Industrial-Grade Trichlorosilane Market: Strategic Outlook for 2026 Decision-Makers

As capital planners, procurement chiefs and corporate strategists prepare budgets and moves for 2026, trichlorosilane (TCS) sits at the intersection of two high-stakes agendas: energy- and cost-efficient polysilicon supply for solar and semiconductor onshoring. PW Consulting’s latest Industrial-Grade Trichlorosilane Market study delivers the focused intelligence executives need to translate macro momentum into defensible, time-sensitive decisions—without exposing the proprietary segmentation that makes the underlying opportunity unique. This release outlines the study’s strategic value and highlights the directional insights that should shape 2026 actions.

Industrial Grade Trichlorosilane Market

Executive summary: market trajectory and concentration

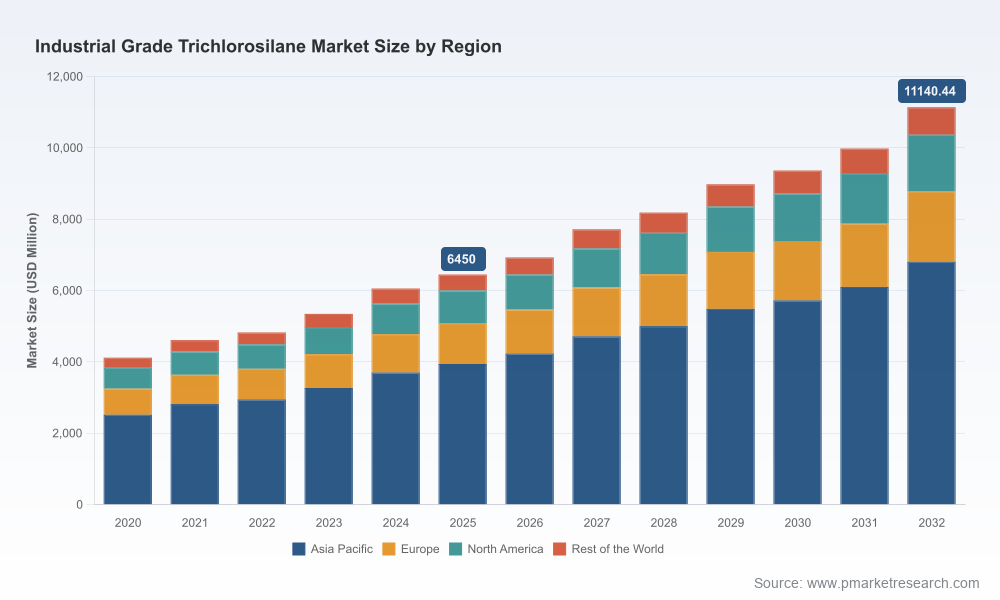

Our market model shows that the industrial-grade TCS market expanded materially during 2020–2025, nearly doubling in scale over that five‑year span. The market reached an estimated USD 6.45 billion in the 2025 base year and, under our central-case assumptions, grows at a compound annual growth rate (CAGR) of approximately 8.12% through the forecast window to 2032—reaching roughly USD 11.1 billion by the end of the period. These dynamics are powered by concurrent secular drivers in polysilicon for solar and by differentiated demand from semiconductor-grade supply chains feeding localized fabs and specialty chemical markets.

Industrial Grade Trichlorosilane Market

Market structure matters: the sector exhibits moderate-to-high concentration, with the top three players controlling nearly half of total market value and the top five exceeding 60%. For strategists, that means an environment with significant scale advantages, but also room for agile entrants to win share around technology, feedstock security and downstream partnerships.

Industrial Grade Trichlorosilane Market

Why 2026 is an inflection year

- Policy-induced demand realignment: Onshoring of semiconductor capacity and government incentives for domestic polysilicon mean larger and timelier offtake commitments for nearby TCS suppliers. Funding windows and rulemaking in 2026 will determine who qualifies for long-term partnership premiums.

- Feedstock and input variability: Silicon metal and other feedstock markets showed renewed instability in late‑cycle price trajectories and regional trade policy actions that directly influence unit economics for TCS producers. Procurement strategies formed in 2026 will determine margin resilience through 2027–2029.

- Technology and emissions constraints: Adoption of lower‑energy production technologies (e.g., advanced fluidized-bed reactor approaches and improved purification trains) and tightening environmental compliance require near-term capex decisions that can materially lower operating cost curves and regulatory risk exposure.

Competitive landscape: what leading suppliers are doing

The competitive map is shaped by a mix of legacy chemical majors, vertically integrated polysilicon producers, and regionally focused manufacturers. Our qualitative and transactional intelligence shows the following patterns:

- Integrated polysilicon players: Producers integrated into the polysilicon value chain are leveraging scale and captive offtake to optimize TCS feedstock utilization. Several have recently commissioned capacity ramp-ups and lower‑energy process units to strengthen cost leadership for solar-grade feedstock.

- Specialty chemical leaders: Long‑standing chemical companies are differentiating through high‑purity and low‑emission product lines, investing in purification capacity and targeting semiconductor demand with premium pricing and technical service agreements.

- Regional champions and policy beneficiaries: Firms operating in policy-favored jurisdictions are accelerating projects to qualify for incentive programs and to secure long-term contracts with domestic polysilicon or semiconductor customers.

Notable corporate moves in the past 18 months illustrate strategic priorities. Leading European and U.S. producers have brought online advanced purification capacity aimed at electronic‑grade customers, while Asian manufacturers have expanded manufacturing footprints and commissioned fluidized-bed reactor plants that materially cut energy intensity. Separately, a major U.S. polysilicon player secured significant governmental funding to expand domestic capacity—an example of how public programs can catalyze upstream TCS demand and reshape supplier economics.

Supply‑chain and regulatory headwinds

Several cross-cutting risks are shaping boardroom decisions for 2026:

- Feedstock availability and pricing volatility: Silicon metal supply remains the single largest cost and operational vulnerability. Recent months saw notable price swings and trade-policy responses that tightened import routes for some buyers and raised landed cost uncertainty.

- Environmental and chemical‑regulatory compliance: Enhanced regulatory requirements in key markets increase compliance costs and, in some cases, create temporary production constraints. Firms without proactive regulatory remediation plans face both operational and reputational risk.

- Geopolitical policy windows: Temporary suspension or tightening of export controls and anti‑dumping measures in various jurisdictions has shifted short-term supply balances; executives must distinguish transient disturbances from structural rerouting of feedstock supply chains.

For 2026 strategy, these dynamics translate into three executable risk mitigations: diversify feedstock sourcing while locking favourable multi-year contracts; accelerate capital projects that materially reduce energy and emissions intensity; and build compliance playbooks ahead of expected regulatory tightening.

What PW Consulting’s full report delivers (practical contents)

The full Industrial-Grade TCS market study is designed as a decision system rather than an academic exercise. Key, actionable components include:

- Proprietary market model with base‑year validation and scenario modules (sensitivity to feedstock price, capex timing and regulatory cost shocks).

- Demand-supply balance by end‑use and production pathway with operable triggers for capacity investment and tactical stocking.

- Price-curve forecast and margin-translation matrices that allow CFOs to stress-test contracts and hedges under policy and commodity scenarios.

- Plant-level economic templates (OPEX/CAPEX benchmarks, energy-intensity profiles, break-even maps) to support site-selection and retrofit decisions.

- Regulatory compliance checklist and playbook for major jurisdictions, including remediation cost estimates and timeline implications for production continuity.

- Supplier and technology scorecards for purification, reactor technology, and emission controls—useful for procurement RFPs and JV structuring.

- M&A and partnership screen highlighting target profiles, earn‑out structures and valuation sensitivities aligned to TCS economics.

- Executive decision playbook: prioritized actions by 90/180/360‑day horizons tuned to 2026 funding cycles and policy windows.

Importantly, the report preserves detailed regional and application splits, proprietary unit-cost curves and transactional comparables as gated content—intentionally withheld here to protect the underlying commercial value and to encourage direct engagement with our advisory team.

Prioritized strategic recommendations for 2026

Executives reading this briefing should consider the following priority moves to capture upside while insulating downside:

- Secure feedstock through blended strategies: Combine short‑term spot exposure with long‑dated offtake and small equity stakes in upstream suppliers. This reduces margin volatility and improves negotiating leverage for large offtake customers.

- Accelerate energy‑efficiency retrofits where IRR-positive: Investments in modern reactor technology and purification systems pay back faster when coupled with favorable power contracts—prioritise projects that reduce unit energy consumption and compliance risk.

- Structure conditional capacity expansions: Use milestone-based investment triggers tied to customer offtakes and incentive disbursements to protect balance sheets while ramping to meet demand.

- Leverage policy windows: Align capital and location decisions to funding opportunities and tariff regimes. Public programs can materially lower effective capex and enhance project returns if eligibility is proven early.

- Differentiate on service and supply assurance: Premiums are available to producers that can guarantee low variability, technical support, and consistent grade switching between industrial and higher‑purity batches.

- Embed regulatory foresight into M&A diligence: Factor in compliance-driven downtime risk and remediation costs when valuing assets—especially assets in jurisdictions with evolving chemical registration regimes.

Implications for 2026 budgets and governance

Board-level priorities for 2026 should explicitly assign ownership for three items: feedstock strategy, technology modernization, and policy engagement. Capital allocation should reflect the asymmetric value of early investments in energy‑efficient production and purification capacity—projects that materially lower operating costs while reducing regulatory exposure tend to de‑risk long-term supply contracts and create credible barriers to entry.

Next steps: how to use this insight

PW Consulting’s full market study provides the validated quantitative layers and proprietary segmentation that translate the directional insights above into executable decisions: detailed supplier scorecards, plant-level financial models, and transaction comparables that are intentionally not reproduced in this briefing. For C‑suite teams preparing 2026 budgets and strategic roadmaps, the immediate actionable step is to engage our advisory team for a tailored briefing that applies the report’s model to your company’s specific footprint, cost base and growth agenda.

In short: 2026 is a year to move from posture to execution. The macro growth trajectory and concentration profile create both opportunity and urgency. Leaders who secure feedstock, invest selectively in technology and operationalize regulatory compliance will capture disproportionate value as the market scales through 2032.

For detailed analysis of this topic, please visit the official page:Industrial Grade Trichlorosilane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com