Industrial-Grade Gamma-Butyrolactone (GBL) Market: Strategic Imperatives for 2026 — PW Consulting Insights

As companies prepare strategic priorities for 2026, gamma-butyrolactone (GBL) has re-emerged as a quietly strategic industrial intermediate and solvent across multiple high-value value chains — from electronics and battery materials to specialty coatings and agrochemicals. PW Consulting’s newest Industrial Grade Gamma Butyrolactone (GBL) Market report (base year 2025; forecast horizon 2026–2032) synthesizes five years of historical behavior with forward-looking scenarios to deliver practical decision-support for commercial, procurement, technical and M&A leaders.

Industrial Grade Gamma Butyrolactone Gbl Market

Market trajectory at a glance: what senior leaders need to know

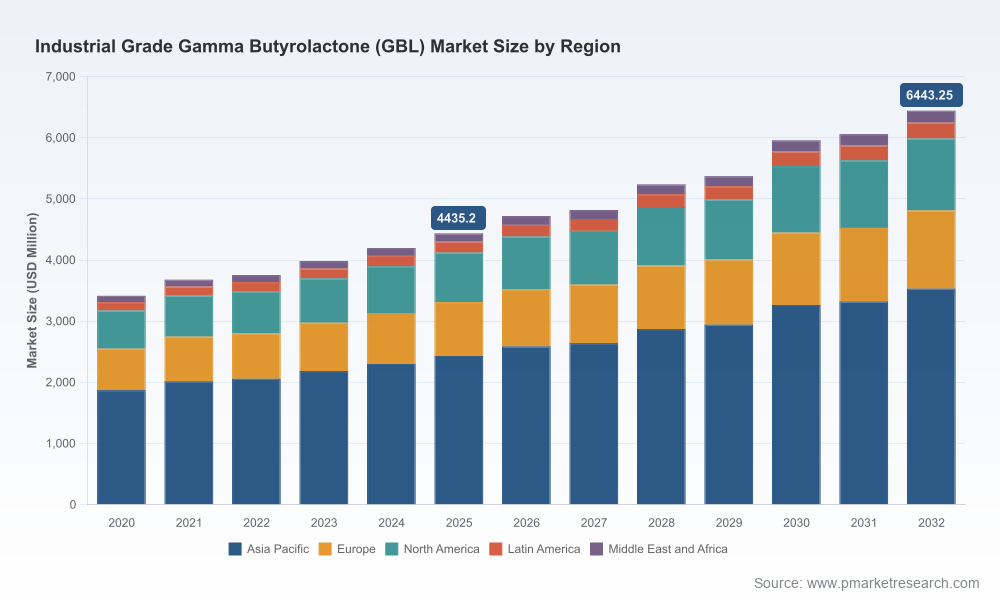

At the macro level, the industrial-grade GBL market stands on a steady expansion path. Our base-year assessment for 2025 values the market in the mid‑single‑billion range (USD Million), and our forecast through 2032 points to material growth driven by demand recovery and structural shifts in downstream industries. The modeled compound annual growth rate for the forecast window is 5.48%, leading to a meaningful increase in absolute market size by 2032. Concentration metrics show an industry that is neither fully commoditized nor dominated by a single player: the top three suppliers account for roughly half of market share, while the top five command a clear majority, indicating both scale advantages and opportunities for niche differentiation.

Industrial Grade Gamma Butyrolactone Gbl Market

Why this matters for 2026 planning

- Timing of investments: The market’s steady CAGR and anticipated step‑ups in downstream demand create a narrow window in 2026 where targeted capacity additions or reliability investments can capture incremental margins without triggering supply gluts. Strategic players should prioritize flexible, debottleneckable investments over large inflexible brownfield builds.

- Procurement strategy: Feedstock volatility and regional supply dynamics mean procurement should shift from simple spot purchasing to layered strategies — combining medium‑term contracts, index‑linked clauses, and feedstock‑linked hedges to protect gross margins while maintaining availability for critical customers.

- Customer segmentation and offtake: Buyers in battery, semiconductor and specialty chemical sectors increasingly prioritize high‑purity grades, sustainability attributes and supply assurances. Winning 2026 tenders will require a combination of product quality, traceable feedstock claims, and commercial flexibility.

- Regulatory readiness: GBL’s regulatory treatment varies by jurisdiction; compliance preparedness is a non‑negotiable risk mitigant. Companies must operationalize controls, documentation and customer gating mechanisms to avoid costly slowdowns or trade disruptions.

Actionable tools and modules included in the PW Consulting report

We designed the report as a practitioner’s toolkit. Beyond market sizing and high‑level forecasting, the deliverable contains a suite of operational models and playbooks that leadership teams can deploy immediately:

Industrial Grade Gamma Butyrolactone Gbl Market

- Supply‑demand engine with scenario capability: A customizable model that allows users to stress test demand trajectories (e.g., battery adoption paths, semiconductor capital cycles) and simulate the impact of capacity additions, outages, and feedstock shocks on regional balances and realized prices.

- Price sensitivity and margin toolkit: Rolling margin calculators tied to BDO feedstock inputs and major cost centers help product managers and pricing teams set resilient commercial terms under different macro outcomes.

- Contract playbooks: Drafted contractual clauses and negotiation playbooks for offtake, tolling, and feedstock supply arrangements — including recommended language for indexation, force majeure, product specifications, and audit rights.

- Regulatory compliance checklist: Practical steps for operationalizing jurisdictional controls, recordkeeping, and customer due diligence — designed to reduce the time between contract signature and commercial supply.

- Capex screening and ROI templates: Decision matrices that combine CAPEX, time-to-market, expected utilization curves and price outlooks to prioritize projects that maximize net present value under conservative scenarios.

- M&A and JV playbook: Due diligence question sets, integration risk maps and synergy quantification templates tailored to GBL assets and adjacent BDO/THF nodes.

- Sustainability benchmarking: A rapid assessment template for scope, product‑level carbon footprints and supplier claims — enabling commercial teams to respond to buyer requests for low‑PCF or biomass‑balanced variants.

Competitive landscape — what the market structure implies

Our competitor analysis synthesizes plant footprints, feedstock integration, product portfolios and strategic moves announced through early 2026. Several themes emerge that should shape counter‑party evaluation and go‑to‑market choices in 2026:

- Integrated incumbents focus on chain control: Large, vertically integrated chemical companies that link BDO production to downstream GBL output (through continuous processes and proprietary routes) retain margin advantages in feedstock access, quality control and sustainability claims. These players often target high‑purity, high‑value industrial applications where reliability matters.

- Specialty suppliers compete on formulation and service: Specialty chemical producers emphasize tailored product grades, regional customer service and regulatory know‑how to win in agrochemical, electronics and niche industrial segments.

- Chinese and regional manufacturers drive cost competition: Regional producers in Asia continue to expand and refine capabilities, increasing supply options for nearby demand centers while also pushing value chain innovations to meet higher‑purity and documentation expectations.

- Recent commercial moves set the tone for 2026: A recent global price adjustment by a major North American supplier — attributable to feedstock pressures and macro factors — highlights the sensitivity of commercial terms to upstream cost changes. Similarly, targeted capacity expansion by a major Japanese producer underscores the strategic value placed on high‑purity supply for electronics and battery ecosystems. Sustainability and product stewardship disclosures from leading European producers demonstrate that buyers will increasingly evaluate suppliers on lifecycle claims, not just price.

Strategic plays for different company archetypes

How should leaders act in 2026? Recommendations vary by company profile:

- Integrated majors: Defend margins through improved feedstock contract structures, accelerate decarbonization claims where they support premium pricing, and pursue selective regional capacity additions that prioritize product quality and logistics efficiency.

- Specialty players: Differentiate on high‑purity formulations, regulatory service, and speed-to-market for custom grades. Consider tolling or co‑processing arrangements to broaden market reach without heavy upstream investment.

- Buyers and formulators: Lock in dual‑source contracts with preferred suppliers that can demonstrate continuity, quality traceability, and regulatory compliance. Design product roadmaps that can flex between grades where appropriate to exploit pricing cycles.

- Private equity and M&A investors: Screen targets for feedstock flexibility, plant operability, and customer concentration. Value creation will come from optimizing commercial contracts, upgrading product stewardship credentials, and deploying bolt‑on specialty co‑products.

Risks and mitigation — practical checklists for 2026

Our analysis identifies a limited set of high‑impact risks and countermeasures that management teams should operationalize immediately:

- Feedstock price volatility: Implement layered procurement and hedging strategies, and model margin sensitivity across realistic short‑term swings.

- Regulatory shifts: Maintain a jurisdictional register and escalate potential changes to senior management; embed compliance conditions in commercial contracts to avoid stranded shipments or delayed approvals.

- Concentration and supplier dependence: Develop contingency sourcing lanes and qualify tolling partners to mitigate single‑supplier exposure.

- Quality and specification drift: Institute rigorous incoming and outgoing quality checks and clarification processes for grade transitions to prevent customer disruption.

How the report supports boardroom decisions in 2026

Boards and executive teams will use this report to anchor three types of decisions: (1) capital allocation — where to place scarce growth dollars for capacity or reliability; (2) commercial strategy — how to price, contract and segment customers given evolving buyer priorities; and (3) risk management — how to design procurement, regulatory and operational defenses. The combination of a transparent macro baseline (base year 2025, forecast 2026–2032 at a modeled CAGR of 5.48%), concentration indicators and scenario tools allows leaders to make defensible, auditable choices under uncertainty.

Next steps — where PW Consulting adds immediate value

Clients who require expedited decision support can engage PW Consulting for rapid extensions of the core report: custom regional demand models, bespoke supplier due diligence, M&A target screens, negotiation support for offtake contracts, or a condensed board briefing. For organizations that prefer a self‑serve approach, the report’s downloadable toolkits and templates are designed to be operational from day one.

PW Consulting’s Industrial Grade Gamma Butyrolactone (GBL) Market report is intentionally structured as a “trailer” — it provides the strategic framing, actionable playbooks and diagnostic tools that senior teams need to move decisively in 2026 while directing readers to the full report for the granular, transaction‑level data that underpins our recommendations. For access to the complete dataset, regional tables, purity‑grade splits, and downloadable models, please consult the report landing page.

Authors: PW Consulting — Senior Strategic Advisory and Industry Analysis Teams. For inquiries about bespoke analyses or executive briefings, contact our Chemical Materials practice.

For detailed analysis of this topic, please visit the official page:Industrial Grade Gamma Butyrolactone Gbl Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com