Business Management Consulting Services Market — 2026 Strategic Preview

PW Consulting today releases a strategic preview summarizing the key implications from our forthcoming Business Management Consulting Service Market report (base year 2025). Built for executive decision-makers, corporate strategy teams, and advisory leaders, this overview synthesizes the macro trajectory, competitive dynamics, regulatory inflection points and practical levers that will shape capital allocation and go-to-market choices in 2026.

Business Management Consulting Service Market

Headline market trajectory: resilient expansion, selective disruption

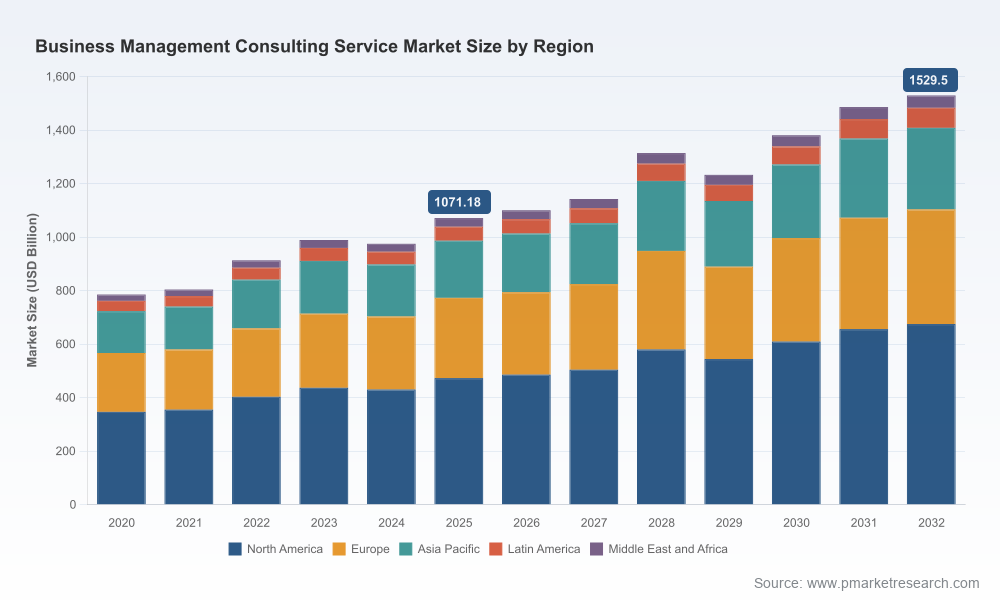

Our analysis finds the global business management consulting market continuing an upward trajectory, growing at a compound annual growth rate (CAGR) of 5.22% over the forecast window. Measured in USD Billion, the market expanded from the high hundreds in 2020 to just over one trillion by the mid‑2020s, with a 2025 base near USD 1.07 trillion and a projected 2026 size in excess of USD 1.10 trillion. The forecast to 2032 points to further expansion supported by digitization, advisory-led transformation and sustained demand for regulatory, financial and operational remediation services.

Business Management Consulting Service Market

That aggregate growth masks meaningful heterogeneity across client segments, service lines and geographies — an observation that underpins the core value of tailored strategy in 2026. The market is neither uniformly concentrated nor atomized: leading global firms hold a material but not dominating share of total revenue, leaving significant opportunity for specialized providers, regional champions and digitally enabled challengers.

Business Management Consulting Service Market

Why this report matters for 2026 decision cycles

- Investment prioritization: Boards and CFOs can use the report’s macro outlook and scenario stress-tests to align consulting budgets with three- to five-year transformation roadmaps, ensuring that spend drives measurable value rather than perpetuating advisory churn.

- M&A and partnership strategy: PE sponsors and strategic buyers will find the report’s transaction playbooks and integration risk matrices practical for targeting tuck-ins and capability buys that accelerate digital, AI and sector-specific advisory capabilities.

- Vendor selection and procurement: Procurement teams can leverage our vendor evaluation framework and implementation risk scoring to move beyond brand recognition toward outcome-based sourcing that links fees to client KPIs.

- Talent and operating model design: C-suite HR and practice leaders can apply the report’s workforce cost modelling and capacity planning tools to reconcile wage inflation with the need for specialised skills in AI, cloud, and regulatory advisory.

What the report contains — pragmatic, operational and decision-ready

Unlike typical market summaries, our report is structured for immediate adoption by client teams executing in 2026. Key deliverables include:

- Dynamic market sizing and multi-scenario forecasts (2026–2032) with revenue and growth assumptions explicitly documented for sensitivity testing.

- Actionable growth playbooks by service line — strategy, operations, financial advisory, HR advisory and technology-enabled management consulting — including go-to-market positioning, pricing archetypes and commercialization KPIs.

- Due diligence and M&A readiness checklists: value leak points, integration accelerators and templates for capturing post‑deal synergy.

- Regulatory impact assessments and compliance roadmaps tailored to cross-border advisory workflows, with pragmatic mitigation templates for data handling, cybersecurity and privacy obligations.

- Competitive intelligence dossiers and benchmarking toolkits that allow clients to map capabilities, partner ecosystems and fee models without revealing proprietary market shares in this preview.

- Deployment guides for AI-enabled advisory — governance models, vendor selection criteria, pilot-to-scale templates and change management playbooks.

To preserve the strategic value of our methodology and commercial datasets, core segmentation tables, granular regional and application breakdowns, and company market share matrices are reserved for subscribers of the full report.

Competitive landscape: leaders, differentiators and the rise of platform plays

The competitive topology of the consulting market is shaped by three overlapping dynamics: the persistence of elite strategy firms that command premium fees for top‑tier corporate advisory; Big Four firms and large systems integrators that leverage scale across audit, technology and transformation; and a second tier of specialized boutiques and product-led consultancies that compete on domain depth and execution. The market exhibits moderate concentration among the top firms, leaving room for specialist players to capture niche premiums.

Key observations on incumbent positioning:

- MBB (McKinsey, BCG, Bain): These firms continue to lead on C-suite strategy mandates and top‑down transformation agendas. Their ability to combine strategic advisory with private equity advisory and selective productization keeps them central to high‑value deals.

- Deloitte, PwC, EY, KPMG: The Big Four increasingly blur advisory, audit and tax value chains into enterprise-wide transformation offerings. Their breadth is a competitive advantage in cross-functional mandates but exposes them to integration complexity and regulatory scrutiny.

- Accenture, IBM Consulting: These firms are accelerating the platformization of consulting — bundling cloud, AI, and managed services with advisory outcomes. Recent strong bookings and revenue announcements underscore demand for integrated technology-enabled transformations.

- Specialists (Oliver Wyman, boutiques): Firms focused on financial services, risk, and sector-specific advisory continue to secure assignments that require deep domain expertise and rapid regulatory adaptation.

Recent market signals reinforce this dynamic. Independent rankings released in early 2026 identified traditional leaders across prestige and client satisfaction metrics, while product launches from major firms are signaling a shift to subscription and platform-based commercial models. At the same time, leading integrators are reporting elevated bookings and revenue growth — evidence that clients are prioritizing bundled technology and advisory solutions.

Regulatory and talent headwinds: constraints that will define winners and losers

Two structural constraints dominate the operational risk profile for consulting firms and their clients in 2026:

- Regulatory complexity: The rapid proliferation of data privacy and security rules — including multiple US state comprehensive privacy laws and tightened financial-sector cybersecurity requirements — compels firms to formalize cross-border data governance, client‑specific handling protocols and evidence trails for advisory work products. Supplementary rules on bulk data transactions and enhanced record‑keeping further increase compliance costs and operational friction.

- Labor and wage inflation: Talent scarcity in AI, digital engineering and transformation management continues to pressure margins. Firms face a choice between raising bill rates, absorbing margin compression, or investing in automation and productization to reduce reliance on high-cost bench resources.

For corporate buyers, these headwinds mean prioritizing partners who can demonstrate robust compliance capabilities and outcome‑aligned staffing models. For sellers, success in 2026 will require rethinking talent deployment, augmenting human expertise with scalable assets, and crystallizing value-based pricing.

Strategic implications and recommended actions for 2026

- Shift from input-based to outcome-based contracting: Move away from day-rate models for transformation programs and structure incentives around measurable client outcomes. Institute phased proof-of-value gates to manage risk.

- Invest in compliance-as-a-service: For firms serving regulated sectors, productize data governance and cybersecurity controls as client‑facing deliverables to reduce friction during procurement and accelerate scaled engagements.

- Productize repeatable assets: Capture IP around common transformation patterns and redeploy through subscription or managed-service vehicles to protect margin as labor costs rise.

- Double down on sector depth: Where regulatory complexity is high (financial services, health, critical infrastructure), prioritize deep domain teams and build rapid regulatory response playbooks that shorten time to trusted advisor status.

- Align M&A to capability gaps: Use targeted tuck-ins to acquire scarce skills — e.g., AI model risk management, cloud-native engineering, or healthcare outcomes analytics — rather than broad revenue plays that dilute focus.

How PW Consulting supports executive action in 2026

Our full Business Management Consulting Service Market report combines the macro numbers, scenario-based forecasts and a proprietary go-to-market playbook with hands-on templates and advisory support. PW Consulting offers a staged engagement model that pairs the report’s diagnostic outputs with implementation programs — from vendor selection sprints and pricing model redesigns to integration of AI governance frameworks and M&A diligence support.

For leaders preparing 2026 budgets, selecting advisory partners, or evaluating M&A targets, the full report provides the empirical foundation and execution playbooks needed to convert market insight into measurable value. Detailed segmentation tables, company market shares and the complete benchmarking dataset are available exclusively in the subscriber edition.

To access the comprehensive dataset and a tailored briefing with PW Consulting’s industry leads, visit our website or contact our research team for a confidential presentation.

For detailed analysis of this topic, please visit the official page:Business Management Consulting Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com