GPS and GNSS Receivers in Aviation: Strategic Imperatives for 2026 — PW Consulting Market Brief

Executive summary

PW Consulting’s newest market study — GPS and GNSS Receivers in Aviation Market — synthesizes five years of historical data (2020–2025, base year 2025) and delivers a seven‑year forward view (2026–2032). The global market has expanded from an already substantive base in 2020 to an estimated USD 1,850.0 Million in 2025; under the central forecast (CAGR 6.75% for the 2026–2032 horizon) the market is projected to approach roughly USD 2.92 Billion by 2032. That combination of healthy mid‑single‑digit growth and a large installed base creates differentiated strategic opportunities across OEMs, avionics integrators, airlines, military programs, and systems integrators in 2026.

Gps And Gnss Receivers In Aviation Market

Why this report matters for 2026 enterprise decision‑making

- Investment timing: With consistent expansion and a clear upgrade cycle driven by NextGen/SESAR and regional mandates, procurement windows for line‑fit and retrofit are materializing now. The report identifies when demand waves will be strongest and the functional attributes that will command premium valuation.

- Product roadmap alignment: The shift to multi‑frequency, multi‑constellation receivers, integrated GNSS/INS units, and hardened PNT solutions is no longer marginal — these are product priorities that separate winners from laggards. Our analysis helps prioritize L5/DFMC capability, anti‑jamming/anti‑spoofing, and timing/holdover performance in next‑generation designs.

- Risk and resilience planning: Regulatory guidance and a rise in interference incidents require new operational procedures and equipment investments. The study maps plausible disruption scenarios and their P&L and safety implications for airframe manufacturers, operators, and defense programs.

- M&A and partnership scouting: The market dynamics favor both horizontal consolidation among component/OEM vendors and strategic partnerships linking avionics integrators with anti‑jam and INS specialists. Our competitive maps and valuation yardsticks help executives target the right assets and timing.

What’s in the report — practical content you can act on

The report is designed as an operational playbook for executives and program managers. Highlights include:

Gps And Gnss Receivers In Aviation Market

- Top‑down market sizing and scenario forecasts (2026–2032) built on bottom‑up adoption curves, validated against historical 2020–2025 performance.

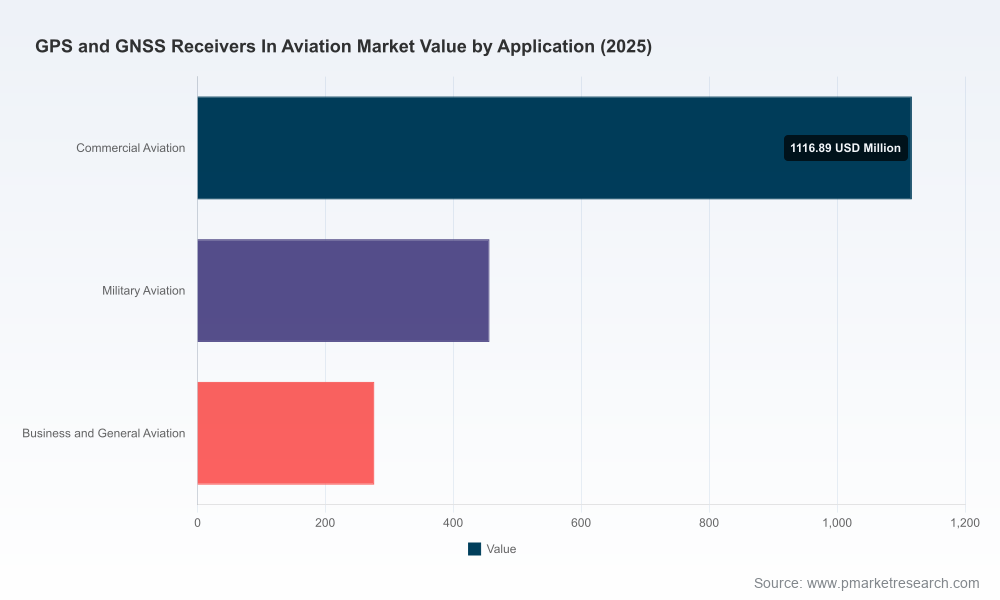

- Segmentation frameworks by technology, application and region with actionable buyer personas and procurement flows. (Note: detailed segment tables and region/application revenue splits are reserved for the full document.)

- Competitive benchmarking and supplier scorecards that assess certification readiness, product roadmaps, delivery lead times, and retrofit capabilities.

- Regulatory and standards tracker covering NextGen, SESAR, SBAS/LPV uptake, civil aviation authority mandates, and military assured‑PNT initiatives.

- Five pragmatic case studies — covering line‑fit avionics programs, major retrofit campaigns, military accreditation pathways, drone PNT integration and airport ground infrastructure — with financial sensitivity analysis and payback timelines.

- Procurement playbooks for airlines and MROs that translate technical specifications into contract clauses, acceptance tests and spares strategies.

Competitive landscape — who matters and why

The ecosystem mixes large aerospace primes, avionics specialists, and high‑precision GNSS vendors. In 2026 the competitive context is defined less by single‑product feature lists and more by integrated capability stacks: certified avionics, INS fusion, anti‑jam/spoof mitigation, and program delivery certainty.

Gps And Gnss Receivers In Aviation Market

- Garmin Ltd. (Schaffhausen, Switzerland) — Strong in certified avionics and retrofit solutions for general and business aviation; certification momentum (including recent EASA approvals) positions Garmin to capture aftermarket upgrades where operators prioritize cost‑efficient compliance and rapid fleet rollouts.

- Honeywell International Inc. (Charlotte, NC, USA) — Depth in integrated inertial/GNSS architectures and systems integration for commercial and military platforms; Honeywell’s strength is in high‑assurance avionics suites and program‑level supplier relationships.

- Collins Aerospace (RTX) (Cedar Rapids, IA, USA) — Focused on multi‑constellation receiver solutions and integrated navigation products that support MIL‑grade features (SAASM, M‑code readiness). Collins remains a go‑to for platform integrators requiring certification and sustainment.

- Thales Group (Paris, France) — Civil and defense capabilities with an emphasis on resilient PNT; recent TopStar Smart Receiver launch underscores a bet on compact anti‑jam modules for both manned platforms and unmanned systems.

- Trimble Inc. (Westminster, CO, USA) — An OEM supplier of high‑precision GNSS/INS modules, Trimble plays a crucial role for airframe manufacturers and avionics developers seeking embedded positioning accuracy.

- NovAtel (Hexagon AB) (Calgary, Canada) — Specialist in high‑precision receivers and ground reference/SBAS solutions that underpin integrity and safety‑critical aviation functions.

- L3Harris, Northrop Grumman, BAE Systems — Defense‑focused players delivering assured PNT solutions (including M‑code capable receivers and modernized EGI systems) that answer military program requirements for jam‑resistant navigation.

- Septentrio (Leuven, Belgium) — Known for anti‑jam and anti‑spoof receiver designs targeting demanding aerospace applications.

Recent industry developments in early 2026—from Northrop Grumman’s delivery of a modernized EGI system with M‑code to Thales’s compact anti‑jam TopStar release and Septentrio’s new multi‑frequency receiver — reflect an intensifying race to field resilient, certified PNT products for mixed civil and defense markets. Regulatory action (FAA’s updated interference guidance, CAAC dual‑frequency mandates, and EASA/IATA planning) is accelerating procurement decisions across the value chain.

Regulatory dynamics and operational risk

Regulation and real‑world interference trends are shaping demand and product specifications. Two contextual facts matter for 2026 planning:

- An uptick in reported GNSS signal loss events has driven air authorities to publish new guidance and mitigation frameworks — operators must now incorporate interference detection, reporting and non‑GNSS contingency procedures into operations and training.

- Air traffic modernization programs (NextGen/SESAR) and region‑specific mandates (including domestic dual‑frequency requirements) are creating firm technical standards (e.g., L5, DFMC) that influence certification roadmaps and retrofit prioritization.

For procurement teams and program managers, the implications are concrete: prioritize receivers and antennas that support multi‑frequency resilience, require deliverables that demonstrate anti‑jamming/anti‑spoofing capability, and structure contracts to accelerate certification deliverables and spares availability under interference scenarios.

Strategic playbook — five actions for executives in 2026

- Define differentiated product bets: Allocate R&D to integrated GNSS/INS and anti‑jam stacks rather than incremental receiver tweaks. Differentiate on verification under contested‑PNT scenarios and certification velocity.

- Lock in retrofit pipelines: Evaluate short‑term revenue from EASA/FAA‑driven retrofit programs versus longer‑term line‑fit opportunities; secure MRO partnerships and certification support early to capture aftermarket margins.

- Harden supply‑chain resilience: Component lead times and qualification cycles for high‑reliability GNSS modules are lengthening; diversify suppliers and secure long‑lead parts for avionics builds.

- Pursue targeted alliances: Combine avionics integrator scale with niche anti‑jam or INS expertise via JV or OEM supply agreements to speed time‑to‑market for certified solutions.

- Embed regulatory foresight: Use scenario planning tied to NextGen/SESAR timelines and regional mandates to prioritize certification testing, documentation and customer acceptance processes.

How PW Consulting’s report supports execution

The market study is built to be executable. It contains actionable modules — market sizing with sensitivity runs, supplier scorecards, product‑level roadmaps, certification risk matrices, and procurement templates — that companies can use in board‑level planning, R&D prioritization, commercial negotiations, and M&A diligence. To balance strategic transparency with commercial sensitivity, the public summary presents directional insights; the full report unlocks the detailed segment tables, regional and application splits, company scorecards and downloadable financial models that practitioners use to finalize 2026 budgets and go‑to‑market plans.

Next steps

For executives preparing 2026 budgets or mid‑cycle product reviews, the time to act is now. The market’s combination of steady growth (CAGR 6.75% through 2032), regulatory urgency, and accelerating innovation means that technical and commercial choices made this year will determine positioning for the next upgrade cycle. PW Consulting’s full report delivers the granular segmentation, vendor benchmarking, and scenario models needed to convert insight into decisive action.

Contact PW Consulting to access the full GPS and GNSS Receivers in Aviation Market report, including the downloadable datasets, supplier scorecards and procurement playbooks that underpin 2026 strategy.

For detailed analysis of this topic, please visit the official page:Gps And Gnss Receivers In Aviation Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com