PW Consulting Strategic Brief: Nylon Rod Market — 2026 Playbook for Action

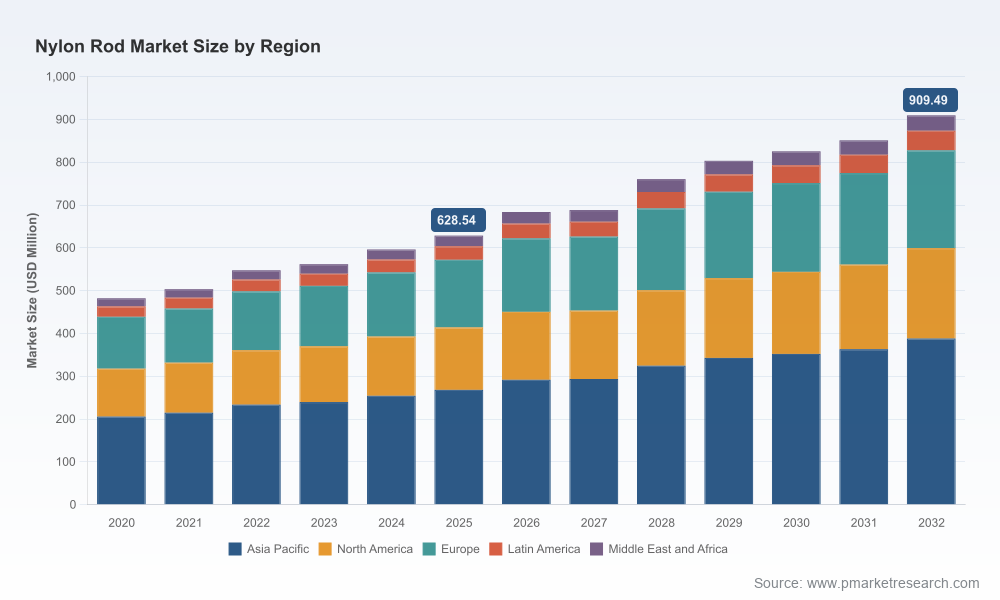

As organizations prepare budgets and capital plans for 2026, the Nylon Rod market is entering a phase where stable growth meets renewed structural risk. Our new market study places the global Nylon Rod market at approximately USD 628.5 Million in the base year 2025 and projects expansion to about USD 909.5 Million by 2032, representing a compound annual growth rate (CAGR) of 5.42% across the forecast horizon. These headline numbers conceal a dynamic ecosystem: shifting raw-material economics, tightening regulatory regimes in developed markets, and a competitive field that is neither fully fragmented nor locked in by a handful of incumbents (CR3 ≈ 32.5%; CR5 ≈ 48.1%). This briefing summarizes the strategic implications for 2026 and outlines the practical steps industrials, suppliers, and investors should prioritize — while preserving the granular tables and model outputs for subscribers to the full report.

Nylon Rod Market

Why this report matters for 2026 decision cycles

Procurement cycles, product roadmaps, and capacity investments decided in 2026 will be shaped by three concurrent forces: mid-single-digit market growth, episodic raw-material volatility, and intensifying regulatory scrutiny related to chemical feedstocks and emissions. For executives, the choices made this year should not only defend margins but also preserve optionality — for example, the ability to re-route supply, accelerate higher-margin customized grades, or respond rapidly to regional trade measures. The PW Consulting Nylon Rod study is designed as a decision-useful tool: it translates market forecasts into capital planning scenarios, commercial scorecards, and supplier playbooks tailored to different enterprise profiles.

Nylon Rod Market

What the study delivers (practical contents)

- Transparent market sizing and scenario models — base, upside, and downside cases — with driver-level levers you can run in-house.

- Supply-chain heat maps and vulnerability scoring for key feedstocks and intermediate chemistries.

- Commercial playbooks for producers and distributors: pricing play, channel segmentation, and OEM engagement frameworks.

- CapEx decision frameworks for plant expansion, including IRR sensitivity to raw-material price swings and regional regulatory costs.

- Regulatory-impact simulations — including N2O/accounting exposures under EU frameworks and cross-border carbon adjustment mechanisms — to quantify future compliance costs by scenario.

- Competitive diagnostic dossiers for the top global and regional players, inclusive of capability matrices, certification footprints, and suggested strategic responses.

- Go-to-market and product-portfolio blueprints for moving up the value chain (modified nylons, value-added machining, and managed inventory services).

Note: In keeping with the ‘trailer’ principle, this public brief deliberately omits the report’s detailed regional/application splits, company market shares and the full financial model. Those datasets and downloadable model files are available in the full report.

Nylon Rod Market

Key dynamics to track in 2026

- Raw-material cost volatility — Caprolactam and adipic acid remain the primary cost drivers for PA6 and PA6,6-based product flows. Recent supplier actions and regional price movements are already feeding margin pressure and will influence contract-renewal negotiations in 2026. A notable producer has signaled price increases for caprolactam and polyamide 6 in North America effective April 2026 — a development procurement teams must model into supply contracts and pass-through clauses.

- Feedstock market rebalancing — In parts of Asia, adipic acid pricing showed downward movement in late 2025 amid weakened demand from certain nylon value chains. That kind of regional decoupling can generate localized arbitrage opportunities but also abrupt policy responses when local producers feel threatened.

- Regulatory and trade risk — Carbon-pricing frameworks that affect upstream caprolactam and related N2O emissions are expanding; European mechanisms and border adjustment proposals are already altering sourcing calculus for firms selling into or operating inside the EU. Concurrently, antidumping and trade investigations in basic chemical feeds are creating bilateral trade uncertainty that could raise landed costs or disrupt continuity.

- Demand composition and premiumization — End-market demand remains resilient in industrial machinery and transportation OEM channels, with growth driven by both volume replacement cycles and increased specification of engineered/modified nylon grades. This supports a strategic pivot for suppliers toward higher-margin, value-added services.

Competitive landscape: who matters and what they signal

The market structure favors a mix of specialized technical producers and geographically integrated suppliers. Key companies profiled in the study include Nylatech, Inc., Ensinger GmbH, Cast Nylons Limited (CNL), Modern Plastics, Dura Polymers, Ningbo Yinzhou Qishan, Emco Plastics, Piedmont Plastics, Professional Plastics, and Trident Plastics. Our competitive diagnostics highlight several differentiated strategic postures:

- Specialist manufacturers (e.g., Nylatech, Cast Nylons, Ensinger) emphasize technical depth in cast and engineered grades, certified supply chains, and extensive machining/fabrication services — positioning them to capture premium projects in heavy industry and defense applications.

- Regional producers and distributors (e.g., Modern Plastics, Emco, Piedmont) compete on speed-to-market, certification breadth (FDA, ISO, AS), and localized inventory programs — strengths that matter for just-in-time OEMs and food-processing customers.

- Emerging-volume players in Asia (including several ISO-accredited manufacturers) combine cost competitiveness with expanding capacity; their moves are central to near-term regional supply dynamics and pricing pressure.

Market concentration statistics show that the top three and top five suppliers control material but not overwhelming share — a structure that supports both competition and selective consolidation opportunities for strategic buyers and private equity.

Actionable recommendations for 2026 (executive checklist)

- Re-run procurement models with multiple raw-material scenarios. Embed a $/tonne and $/lb sensitivity into supplier contracts and evaluate short-term hedging for caprolactam where available.

- Adopt a supplier segmentation and dual-sourcing strategy for high-risk chemistries. Prioritize alternate routes for critical intermediates and create “switch” protocols for rapid qualification of second-source materials.

- Accelerate product premiumization. Redirect engineering resources to modified nylons, metal-detectable grades, and self-lubricating variants where margin collars are wider and technical lock-in is stronger.

- Quantify regulatory exposure. For firms with EU-facing sales, run CBAM/N2O impact scenarios now and budget for incremental compliance or relocation costs as necessary.

- Inventory and working-capital optimization. Consider targeted safety stock increases for high-use grades and deploy vendor-managed inventory (VMI) in strategic hubs to reduce lead-time risk.

- Pursue asset-light service models. For distributors, move up the chain into kitting, machining-as-a-service, and certified clean-room supply for food and pharma customers.

- Assess consolidation and partnership targets. Given mid-market fragmentation, selective M&A that adds value-added machining or regional footprint can yield scale benefits and margin uplift.

- Invest in traceability and sustainability credentials. Certifications and low-carbon product passports will differentiate suppliers in regulated markets and among OEMs with supply-chain decarbonization targets.

Use cases that shape portfolio choices

Demand is being driven by a mix of legacy replacement and new-specification growth. Industrial machinery and transportation segments are driving durable demand for structural and wear-resistant rod grades, while electronics and food-contact applications continue to raise specification and traceability requirements. Suppliers and buyers should therefore allocate development resources based on end-market elasticity and margin potential rather than volume alone.

How PW Consulting supports execution

PW Consulting’s Nylon Rod study is built to move clients from insight to action. Subscribers receive the full dataset, downloadable financial models, supplier scorecards, and a 90-day implementation roadmap tailored to their role (procurement, commercial, or corporate development). Our advisory packages include scenario workshops, supplier negotiation support, and transaction advisory for M&A targets identified through the study’s proprietary screening.

For procurement leaders, the immediate value is the ability to test supplier and pricing levers against realistic raw-material and regulatory scenarios. For strategic planners and investors, the value is in the combination of growth trajectories and concentrated pockets of opportunity that justify targeted capital deployment in 2026.

Next steps

To access the complete Nylon Rod Market report — including the full regional and application splits, company market shares, and the downloadable scenario model — please visit the PW Consulting reports portal or contact our industry team to schedule a live briefing and model walkthrough. The headline forecasts and strategic levers summarized here are decision-useful; the full report will convert them into executable 90–180 day plans tailored to your organization’s risk appetite and commercial objectives.

For detailed analysis of this topic, please visit the official page:Nylon Rod Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com