consulting’s research adds value in executive decision cycles

Our work distills market dynamics into transaction-ready intelligence. Rather than abstract forecasts, the report couples financial modeling with operational roadmaps: prioritized investment themes, supplier scorecards, and contract language templates that pragmatically shorten the path from board approval to field execution. For C-suite and business-unit leaders, the brief provides the confidence to set budgets for 2026 while preserving optionality across SAF adoption trajectories and regulatory scenarios.

Fuel Fuel Oil Aircraft Aerospace Filters Market

Next steps & how to access the full dataset

The public briefing is designed to orient strategy and flag near-term tactical imperatives. For teams that require the full breakdown — including region-by-region and application-level revenue splits, detailed company market shares, downloadable time-series files and scenario-ready financial models — PW Consulting provides the complete report and client workshops. The full package includes editable scenario models, supplier diligence templates and a facilitated 90-day implementation roadmap tailored to your organization.

To arrange a briefing or secure access to the full report and accompanying datasets, contact PW Consulting’s Aerospace & Filters practice. Our advisory teams are prepared to run a confidential workshop that converts findings into prioritized initiatives you can operationalize within the next quarter.

For detailed analysis of this topic, please visit the official page:Fuel Fuel Oil Aircraft Aerospace Filters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com