Digital Biomarkers Market Report: Trends, Drivers, and Strategic Analysis

Art |

2026-06-05 09:37:01

PW Consulting’s latest market study on elastic sealing (resilient seated) gate valves delivers a focused strategic toolkit for executives making capex, sourcing, product and M&A decisions in 2026. Anchored on a 2025 base year and a seven‑year forecast horizon (2026–2032), the market is forecast to grow at a compounded annual growth rate (CAGR) of 7.3% — expanding from a reported USD 1.45 billion in 2025 to an estimated USD 2.37 billion by 2032. The historical trajectory (2020–2025) shows material acceleration in procurement and replacement cycles that materially changes competitive dynamics heading into the mid‑2020s.

Elastic Sealing Gate Valve Market

Decisions made in 2026 will determine market positioning throughout the forecast period. With near‑term market value expanding meaningfully year‑on‑year into 2026, procurement windows and product roadmaps must be aligned now to capture growth while managing longer manufacturing lead times and certification cycles.

Elastic Sealing Gate Valve Market

Market structure is neither fully fragmented nor tightly consolidated: the top three players account for a material but non‑dominant share of industry revenue, and the top five widen that concentration moderately. This creates both defensive pressures for incumbents and attractive entry corridors for focused challengers with differentiated technology, cost or channel strategies.

Elastic Sealing Gate Valve Market

Regulation, materials and standards are active drivers. Compliance with AWWA and European potable water standards and the cost of elastomers such as EPDM are already reshaping supplier choice, warranty structures and total cost of ownership conversations with infrastructure owners.

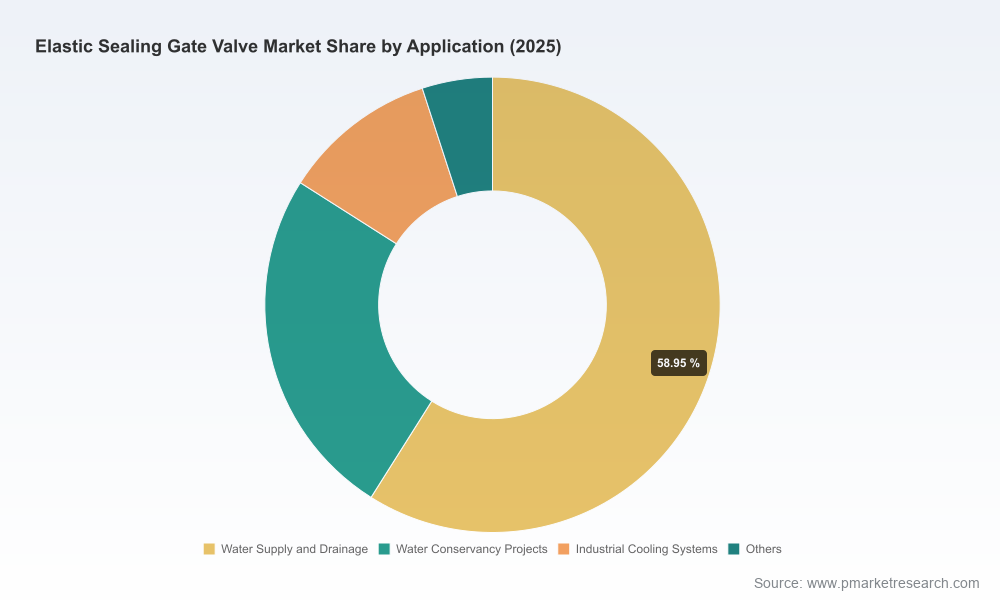

Strategic synthesis: an evidence‑based narrative linking macro demand drivers (urban water infrastructure upgrades, water conservation projects and industrial cooling needs) to procurement cycles, pricing pressure and product innovation imperatives.

Commercial playbooks: tender structuring templates, unit price sensitivity models, and a procurement scorecard that buyers and OEMs can adapt to make first‑order tradeoffs (price vs. warranty vs. lead time vs. certification cost).

Supplier and channel diagnostics: supply‑chain maps, raw‑material exposure heatmaps, and a shortlist methodology for strategic supplier partnerships and dual‑sourcing where appropriate.

Product and R&D briefs: a technology readiness assessment for elastomers and sealing configurations, suggested test plans for zero‑leakage claims and a prioritised R&D agenda for mid‑market and premium product lines.

M&A and investment toolkit: valuation sensitivity templates, an acquisition target scorecard and three scenario templates (baseline growth, accelerated adoption, and disruption) for board‑level debates and investment committees.

Regulatory and compliance matrix: mapped certification pathways (AWWA, EN, BS) with timing and cost implications for product launch in major markets.

The market features a mix of longstanding European specialists and highly competitive Chinese manufacturers. Established European firms bring certification pedigree and deep municipal channel relationships, while several China‑headquartered suppliers are scaling manufacturing, broadening elastomer options and aggressively competing on price and lead time.

AVK Valves (Denmark) — Known for resilient seated gate models engineered to meet BS and EN standards, AVK’s emphasis on certified product families and DN‑range coverage keeps the company well‑positioned for municipal procurements that prioritise standards compliance and long‑term warranties.

VAG GmbH (Germany) — Specialist in advanced sealing technology, VAG’s technical foothold in municipal and industrial water projects makes it a logical partner for infrastructure owners seeking lifecycle performance assurances rather than lowest‑cost hardware.

China‑based manufacturers (EJ Industrial, Union Valve, Dervos, Weidouli, BELGICAST) — These suppliers have expanded product portfolios to include EPDM/PTFE options, non‑rising and rising stem designs, and export programmes targeting large water projects. Their scale and supply agility introduce pricing pressure and faster time‑to‑ship options for large projects, but purchasers must weigh certification timelines and counterparty risk.

For strategic planners: incumbents should double down on certifiable product differentials, predictable warranty economics and bundled service offers (testing, installation oversight, remote diagnostics). New entrants with manufacturing scale should invest selectively in internationally recognised certifications and a small number of reference projects to reduce perceived buyer risk.

Two operational facts deserve immediate attention:

Elastomer exposure — EPDM, a key resilient seating material, is subject to cyclical feedstock pricing and regional availability. Recent market checks indicate typical pricing around USD 3.08/kg in Northeast Asia (April 2026), which feed through to margin sensitivity on soft‑seal designs and to lifecycle cost assessments for buyers.

Certification burden — Water service standards (AWWA C509/C515 in the US; EN 1074‑2 and BS 5163 in Europe) impose material, testing and documentation requirements that affect time to market and unit economics. For any supplier seeking to scale in municipal channels, a clear path to certification must be part of the go‑to‑market plan.

Practical implication: procurement teams should incorporate elastomer price indices and certification lead‑time assumptions into three‑year purchase forecasts and vendor scorecards. Suppliers should model contract pricing with raw material pass‑through clauses or hedging strategies where appropriate.

Baseline (Most likely): Market grows in line with the forecast CAGR of 7.3%. Tactical focus: protect margins through productivity gains, secure dual suppliers for EPDM, expedite certifications for top‑selling SKUs, and lock multi‑year supply agreements with indexed pricing clauses.

Accelerated adoption: Upgrades and new water projects accelerate faster than expected driven by climate resilience funding and capex stimulus. Tactical focus: prioritise capacity expansion, pre‑qualify subcontractors for field services, and accelerate premium product launches with demonstrable TCO benefits.

Disruption scenario: Raw material shocks, trade restrictions, or sudden standard changes increase certification costs and delivery uncertainty. Tactical focus: pivot to alternative elastomers where validated, increase inventory coverage for critical SKUs, and implement contingency logistics routes to maintain project delivery dates.

Execute a 30‑day procurement quick‑scan: identify top five SKUs for re‑negotiation, quantify raw material exposure and implement immediate pass‑through or fixed‑price clauses where feasible.

Run a 60‑day product certification sprint: map required tests, assign technical owners, and budget for accelerated third‑party testing to shorten market entry for priority regions.

Deliver a 90‑day commercial action plan: segment customers by risk appetite, craft tailored value propositions (lowest TCO vs. fastest delivery vs. certified compliance), and launch pilot bids with a selected set of distributors or integrators.

The elastic sealing gate valve market is at an inflection point: clear growth, persistent certification requirements and supply‑side shifts create an environment where disciplined strategic moves in 2026 will yield multi‑year advantage. Whether the objective is protecting margin, scaling fast or acquiring niche capabilities, companies that align procurement, certification and product development to the market’s trajectory — and that use scenario planning to mitigate elastomer and regulatory risk — will be best placed to convert market growth into sustained value.

PW Consulting’s full Elastic Sealing Gate Valve Market report contains the granular datasets, regional and application models, supplier due‑diligence templates and financial sensitivity models needed to operationalise these insights. For the complete dataset, proprietary segmentation analysis and the investor‑grade annexes, visit the PW Consulting report page to request access to the full study.

For detailed analysis of this topic, please visit the official page:Elastic Sealing Gate Valve Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com