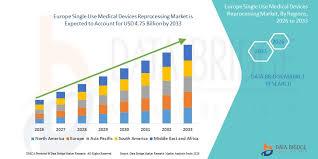

Europe Single Use Medical Devices Reprocessing Market Size, Share, Trends, and Forecast by 2033

Other |

2026-06-25 12:47:35

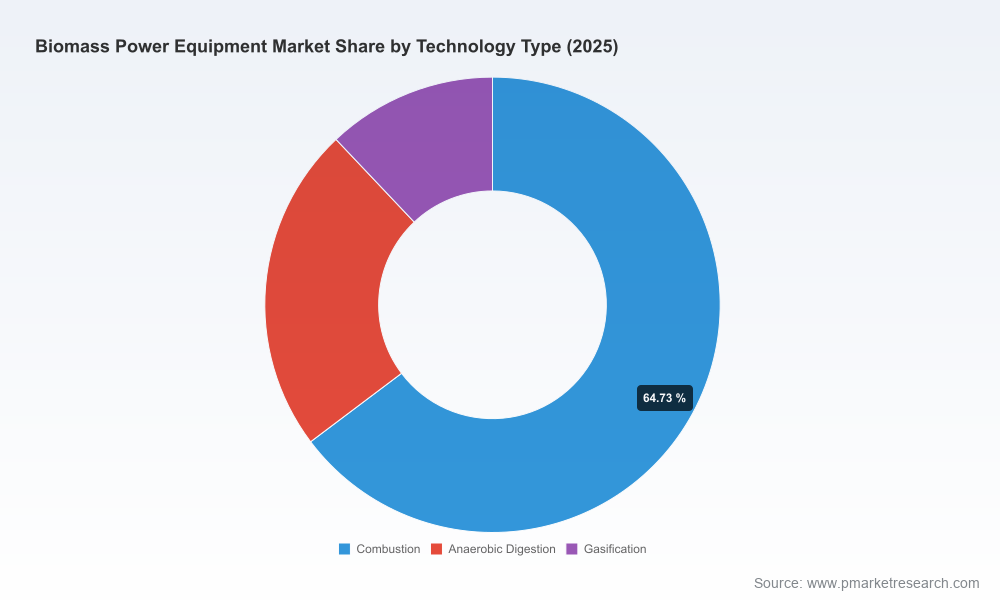

PW Consulting today publishes a strategic briefing drawn from our full Biomass Power Equipment Market report (base year 2025). The global market for biomass power equipment reached USD 125,458.26 Million in 2025 and, under the scenarios modeled in our forecast window (2026–2032), is expected to expand at a compound annual growth rate (CAGR) of 6.99%, reaching roughly USD 201,458.54 Million by 2032. This briefing distills the practical, decision-ready insights that corporate leaders, project developers, investors and OEMs need to shape 2026 strategies — while reserving the granular segment tables and model outputs for the full report.

Biomass Power Equipment Market

Policy and finance alignments are maturing. Regulatory drivers and fiscal incentives implemented through the mid‑2020s are moving from design to deployment; 2026 will be the first full operational year where many incentive frameworks (and their compliance and subsidy mechanics) materially affect project-level returns.

Biomass Power Equipment Market

Technology inflection points are converging with supply-chain normalization. Advancements in boiler and turbine integration, alongside modular gasification and anaerobic digestion systems, are lowering threshold project sizes and shortening lead times, shifting where and how capital should be deployed.

Biomass Power Equipment Market

Feedstock markets and carbon pricing dynamics are crystallizing project economics. Commodity and emissions-cost trajectories that were speculative in earlier years are now exerting measurable influence on long‑term LCOE and bankability.

The market’s projected 6.99% CAGR to 2032 translates to meaningful expansion in equipment demand, spare-parts markets and long‑term service revenues. For 2026 planning, companies must treat the near-term window as an “early-adopter lifecycle” phase: opportunities to secure preferred engineering, procurement and construction (EPC) slots, long-lead components and strategic feedstock contracts will provide outsized advantage to projects that can close financing within the next 12–18 months.

For private equity and infrastructure investors, the growth profile suggests a dual strategy: selectively accelerate late-stage, shovel‑ready deployments to capture near-term contracted cashflows and concurrently seed technology‑led pilots (e.g., advanced gasification hybrids, modular anaerobic digestion) to capture higher-margin equipment and aftermarket services later in the decade.

Regulatory drivers: Renewables targets and clean‑energy directives are reshaping subsidy availability and market access. Regulatory frameworks enacted through 2024–25 materially improve revenue certainty for qualified biomass projects, but the degree of support and compliance complexity varies by jurisdiction — a primary sensitivity in our base and upside cases.

Carbon pricing: Elevated carbon allowance levels have made biomass an increasingly attractive alternative to fossil fuels from an operational cost perspective. Carbon-cost trajectories are among the top three variables that swing internal rate of return (IRR) modeling across our scenario set.

Feedstock economics: Commodity pricing volatility for pelletized wood and agricultural residues directly affects operating margins. Recent market signals and Q4 2024 price references point to higher baseline feedstock costs relative to the early 2020s, requiring more conservative fuel-price assumptions in underwriting.

Capex composition: Equipment-class capital intensity — particularly for grate stoker systems and fluidized bed configurations — remains a dominant driver of early project cash burn. Component-level cost benchmarks are included in the full report to enable bottom-up capex build-ups for deal diligence.

Across combustion, fluidized bed and gasification architectures, our analysis highlights three operational priorities for 2026 deployments:

Fuel flexibility and pre-treatment integration — enabling co-firing and variable-sourcing strategies to manage feedstock price and availability risk;

Modularization and standardization — reducing EPC cycle times and capital intensity for small-to-medium scale projects;

Digital operations and predictive maintenance — driving aftermarket service revenue and availability improvements that materially affect levelized costs.

Project-level efficiency gains reported by industry leaders in 2023–2024 demonstrate that incremental efficiency and integration improvements can move project returns meaningfully. Incorporating such improvements into 2026 bidding and plant design is a practical lever for competitiveness.

The market remains moderately fragmented, with leading equipment suppliers, turbine manufacturers and EPC integrators capturing a meaningful but not dominant share of global demand. Market concentration metrics show that the top three and top five players command a minority portion of global revenue, leaving room for regional specialists and innovative technology vendors to grow through targeted propositions.

Key companies in our coverage bring complementary strengths:

Valmet (Espoo, Finland) — strengths in turnkey biomass CHP plants, flue-gas treatment and integration across grate and fluidized-bed platforms; recent 2024 commissioning activity highlights continued delivery capability on mid‑to‑large projects.

ANDRITZ (Graz, Austria) — deep expertise in fluidized bed combustion and boiler systems; continued order activity in 2024 evidences strong project pipeline in industrialized markets.

Babcock & Wilcox (Akron, USA) — established technology for grate and stoker systems, with recent grid-connection milestones demonstrating operational readiness in major markets.

Mitsubishi Power (Yokohama, Japan) and Siemens Energy (Munich, Germany) — turbine and plant integration leaders, pushing efficiency and controls; notable efficiency advancements and plant deployments in 2023–24.

GE Vernova (Cambridge, USA) — adaptable gas and steam turbine offerings with integrated control systems attractive to large-scale and flexible applications.

Regional specialists (e.g., Zibo Zichai New Energy) — cost‑competitive gasifier and equipment suppliers for small‑to‑medium scale projects, particularly where modularity and local manufacturing matter.

Recent corporate milestones — including commissioning and order wins in 2024 — confirm that established players remain active in both technology development and project delivery. For acquirers and suppliers, the implication is clear: strategic partnerships, joint ventures and selective M&A will be the accelerants to capture growing equipment demand, but targets and synergies must be evaluated with candid engineering and feedstock stress‑tests.

Our full report is designed as an operational toolkit, not an academic treatise. Deliverables include:

Market sizing and validated revenue forecast models (interactive spreadsheets for scenario simulation);

Capex and opex benchmarking by technology class and plant scale;

Supplier scorecards and procurement playbooks to inform RFPs and contract structuring;

Feedstock risk maps, price-sensitivity dashboards and sourcing optimization templates;

Regulatory and subsidy impact matrices aligned to key policy regimes, and a calibrated carbon-pricing sensitivity module;

M&A target shortlist methodology and a bankability checklist for project finance diligence;

Executive playbooks for developers, OEMs, utilities and institutional investors, with 12–36 month action plans for 2026 execution.

We recommend a three-horizon decision framework for teams preparing budgets and capital allocation in 2026:

Horizon 1 (0–12 months): Lock preferred EPC and long‑lead equipment procurement; secure feedstock offtake or options; stress-test project economics against conservative carbon and fuel-price cases.

Horizon 2 (12–36 months): Deploy modular pilots and digitize operations for O&M scale-up; pursue strategic partnerships with turbine and controls suppliers to de‑risk performance guarantees.

Horizon 3 (36+ months): Consolidate aftermarket services and develop regional service hubs; evaluate M&A to acquire technologies or footprint in priority markets once early projects validate returns.

Key risks identified in our scenario work are: feedstock availability and price shocks, regulatory policy reversals or tightening of sustainability standards, and supply‑chain bottlenecks for critical components. Mitigation levers that materially improve bankability include multi-sourced fuel contracts, indexed tariff structures, stepped-in warranties from OEM partners, and community engagement programs that secure social license to operate.

This briefing is a strategic preview. The full PW Consulting Biomass Power Equipment Market report contains the granular segmentation, underlying datasets, model files and supplier benchmarking that corporate teams require to act in 2026. Access to the full intelligence package will equip you to underwrite projects, structure commercial terms, and pursue growth with quantified downside protections and upside scenarios. Visit our report page to download the executive dashboard, sample chapters and to arrange a bespoke briefing with our industry advisory team.

For detailed analysis of this topic, please visit the official page:Biomass Power Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com