Electric Tailgate Radar Market — Strategic Outlook for 2026: What Decision‑Makers Must Know

Executive summary

The electric tailgate radar market has moved from niche convenience feature to a strategic node at the intersection of vehicle safety, user experience, and sensor convergence. Our latest market study at PW Consulting shows the market more than doubled in five years, expanding from roughly USD 312 million in 2020 to about USD 620 million by 2025, and we project continued expansion to slightly above USD 1.1 billion by 2032. That trajectory implies a healthy compound annual growth rate of 8.65% through the 2026–2032 forecast window. For 2026 specifically, the market is set to cross the mid‑hundreds of millions of dollars as early adopters scale to series production and new platforms integrate hands‑free access as standard.

Electric Tailgate Radar Market

Why this matters for 2026 corporate decisions

Electric tailgate sensors are no longer an accessory-line item; they are an architectural choice that impacts vehicle BOM structure, supplier selection, compliance timelines and end‑user differentiation. OEMs face pressure to deliver robust hands‑free entry while meeting tighter functional safety and frequency-management rules. Tier‑1s and semiconductor suppliers must decide whether to prioritize investment in millimeter‑wave (mmWave) sensor designs, pursue multi‑modal fusion with UWB and proximity sensors, or double down on software differentiation such as gesture recognition and false‑trigger mitigation.

Electric Tailgate Radar Market

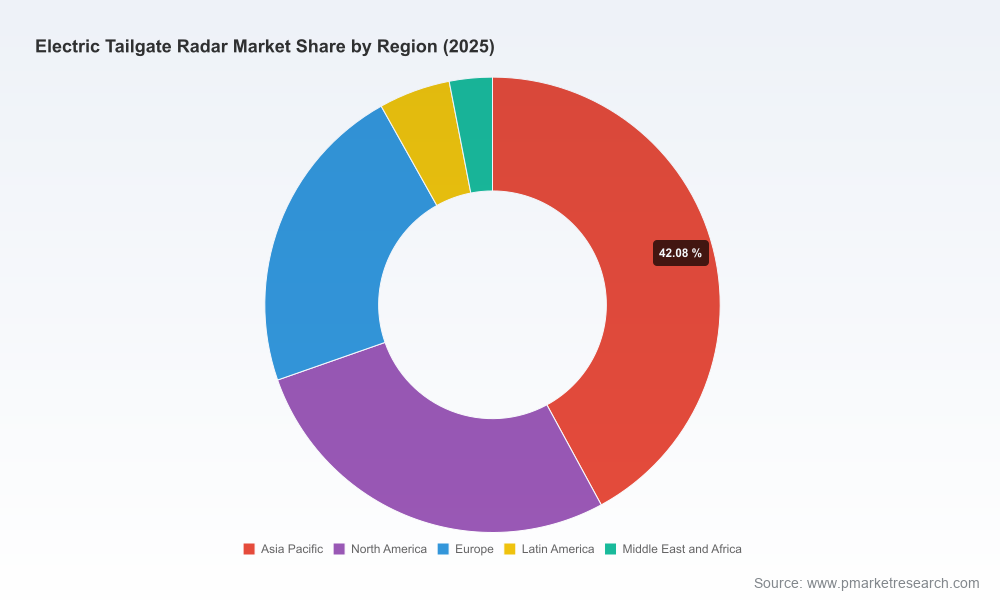

Decisions made in 2026 will influence program economics across multiple product generations. With the market concentration currently moderate (the top three suppliers hold roughly 42% and the top five roughly 59% of market share), there is room for both incumbent expansion and targeted entrants to capture niche or regional opportunities — provided they move quickly on certification, integration, and cost engineering.

Electric Tailgate Radar Market

Key demand and technology drivers

- Consumer expectation for reliable hands‑free operation combined with safety requirements for obstacle detection is driving adoption on mainstream vehicle segments.

- Regulatory activity around frequency allocation (notably 79 GHz rulesets) and functional safety (ISO 26262 ASIL requirements for obstacle detection) is shaping preferred technical architectures and time‑to‑market constraints.

- Semiconductor supply stabilization has materially shortened lead times for mmWave chips, improving the feasibility of multi‑sourcing strategies for 2026 program starts.

- Sensor fusion — combining mmWave radar with UWB or proximity sensors — is emerging as the performance differentiator for premium implementations and for mitigating false activations in crowded urban environments.

What’s in the PW Consulting report (practical, decision‑grade deliverables)

- Proven market sizing and an actionable forecast model (2026–2032) with scenario toggles for regulatory, supply‑chain, and adoption rate variances.

- Vendor scorecards across performance, cost, production readiness, certification track record, and integration support — designed to shorten your supplier selection cycle.

- Technology roadmaps that map sensor performance (range, angular resolution, processing latency) to use‑cases (gesture recognition, obstacle stop, parking assist) so product managers can prioritize investments.

- Procurement playbooks and TCO templates that quantify program impact across modules, software licenses, and service agreements — enabling negotiation with clear levers to reduce BOM cost.

- Regulatory and homologation checklists for 79 GHz deployments and ISO 26262 conformance, with a recommended timeline to complete certifications for 2026 production ramps.

- Risk heatmaps (supply, regulatory, obsolescence) and mitigation plans for each critical path — particularly useful for platform launches in 2026 and 2027.

Competitive landscape: who’s influencing program decisions in 2026

The market is shaped by a mix of automotive systems integrators, specialized radar vendors, and semiconductor suppliers. Strategic positioning differs: some players compete on high‑precision mmWave performance for premium models, others on cost‑efficiency and supply reliability for high‑volume mainstream platforms.

- Huf Group (Velbert, Germany) — A strong playbook in series production for 79 GHz radar kick sensors positions Huf as an attractive partner for OEMs seeking compact, high‑accuracy solutions with proven gesture recognition. Their 2025 series production win signals readiness for scaled deliveries and reduced integration risk for 2026 launches.

- InnoSenT GmbH (Donnersdorf, Germany) — Specialist radar capabilities focused on contactless tailgate actuation underscore InnoSenT’s role as a focused supplier for integrators who prioritize radar‑centric sensing solutions. Their vertical expertise is valuable for programs that place a premium on radar performance tuning.

- Continental AG (Hanover, Germany) — As a systems integrator with broad sensor portfolios, Continental competes on integrated safety functionality and aftermarket scalability. Their solutions appeal to OEMs looking to consolidate supplier count and leverage cross‑domain integration.

- Brose Fahrzeugteile (Coburg, Germany) — Brose’s drive systems and sensor interfaces, showcased with UWB and multi‑sensor demos, make them a strategic partner for clients seeking end‑to‑end tailgate subsystems where mechanical and sensor integration are co‑designed.

- Aisin Corporation (Kariya, Japan) — Strong OEM ties in Asia and a focus on reliable power tailgate assemblies with integrated sensing make Aisin a preferred partner for regional platforms where localization and supply consistency matter.

- Texas Instruments (Dallas, USA) — As a mmWave semiconductor supplier, TI’s chips are enablers for many Tier‑1 and OEM prototype programs. Their roadmap and supply capabilities will be decisive for suppliers planning multiple sourcing strategies into 2026.

- Other notable movers — Recent product and production milestones from non‑traditional entrants (UWB SoC vendors, advanced signal‑processing start‑ups) are changing the competitive dynamics by offering hybrid solutions that combine radar, UWB and AI‑based filtering.

Recent industry signals you cannot ignore

- May 2025 — A series production order for 79 GHz tailgate radar (announced by a major radar supplier) confirms that mmWave systems are moving from validation to OEM production allocations.

- April 2025 — Demonstrations at major auto shows highlighted integrated power‑tailgate systems pairing UWB and radar, underscoring a trend toward sensor fusion as a market differentiator.

- Supply chain update (Q1 2026) — Semiconductor lead times for mmWave radar chips improved markedly, creating a practical window for new supplier qualification ahead of many 2027 programs.

- Standards & safety — Evolving frequency allocation guidance and ISO 26262 functional safety expectations are narrowing the field for compliant, certifiable solutions in 2026 product cycles.

Regulatory and supply‑chain considerations

Deployments centered on 79 GHz must navigate updated UN ECE and regional frequency rules, and engineering teams must plan for certification resources early in program timelines. From a safety perspective, radar modules integrated into obstacle detection loops will require documented ISO 26262 evidence at ASIL levels that are increasingly enforced by OEM QA teams. On the supply side, semiconductor stabilization reduces one common bottleneck — but it raises another: software and integration capacity (the ability to tune radar performance for varied bumpers, metals and environmental conditions).

Actionable recommendations for 2026 (prioritized)

- Secure mmWave chip supply via dual sourcing and framework agreements in H1 2026. Where possible, include capacity reservation clauses tied to production ramps.

- Accelerate functional safety workstreams: start ISO 26262 artifacts and homologation plans during concept phase to avoid late-stage rework.

- Adopt a “fusion first” architecture for premium and high‑noise environments: pair radar with UWB/proximity sensors and edge‑based filtering to improve reliability and reduce false positives.

- Use the PW Consulting supplier scorecards to shortlist partners that match your production geography, certification experience, and software support capabilities — then run rapid pilot programs with defined KPIs for reliability and false‑trigger reduction.

- Evaluate strategic M&A or JV targets among specialist radar vendors to vertically integrate key IP and shorten time‑to‑market for differentiated sensing stacks.

How PW Consulting’s report accelerates execution

Our market model and recommended playbooks translate market projections and competitive intelligence into executable steps for procurement, product management, and corporate development teams. The report’s modular deliverables — including a downloadable forecast model, supplier shortlists and a certification timeline — are designed to be embedded directly into 2026 program planning cycles. To preserve actionable negotiation leverage for our clients, we surface all the inputs and scoring logic; in this public executive summary we withhold granular supplier price matrices and region‑by‑application revenue splits, which are provided in the full report and associated data pack.

Conclusion and next steps

For companies deciding 2026 roadmaps — whether OEMs, Tier‑1s or component specialists — the electric tailgate radar market represents a fast‑moving opportunity that couples consumer UX with regulatory and safety constraints. The path to commercial success will be won by organizations that align procurement, engineering and compliance early, and that choose the right partners supported by robust vendor scorecards and scenario planning. PW Consulting’s full Electric Tailgate Radar Market report provides the granular segmentations, supplier benchmarks and financial models needed to operationalize these recommendations; access to the complete dataset and supplier intelligence is available through the report’s source page.

For detailed analysis of this topic, please visit the official page:Electric Tailgate Radar Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com