Chip Encapsulation Resin Market: Strategic Intelligence for 2026 — A PW Consulting Executive Brief

As semiconductor packaging complexity accelerates and the electrification of end markets deepens, the chip encapsulation resin market is moving from incremental commodity dynamics to strategic foundations of reliability, thermal performance and supply resilience. PW Consulting’s latest market research — covering 2020–2025 historical performance and a 2026–2032 forecast — quantifies these shifts and translates them into an executable agenda for C-suite and investment teams planning for 2026. This executive brief outlines the report’s strategic value, highlights high‑impact market signals, and summarizes the competitive and supply‑chain implications clients must act on now.

Chip Encapsulation Resin Market

Market Snapshot: Macro Trajectory and Concentration Dynamics

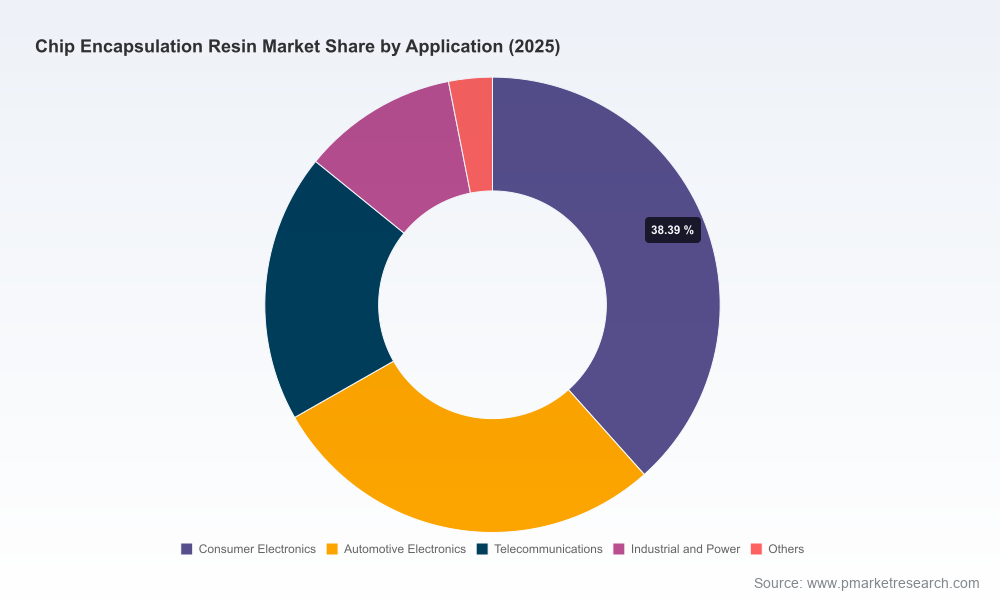

Our model shows the global chip encapsulation resin market at approximately 3,892.6 USD Million in the base year (2025), with a compounded annual growth rate (CAGR) of 6.81% across the 2026–2032 forecast window. By 2032 the market trajectory points to a materially larger opportunity as packaging density, power handling and environmental reliability requirements expand across AI accelerators, automotive electrification and 5G/6G infrastructure applications.

Chip Encapsulation Resin Market

Market concentration is meaningful: the top three suppliers command a majority share (CR3 ~54.2%), and the five largest players capture over three-quarters of the market (CR5 ~76.5%). This structure creates clear competitive advantages for scale players — particularly in securing specialty feedstock allocations, financing advanced production assets, and influencing qualification roadmaps with key OEMs — while leaving room for nimble specialists to capture pockets of premium growth.

Chip Encapsulation Resin Market

Why This Report Matters for 2026 Decisions

- Timing of Capacity Investments: The combination of persistent demand growth and concentrated supplier structure means decisions on greenfield capacity, brownfield debottlenecking, or JV partnerships in 2026 will determine supply positioning for the next cycle. Our scenarios quantify lead‑times and break‑even utilization thresholds across upstream resin chemistries.

- Product Roadmaps and Premiumization: Thermal conductivity, low alpha emissions, high glass transition temperature (Tg), and moisture resistance are no longer niche — they are prerequisites for success in EV power modules and AI packaging. The report matches material performance archetypes to packaging use cases and risk‑adjusted margin uplifts to guide R&D prioritization.

- Procurement and Hedging Strategies: Raw material volatility and regional trade measures are compressing margins unpredictably. Our analysis provides procurement playbooks — from strategic long‑term supply agreements to formula‑level substitutions — and stress‑tests P&L under multiple feedstock price scenarios.

- M&A and Partnering Signals: Given high CR5 concentration, targeted acquisitions of specialty grades, regional capacity, or niche polymer IP can shortcut time to market. The research lays out acquisition screens and integration risks for 2026 deal pipelines.

High‑Impact Market Signals — What We Observed

- Demand Drivers: Packaging complexity (multi‑die, heterogeneous integration), rising thermal loads in power electronics, and stringent reliability needs in automotive and data center applications are the principal demand multipliers.

- Supply Actions by Leading Players: Major incumbents have accelerated capacity investments and product launches aimed at high‑reliability segments. Recent industry moves include large-scale capacity expansions and commissioning of new plants intended to serve AI and automotive power markets.

- Raw Material Dynamics: Feedstock pricing and trade flows are reshaping regional competitiveness. Notably, epoxy resin pricing trends in Northeast Asia and significant year‑over‑year movements in bisphenol A (BPA) markets have implications for cost pass‑through, formulation choices, and regional sourcing strategies.

- Regulation and Standards: Regulatory compliance (e.g., REACH/SVHC) and evolving reliability standards for automotive and power semiconductors are elevating qualification timelines and influencing material selection.

What the Full Report Contains — Practical, Actionable Deliverables

- Quantitative market model (USD Million) spanning 2020–2032 with transparent assumptions, sensitivity tables and scenario outputs for planners to run their own “what‑if” cases.

- Granular demand drivers by application, material type and region, plus a matrix that links packaging performance requirements to resin formulations and expected margin differentials.

- Supply‑side mapping: capacity by producer, plant locations, throughput ramp schedules and techno‑economic notes on key polymer production processes.

- Raw material and logistics intelligence including historical price series, trade flow analysis, and procurement risk heatmaps to inform hedging and supplier diversification strategies.

- Regulatory and qualification playbooks detailing timelines, test regimes and compliance checkpoints for automotive, industrial and high‑reliability memory/logic packages.

- Competitive landscape dossiers and strategic profiles for the leading and fast‑growing players, paired with M&A screens and integration risk assessments.

- Executive action checklists and 90‑180‑365 day roadmaps for product, supply chain and commercial teams to operationalize strategic options in 2026.

Note: While this executive brief highlights market direction and strategic recommendations, the report deliberately withholds certain granular segmentation tables in order to preserve the commercial value of the full intelligence package. Detailed regional, application and material split tables are provided exclusively in the full report.

Competitive Landscape: Who Matters and Why

The competitive fabric is a mix of specialized resin chemists and vertically integrated conglomerates with polymer and electronics portfolios. Key players include established epoxy‑focused leaders, specialty chemical houses and company divisions embedded in larger industrial groups. Their strategic moves illustrate divergent approaches to growth:

- Scale and Capacity Leadership: Certain Japanese and East Asian leaders have invested heavily in capacity additions and new plant commissions to capture backend packaging demand for AI chips and automotive power modules. These investments are designed to secure supply relationships and support qualification cycles with major OEMs.

- Specialization and Performance Premiums: Companies with strengths in ultra‑low alpha, high‑Tg formulations, or thermally conductive grades are commanding premium pricing in high‑reliability segments. These suppliers are prioritizing R&D and close co‑engineering with customers to shorten time‑to‑qualification.

- Portfolio Diversification: Several global chemistry players are leveraging broader polymer and materials portfolios to bundle thermal interface, potting, and encapsulation solutions, thereby increasing share of wallet with electronics assemblers.

Representative recent developments underscore these trends: suppliers have announced thermally conductive EMC portfolios for EV power electronics, sizable capacity expansions in response to AI packaging demand, and joint‑venture manufacturing to strengthen regional backend supply chains. These moves validate the strategic thesis that scale plus specialized product depth will dominate premium segments.

Raw Materials, Trade Flows and Regulatory Headwinds

- Feedstock Price Volatility: The epoxy resin and BPA value chains experienced notable price swings in recent periods driven by upstream phenol and acetone cost movements and regional demand softness. These dynamics create margin pressure for formulators who cannot pass through costs quickly.

- Trade and Oversupply Risks: Changes in import flows and anti‑dumping measures have materially altered availability in certain regions, compressing arbitrage opportunities and forcing buyers to reconsider regional sourcing strategies.

- Compliance Imperatives: REACH and SVHC compliance for key encapsulant systems is non‑negotiable in many end markets; suppliers that can demonstrate compliance and provide transparency are shortening qualification cycles and winning business.

Action Playbook for 2026 — Decisions Executives Must Make

- Procurement Strategy: Secure multi‑tiered supply agreements for critical feedstocks, incorporate dynamic price clauses, and evaluate collaborative inventory models with strategic suppliers.

- Capex and Capacity Planning: Prioritize brownfield optimizations and modular expansions where lead times are short; evaluate JVs or tolling arrangements to access regional demand without full greenfield exposure.

- Product Development & Qualification: Align R&D roadmaps to thermal and reliability performance tiers demanded by EV and AI packaging. Invest in co‑engineering capabilities to compress customer qualification timelines.

- M&A & Partnerships: Pursue bolt‑on acquisitions for specialty grades or regional footholds; consider licensing or JV models to mitigate integration risks and accelerate market entry.

- Commercial Go‑to‑Market: Differentiate on systems thinking — bundle encapsulants with underfills and thermal interface materials, and offer qualification support to shorten the OEM ramp.

Why PW Consulting’s Report Is the Tactical Asset You Need in 2026

Our research translates macro growth (6.81% CAGR through the forecast period) and market concentration dynamics into specific, executable options — not just directional advice. The full report provides the calibrated market model, supplier scorecards, and scenario outputs necessary for investment committees, product leaders and procurement heads to prioritize action in 2026 with confidence.

For executives preparing capital budgets, sourcing strategies or M&A pipelines in 2026, this report acts as both a roadmap and a risk‑management tool. It combines deep chemistry knowledge, operational supply‑chain intelligence and deal‑level pragmatism to help organizations harvest the growth opportunity while insulating margins from raw material and regulatory shocks.

Next Steps

This brief is a curated preview designed to surface strategic implications and the most consequential signals in the chip encapsulation resin market. Access the full PW Consulting report for the complete market model, proprietary segmentation tables, supplier dossiers, and the tactical 90‑180‑365 day playbooks that will inform board‑level investment and procurement decisions in 2026.

For detailed analysis of this topic, please visit the official page:Chip Encapsulation Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com