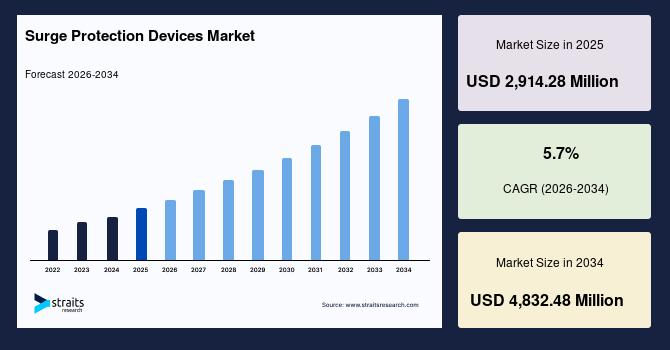

サージ保護デバイスの市場規模は、電気安全と電力インフラの近代化に対する需要の高まりによって、5.2によって2031億ドルに達する

Crafts |

2026-04-23 11:16:12

As executive teams prepare budgets and roadmaps for 2026, winter loungewear has quietly evolved from a pandemic-era comfort play into a structural market with clear growth dynamics and actionable battlegrounds. PW Consulting’s forthcoming Winter Loungewear Market report — based on a 2020–2025 historical baseline and a 2026–2032 forecast horizon — synthesizes primary retailer audits, supply‑chain mapping, consumer segmentation, and econometric demand modelling to deliver a pragmatic decision kit for apparel leaders, private equity investors, and strategic planners.

Winter Loungewear Market

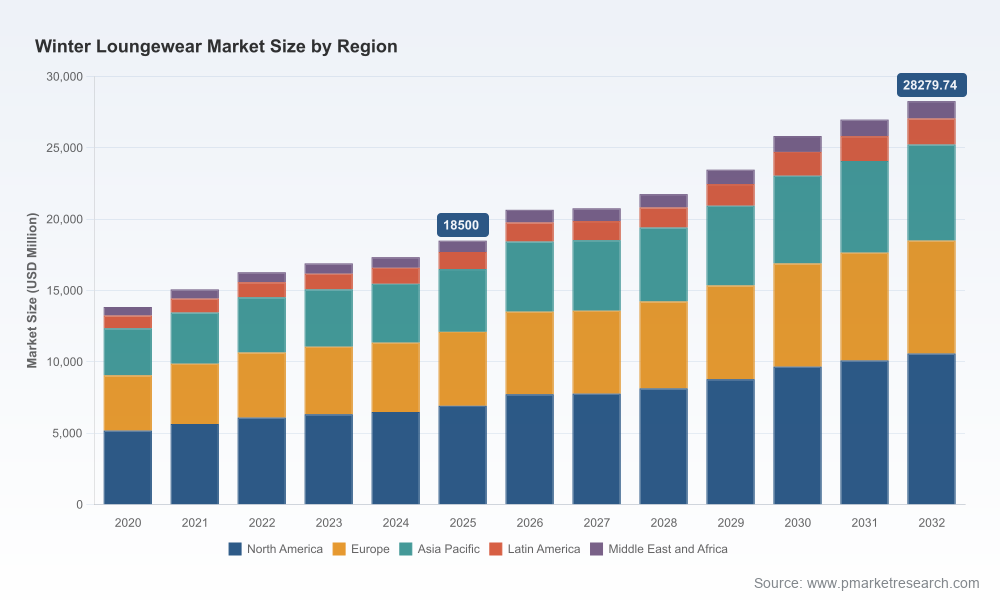

Scale and momentum: The winter loungewear market sits at approximately USD 18,500 Million in 2025 and is projected to expand into the low‑twenty billions in 2026 under a baseline scenario, driven by continued consumer demand for functional comfort, hybrid athleisure adoption, and expanding seasonal wardrobes.

Winter Loungewear Market

Reliable growth profile: Our forecast uses a central-case compounded annual growth rate of 6.25% across the 2026–2032 period, which implies sustained, investment‑grade expansion rather than a short‑lived fad. That pace justifies selective capacity investments, brand premiumization strategies, and channel reallocation for firms that can execute efficiently.

Winter Loungewear Market

Fragmented competitive structure: Market concentration remains low — the top three players account for only mid‑teens share (CR3 ≈ 16.4%) and the top five for under one quarter (CR5 ≈ 23.8%). This fragmentation creates continuous margin pressure but also leaves space for differentiated entrants and regional scale plays.

Material innovation as a demand hinge: Polyester‑based fleece continues to dominate functional winter loungewear because of cost-efficiency and thermal performance; global polyester production exceeded 78 million tonnes in 2024. At the same time, recycled polyester and blended sustainable fleeces are moving from a marketing message to a sourcing requirement for many retailers, driven by visible consumer preference shifts.

Channel bifurcation — margin vs reach: E‑commerce and direct‑to‑consumer models have matured into the primary channel for premium discovery and higher ASPs, while mass retail and department channels continue to drive volume on value propositions. The optimal channel mix in 2026 will be company‑specific and dependent on SKU architecture and inventory agility.

Design/price elasticity: Consumers reward hybrid features — improved fit, thermal grading, and multifunctional silhouettes — which enable modest price premium capture. However, the elasticity curve steepens in value segments, so SKU rationalization should be guided by a SKU‑level demand model rather than intuition.

Supply chain resilience and cost modeling: Volatility in cotton supplies (global production ~24.5 million tonnes in 2023/24) and rising demand for recycled inputs necessitate dual sourcing strategies, rounded cost‑pass‑through models, and near‑real‑time inventory analytics to avoid margin erosion in promotional windows.

Actionable market sizing and scenarios — top‑line forecasts to 2032 with three stress‑tested scenarios (baseline, upside innovation, downside trade shocks) and clear triggers that flip outcomes between scenarios.

Go‑to‑market playbooks — channel‑specific activation templates for DTC, wholesale, and mass retail; recommended assortment depth; first‑90‑day promotional calendar for winter launches; and conversion levers for subscription and membership programs.

SKU & pricing toolkit — elasticity curves by price band, margin waterfall templates, and recommended pricing zones for premium, core, and value lines (note: component‑level revenue splits and segment granularities are reserved for the full report).

Sourcing and supplier scorecard — mapping of high‑capacity polyester/fleece suppliers, recommended sustainability checkpoints (recycled content tiers, traceability), and a decision matrix for near‑shoring vs. low‑cost‑country strategies.

Consumer archetypes & product briefs — seven behavioral cohorts for winter loungewear buyers, corresponding design cues, and targeted marketing creative themes validated by A/B test benchmarks.

Competitive benchmarking — strategic positioning, product portfolio gaps, and potential weaknesses for incumbent and emerging brands, plus M&A and partnership targets prioritized by strategic fit and return horizon.

Implementation assets — slide‑ready investment memos, a 12‑month KPI scorecard template, and an Excel workbook with baseline demand curves and sensitivity toggles (note: full segment-level tables are accessible in the subscriber download).

The competitive field mixes legacy mass brands, aspirational DTC players, and fast‑fashion chains. Each category presents specific threats and opportunities for 2026 plans.

Value and staples: Companies like Hanesbrands Inc. (Winston‑Salem) and mass apparel divisions within larger retail groups continue to defend share through broad assortment and economies of scale. Their strength is supply continuity and unit economics at low price points.

Fast fashion and scale discounters: Global fast fashion players leverage rapid design cycles and aggressive pricing to capture impulse purchases for winter loungewear. Their speed to market is a structural advantage in seasonal categories.

Premium DTC and lifestyle: SKIMS (Los Angeles) and boutique labels such as Eberjey (Miami) focus on fabric hand, silhouette detail, and brand narrative. SKIMS’ recent initiatives — including a Team USA Winter Olympics collection (Jan 2026) and expanded holiday sets (Nov 2025) — demonstrate how lifestyle storytelling and limited drops can command premium, especially in gifting seasons.

Specialty premium & active hybrids: Aritzia (Vancouver) and Athleta (Gap Inc.) are blending performance fabrics with cozy aesthetics to seize premium share from both athleisure and classic loungewear buyers. These firms illustrate the margin upside of hybridization when coupled with membership models and loyalty programs.

Omnichannel majors: H&M (Stockholm) and Gap Inc. (San Francisco) operate across price bands. Old Navy’s recent Bounce Fleece launch (Dec 2025) is evidence that mainstream channels are investing in differentiated fabric technologies at scale to blunt premium encroachment.

Heritage premium: PVH Corp. leverages brand equity (e.g., Calvin Klein) to sell premium winter sleep and lounge offerings — a useful anchor in portfolio strategies that balance aspirational image with consistent wholesale distribution.

Strategic takeaways for market players:

Incumbents should prioritize margin defense through SKU rationalization and targeted premiumization while protecting volume with value offerings in core channels.

Challengers can win by owning fabric innovation narratives (e.g., validated recycled fleece performance), creating scarcity via limited‑edition drops tied to cultural moments, and deepening loyalty economics.

Retailers must treat winter loungewear as a seasonal platform category — central to gift strategies and winter merchandising — and align merchandising cycles with supply lead times to avoid overstock in late Q1.

Polyester capacity and recycled feedstock availability will determine cost volatility and product claims. With polyester production north of 78 million tonnes in 2024, supply exists — but recycled inputs and certified recycled content remain constrained relative to demand.

Cotton dynamics continue to influence blended constructions. While global cotton production was approximately 24.5 million tonnes in 2023/24, seasonal yield variability and competing demand for apparel vs. industrial uses create upstream pricing noise.

Regulatory and procurement standards — particularly EU and North American sustainability reporting frameworks — will push brands toward demonstrable recycled content and traceability, affecting supplier selection and cost pass‑through strategies.

Scenario‑based budgeting: Adopt the report’s three scenarios to define capex and inventory buffers. Link trigger points (commodity price thresholds, promotional conversion rates, channel GMV shifts) to automatic contingency actions.

Assortment surgery: Reallocate SKU density to top‑performing silhouettes and fabric families; pilot premium hybrids with controlled inventory to measure premium capture without full category exposure.

Sourcing hedges and supplier partnerships: Lock differentiated recycled‑fleece capacity with preferred suppliers and create dual sourcing lanes for staple cotton blends to reduce single‑supplier risk.

Retail & digital experiments: Use targeted DTC launches and influencer‑led drops to validate price bands and gather first‑party data for 2027 assortment scaling.

This preview outlines the strategic contours and executional levers that matter for winter loungewear in 2026. The full PW Consulting Winter Loungewear Market report contains the complete segmentation matrices, regional and channel breakdowns, SKU‑level elasticity models, and an Excel workbook with the underlying forecasts and sensitivity toggles — data we intentionally withhold here to preserve subscriber value.

Clients looking to translate these insights into a 90‑day action plan can engage PW Consulting for a tailored workshop, detailed competitor simulations, and immediate access to the full data annex and supplier scorecards. For organizations evaluating M&A or portfolio allocation, we offer targeted due diligence packages that overlay this market intelligence with company financials and product‑level margin simulations.

Winter loungewear is no longer a peripheral seasonal line — it is a structurally growing category with clear technical, channel, and sustainability inflection points. Companies that align design, sourcing, and channel economics to the market’s growth cadence in 2026 will convert trend into durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Winter Loungewear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com