Rative Dentistry Market — 2026 Strategic Preview for Executive Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present an executive preview of our Rative Dentistry Market report — a practical intelligence asset tailored to inform C-suite and corporate development decisions through 2026 and beyond. This briefing synthesizes market-scale dynamics, competitive shifts, regulatory inflections, and practical tools executives need to translate market signals into fast, defensible action. Designed as a strategic “trailer,” the piece demonstrates the report’s analytical depth while reserving core segmented findings for subscribers who require the detailed data to execute plans.

Rative Dentistry Market

Executive snapshot: scale, growth trajectory, and market structure

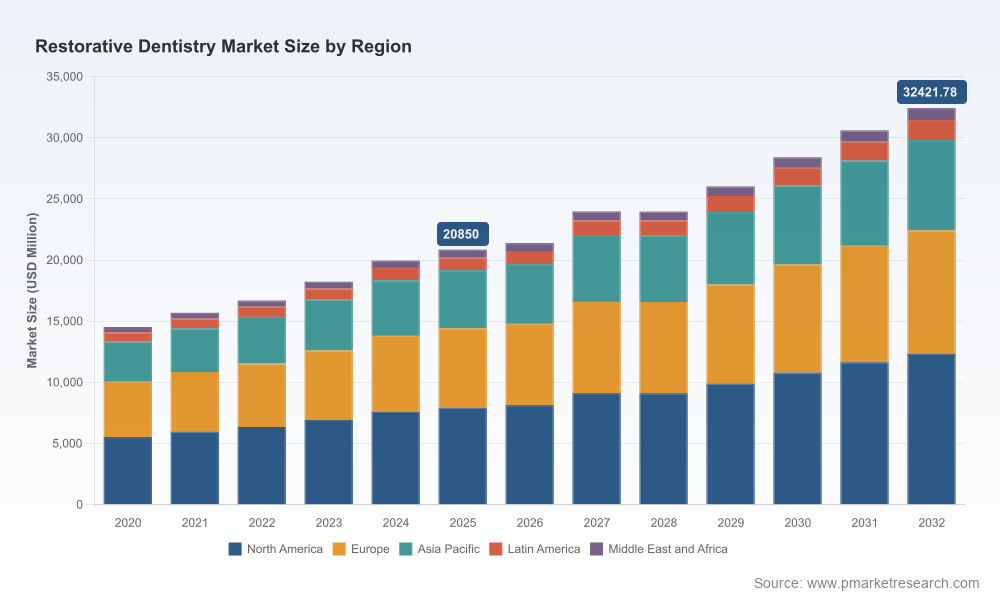

The Rative Dentistry market sits on a trajectory of steady expansion. Using 2025 as the analytical base year, our modeling shows the market approaching the low‑tens of billions of USD, and tracking at a compound annual growth rate (CAGR) of approximately 6.51% over the 2026–2032 forecast window. Under our base scenario the industry is projected to expand meaningfully through 2032, reflecting rising demand for restorative materials, digital restorative workflows, and incremental adoption of implant and prosthetic solutions.

Rative Dentistry Market

Competitive structure is moderately concentrated: the top global vendors capture a meaningful share of demand, yet the market remains open to targeted product innovation and regional consolidation. Our CR3 and CR5 concentration analysis confirms a marketplace in which scale delivers advantages—particularly for channel reach, R&D investment, and CAD/CAM platform bundling—but differentiated material science and service models create defensible niches for challengers.

Rative Dentistry Market

Why 2026 is a strategic inflection for industry players

- Regulatory and reimbursement momentum: New incentives and evolving wastewater and materials standards are changing capital and operating choices for care providers and manufacturers alike. Recent policy adjustments that encourage oral-screening integration and environmental controls are already influencing demand patterns and procurement specifications.

- Material and supply volatility: Rising costs and volatility in synthetic monomers and fillers are compressing margins in commodity composite lines, while simultaneously elevating the strategic importance of cost-stable, bioactive and higher-margin specialty materials.

- Digitalization and workflow integration: Investments in CAD/CAM, same-day restorative systems, and integrated digital platforms continue to re-shape purchasing bundles — benefiting firms that can monetize hardware/software ecosystems alongside consumables and services.

- Product innovation wave: The emergence of bioactive, ion‑releasing composites and enhanced restorative resins is shifting clinical preferences toward materials that demonstrably reduce secondary caries and extend restoration longevity—redefining clinical value propositions.

What the PW Consulting report delivers — operational intelligence for 2026 decision cycles

Our report is structured to be transactionally useful to strategy teams: it couples robust forecast modeling with execution-ready outputs. Key deliverables include:

- Top-line market forecast (2026–2032) with scenario variants reflecting macroeconomic, regulatory, and raw-material shocks.

- Competitive positioning maps and capability matrices for leading vendors, highlighting where each player is investing (digital platforms, implants, bioactive materials, CAD/CAM) and the commercial levers they are deploying.

- Go-to-market playbooks for three archetypes — global leaders, regional champions, and product innovators — with recommended sales motions, pricing tactics, and channel strategies tailored to 2026 dynamics.

- M&A and partnership screening: an annotated shortlist of inorganic opportunities, valuation sensitivities, and integration risk checklists to accelerate diligence and post‑merger value capture.

- Regulatory and reimbursement roadmaps that translate standards and policy updates into procurement triggers and product-compliance timelines.

- Granular qualitative insights from clinician panels and distributor interviews on drivers of product choice, switching barriers, and price elasticity in restorative and implant categories.

Competitive landscape: who’s moving and why it matters

Major incumbents continue to shape the market’s technology and channel contours. Several observable strategic themes emerge from recent company activity and disclosures:

- Platform consolidation by product leaders: Multi‑category firms are leveraging CAD/CAM and digital workflows to lock in consumable and prosthetic demand through bundled procurement models. Public disclosures from leading manufacturers indicate continued emphasis on integrated hardware‑software-consumable plays that enhance clinical throughput and create recurring revenue streams.

- Material differentiation drives clinical adoption: Companies investing in bioactive composites, remineralization-capable fillers, and next‑generation resin chemistries are gaining clinical interest; early launches and R&D disclosures highlight the commercial payoff of clinically demonstrable outcomes.

- Channel and brand strength remain decisive: Global reach, service infrastructure, and education programs are primary weapons in competitive battles for dental clinics and hospital accounts. Mid‑sized vendors that specialize in specific restorative niches retain opportunities to scale through targeted distributor partnerships.

Representative firms profiled in the research range from global leaders with full restorative portfolios and digital systems to specialized innovators focused on advanced materials and adhesives. Recent corporate activity — including quarterly results focused on restorative growth, annual reports emphasizing digital and regenerative solutions, and product launches of bioactive composites — underline that incumbents are actively repositioning portfolios to capture higher-value segments.

Risk map and regulatory watchlist — pragmatic actions for compliance and resilience

- Environmental and standards compliance: Wastewater management and device quality systems are no longer peripheral issues. Adoption of amalgam-separator standards and adherence to medical device quality systems are procurement gatekeepers in many markets. Companies should prioritize ISO standard alignment and proactive environmental certification to avoid market access friction.

- Raw material exposure: Volatility in monomer and filler supply chains will continue to erode margins in commodity lines. Hedging strategies, supplier diversification, and vertically aligned supply relationships are essential defensive measures.

- Reimbursement-linked access: Extensions to quality‑based physician reimbursement frameworks that include oral-health incentives open opportunities for restorative care pathways tied to screening programs; suppliers able to demonstrate outcomes-based value will secure preferential inclusion in bundled payment pilots.

- Emerging R&D solicitations: Public research calls for mercury-free, durable restorative alternatives are accelerating non‑amalgam innovation; participants should assess public‑private funding channels as accelerators for lower-cost, high‑performance materials.

How C-suite teams should use this intelligence in 2026

Translate the report’s insights into four immediate actions for 2026 planning cycles:

- Reset portfolio investment priorities: Reallocate R&D and marketing spend towards bioactive and digital-compatible products where clinical differentiation is emerging and price premium potential exists.

- Revise go-to-market economics: Update channel compensation and service offerings to reflect greater demand for bundled digital workflows and outcome‑focused solutions in institutional accounts.

- Pursue targeted partnerships and acquisitions: Prioritize bolt‑on deals that fill capability gaps in materials science, digital prosthetics, or regional distribution — using the report’s M&A screening to short‑list and stress-test targets.

- Operationalize compliance and sourcing resilience: Implement a two‑stream procurement strategy that isolates critical raw materials, and accelerate certification programs to match regional regulatory timetables.

Methodology and confidence markers

Our analysis synthesizes multi‑year historic sales data, primary interviews with clinical and distributor stakeholders, patent and product‑launch tracking, and a robust scenario model that reflects material-cost shocks, regulatory shifts, and adoption lags for new restorative technologies. The base year of analysis is 2025, historical coverage extends from 2020 through 2025, and the forecast horizon spans 2026–2032. Confidence in the headline trajectory is supported by cross‑validation of vendor disclosures, clinician uptake signals, and macroeconomic sensitivity testing.

What we are intentionally holding back — and why

To respect the “trailer” nature of this executive preview, we have deliberately withheld the granular segment breakouts, regional share tables, and proprietary price‑deck matrices that underpin tactical execution. These core segment datasets — which include disaggregated product, regional and end‑user splits, and price sensitivity curves — are included in the full report and are the precise levers executives will use for budgeting, commercial modeling, and M&A valuation. This preview is designed to demonstrate the strategic value and signal reliability; the full report delivers the operational detail.

Next steps — turning insight into competitive advantage

Leaders who act quickly in 2026 will capture disproportionate returns by aligning R&D, channel, and compliance initiatives to the evolving restorative care landscape. PW Consulting’s Rative Dentistry Market report offers the analytical depth and actionable templates necessary to convert the growth trajectory into sustainable market share and margin improvement. For teams preparing 2026 strategic plans, the report functions as both a market roadmap and an execution playbook.

To access the full dataset, segmented forecasts, and executable playbooks that support the above conclusions — including the purchase-ready M&A shortlist and the supplier‑risk heatmaps — please visit the report landing page or contact our research desk for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Rative Dentistry Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com