Fused Silica Tubing Market: Strategic Imperatives for 2026 — PW Consulting Announces New Industry Intelligence

PW Consulting’s latest market study on Fused Silica Tubing provides a focused playbook for executives who must make capital, sourcing, and product-strategy decisions in 2026. The report synthesizes historical performance, forward-looking forecasts, supplier risk profiles, and actionable scenario tools to translate material science nuances into boardroom-ready choices. This press release outlines the report’s strategic value—demonstrating depth while preserving full segment-level detail for subscribers who access the complete report.

Fused Silica Tubing Market

Market trajectory at a glance

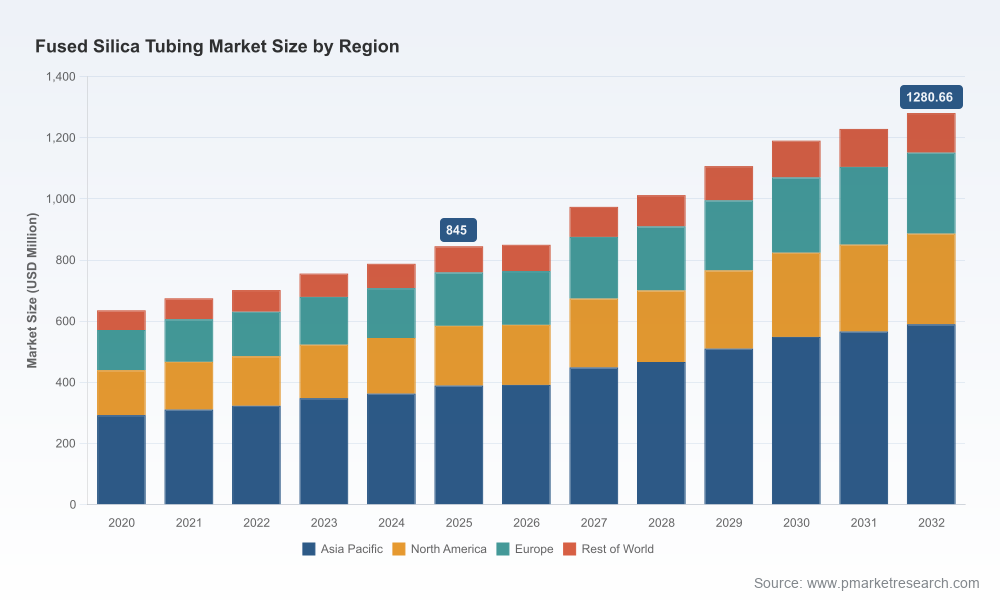

Using 2025 as the base year (revenue unit: USD Million), PW Consulting’s topline model traces a steady recovery and expansion of the fused silica tubing market since 2020. Our historical series shows the market moving from approximately USD 635 million in 2020 to USD 845 million in 2025. Under the base-case assumptions embedded in the report, the market is forecast to grow at a compound annual growth rate (CAGR) of 6.12% over the 2026–2032 forecast horizon, reaching roughly USD 1,281 million by 2032.

Fused Silica Tubing Market

These macro dynamics reflect a confluence of demand drivers—continued semiconductor process tightening, specialty fiber and optics requirements, and targeted industrial and laboratory applications—tempered by raw-material and regulatory constraints that can amplify pricing and supply volatility.

Fused Silica Tubing Market

What the report delivers — practical, transaction-ready intelligence

- Concise market sizing and growth pathways that reconcile historical shipments, capacity utilization, and demand-side signals into an investable forecast.

- Supply-chain risk maps that identify feedstock concentration points, single-source exposures, and logistics choke points, paired with mitigation playbooks.

- Supplier scorecards and benchmarking across manufacturing footprint, technology differentiation, quality (e.g., purity, fluorescence, UV stability), and aftermarket service levels.

- CapEx and capacity planning tools, including a prioritized list of facility investments and an IRR sensitivity model calibrated to HPQ availability and pricing scenarios.

- Commercial frameworks—TCO and pricing playbooks for OEMs and contract manufacturers that align product segmentation, coating options, and service SLAs to margin targets.

- M&A and partnership heatmaps highlighting target attributes (technology, geography, customer access) and deal-structuring considerations under different regulatory scenarios.

- Scenario analyses that stress-test revenue and margin outcomes against raw-material shocks, trade-policy shifts, and demand bifurcation between semiconductor and non-semiconductor end markets.

Key dynamics shaping 2026 decisions

- Feedstock scarcity and purity premium: High-purity quartz (HPQ) remains the strategic raw material differentiator. Supply is geographically concentrated and subject to environmental and mining constraints, which elevates supplier power and creates acute procurement risk for manufacturers and downstream buyers.

- Regulatory and trade complexity: Environmental controls in mining regions and episodic tariff negotiations have already influenced landed costs and supplier sourcing strategies. Firms must now embed trade-policy scenarios into multi-year sourcing contracts.

- Manufacturing specialization and scale economics: Technology choices—ranging from plasma fusion to traditional fusion methods, large-diameter capabilities, and precision coating processes—drive margin dispersion. Capacity expansions in targeted niches can produce outsized returns where demand is structurally durable.

- Concentration of supply: The market exhibits a moderate-to-high degree of supplier concentration, which affects competitive dynamics and creates both risk and opportunity for consolidation-minded players.

Competitive landscape — how major players are positioning

PW Consulting’s competitive assessment synthesizes public disclosures, proprietary interviews, and site-level analysis to characterize strategic postures across the vendor ecosystem. The market features a mix of global incumbents with vertically integrated feedstock-to-product capabilities, specialized technology houses that create differentiated large-diameter or low-fluorescence products, and regional manufacturers that compete on cost and responsiveness.

- Heraeus Quarzglas (Heraeus Covantics) — A leading global producer with a broad product portfolio tailored to semiconductor, specialty fiber, optics, and UV applications. Strengths include high-purity product lines and deep channel relationships; strategic focus is on premiumization and advanced process tubes.

- Momentive Technologies — Notable for its center of excellence in quartz fusion and execution of targeted capacity expansions focused on large-diameter tubing for wafer processing. The company’s recent plant investment underscores a play for higher-margin, capital-intensive segments.

- QSIL GmbH — A specialist using plasma fusion to produce very large hollow cylinders and custom OD tubing. QSIL’s technology is a competitive differentiator for applications requiring non-standard sizes and certain optical properties.

- Tosoh Quartz & Shin-Etsu — Japanese incumbents with strong positions in semiconductor-grade quartzware and integrated supply chains that emphasize consistency and cleanroom-compatible products.

- Saint-Gobain Quartz — Offers a diversified industrial portfolio with capabilities in high-temperature and specialty tubular products, leveraging its broader materials footprint for industrial cross-sell.

- Polymicro Technologies (Molex) — Focused on precision polyimide-coated fused silica capillaries for analytical and microfluidic segments. Polymicro’s strength is in precision and coating integration rather than large-diameter supply.

- Technical Glass Products (TGP) & WEINERT Industries — Providers that compete on customization, specialty optical properties (e.g., low fluorescence), and rapid-order responsiveness for laboratory and niche industrial applications.

- Chinese integrated producers — Regional players have scaled capacity to serve local semiconductor and solar markets; their strategic role continues to evolve under shifting trade and raw-material dynamics.

PW Consulting’s concentration metrics quantify this structure and point to a market where the top three and top five suppliers together control a meaningful share of global revenue—creating a landscape with both competitive intensity at the top and opportunity for smaller players to differentiate by specialization and service.

Strategic implications for 2026 — five priority moves

- Secure feedstock optionality: Negotiate multi-year HPQ arrangements with embedded quality tiers and force-majeure provisions; consider direct investments or offtake agreements with miners in strategically diversified geographies.

- Match technology to margin pools: Prioritize investments in large-diameter fusion, low-fluorescence materials, or specialty coatings where technical barriers sustain pricing power.

- Embed regulatory stress-testing into capital plans: Model project returns under tightened environmental constraints and tariff permutations to avoid stranded capacity.

- Pursue targeted M&A and JV plays: Look for tuck-ins that supply complementary process know-how, regional market access, or proprietary manufacturing methods to accelerate time-to-market.

- Operationalize supply-chain resilience: Deploy inventory hedging, dual-sourcing strategies, and local buffer capacity for critical customers in semiconductor fabs where supply disruption has high economic cost.

How PW Consulting’s tools accelerate execution

The report is designed as an execution toolset, not just a narrative. Subscribers receive dynamic models (editable spreadsheets and scenario dashboards), supplier scorecards that are exportable for procurement RFIs, and a prioritized investment rubric that ranks capex by risk-adjusted return. We also include negotiation playbooks for raw-material procurement and an M&A checklist calibrated to regulatory and technical due diligence needs unique to fused silica products.

Next steps — where to find the full intelligence

This release highlights the strategic threads senior leaders need to consider in 2026, while intentionally withholding the granular segment and regional splits that are part of the full PW Consulting dataset. Executives, investors, and procurement leaders who require the detailed breakout—regional demand trajectories, application-level volume and price sensitivity matrices, supplier-level capacity maps, and the editable scenario models—can access the complete report and supporting databases through PW Consulting’s subscription portal.

For immediate guidance and to request a briefing with our fused silica tubing practice leads, contact PW Consulting. The full report provides the actionable granularity that converts market insight into investment, sourcing, and M&A decisions for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Fused Silica Tubing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com