Why Hiring a Digital Marketing Expert Kerala is Important for Business Success

Other |

2026-05-27 05:43:57

As organizations accelerate small-footprint automation across electronics, life sciences and precision manufacturing, desktop industrial robots have emerged as a strategically indispensable asset. PW Consulting’s new Desktop Industrial Robot Market report synthesizes five years of historical performance (2020–2025) and an actionable seven‑year forecast (2026–2032), revealing a compound annual growth rate (CAGR) of 13.52% and a market trajectory that moves from a mid‑single‑to‑high‑hundreds million-dollar industry in the mid‑2020s toward a near‑two‑billion‑dollar opportunity by 2032. For executives finalizing investment, product and partnership decisions in 2026, the report supplies the market context and operational playbooks necessary to convert this growth into competitive advantage.

Desktop Industrial Robot Market

Adoption inflection: The desktop segment has matured beyond pilot programs into scalable benchtop production. Increasing labor costs in precision assembly and electronics, coupled with Industry 4.0 initiatives, are driving executives to prioritize compact automation investments in 2026 as a means to protect margins and accelerate small‑lot, high‑mix production.

Desktop Industrial Robot Market

Technology convergence: Advances in compact 6‑DoF manipulators, SCARA and Cartesian architectures, plus an emerging generation of collaborative desktop arms with safety‑rated force monitoring, enable integrators to build safe, dense production cells without the footprint penalty of traditional industrial robots.

Desktop Industrial Robot Market

Regulatory clarity: Existing standards (ISO 10218 family and ISO/TS 15066) continue to provide a predictable safety framework for collaborative desktop deployments, reducing compliance risk for buyers and accelerating procurement cycles.

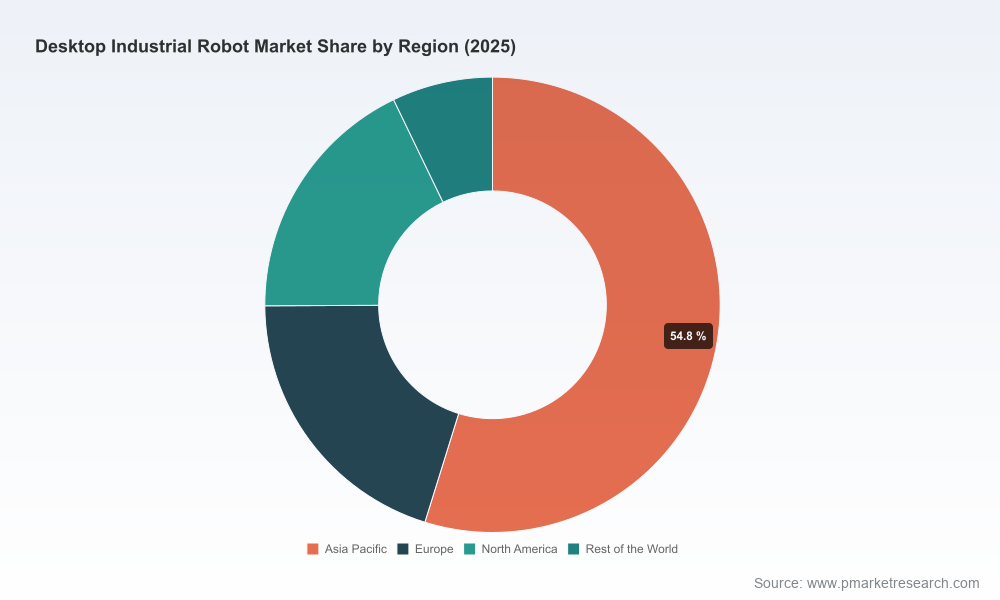

PW Consulting’s topline numbers underscore a robust expansion phase. The market has more than doubled in value over the 2020–2025 historical window and is forecast to grow at a healthy double‑digit pace through 2032. This growth is not monolithic: it is driven by the convergence of demand from electronics and semiconductor assembly, healthcare/life sciences benchtop automation, and precision engineering use cases that require sub‑millimeter repeatability. While the report documents granular regional and application splits within the dataset, this briefing intentionally omits segmental breakouts — we reserve those fine‑grained maps for the full report and data package to ensure a high‑value audience conversion to the study’s access portal.

Importantly, the market shows a moderate concentration profile: three of the largest players control a meaningful share of accessible revenue, and a top‑five cohort amplifies scale advantages in distribution, IP and channel support. This concentration creates both barriers and opportunities — incumbents defend through integrated solutions and ecosystem partnerships, while nimble challengers capture share with differentiated pricing, speed of integration and localized services.

End‑use playbooks: Practical deployment templates for electronics assembly, medical device benchtop manufacturing and laboratory automation — detailing cell layouts, cycle‑time budgeting, tooling and integration checkpoints.

Procurement and TCO modeling: A step‑by‑step methodology to assess capital and operating costs, developer and integrator labor, spare parts provisioning and expected payback periods across representative use cases.

Integration checklists: Interfacing standards, payload and precision matching guidelines, safety barrier vs. collaborative cell decision trees, and recommended testing regimes to minimize production disruption during ramp.

Supply chain risk matrix: Materials exposure (steel and precision aluminum alloys), supplier concentration maps and mitigation actions for procurement managers to secure continuity amid metals market volatility.

Commercial motion recommendations: Go‑to‑market approaches for OEMs, integrators and component suppliers, including pricing levers, channel incentives and after‑sales service models that sustain recurring revenue.

Proprietary forecast and scenario engines: Base, upside and downside pathways to 2032 that allow CFOs to stress‑test budgets under alternative adoption and macroeconomic assumptions.

The desktop robot ecosystem is diverse, ranging from heritage Japanese automation firms to agile North American and Chinese challengers. Our competitive review assesses positioning across product breadth, precision, integrator readiness and go‑to‑market execution.

Janome (Japan) — A stalwart in cartesian desktop systems, Janome’s JR3000 series demonstrates the strategic value of focused, application‑specific platforms for precision dispensing, screwing and low‑volume assembly. Their engineering depth and reputation in small‑footprint industrial tasks make them a first call for customers needing deterministic performance with minimal integration overhead. (https://www.janomeie.com)

Dobot / Shenzhen Yuejiang Technology (China) — Aggressive on price‑performance and rapid product iteration, Dobot has positioned desktop collaborative arms and four‑axis benchtop cells for fast integration. Their presence at global shows and a growing product family make them a notable contender for OEMs seeking cost‑efficient automation at scale. (https://www.dobot-robots.com)

DENSO Robotics (DENSO WAVE, Japan) — With a proven pedigree in compact SCARA and assembly robots, DENSO blends high reliability with strong support networks, which is critical for mission‑critical benchtop applications in automotive electronics and consumer devices. (https://www.densorobotics.com)

Mecademic (Montreal, Canada) — Offers some of the smallest, most precise 6‑axis industrial robots engineered specifically for desktop and benchtop use. Their precision advantage makes them a natural choice in metrology, micro‑assembly and laboratory automation contexts. (https://mecademic.com)

TOYO Robotics, TM Robotics, Nitto Seiko, Elephant Robotics and USABotics — Each brings regional strengths, distribution networks and niche product specializations (electric actuators, compact SCARA options, and collaborative 6‑DoF arms). Collectively, they comprise the middle tier of the market that competes on service, responsiveness and localized application engineering.

Recent market activity validates these dynamics: leading platform vendors announced higher‑speed collaborative arms and showcased desktop portfolios at 2025 trade events, while multi‑vendor participation at major industry shows reinforced the shift from lab demonstrations to production‑ready systems. These product developments and exhibitions are covered in the report with comparative feature matrices and integration timelines to inform 2026 sourcing strategies.

Raw materials: The industry remains sensitive to global metals markets. Structural frames and arms primarily use steel and precision aluminum alloys; procurement teams must incorporate metals price and lead‑time assumptions into TCO models.

Regulatory and safety compliance: For collaborative desktop deployments, adherence to ISO standards is non‑negotiable. Buyers should prioritize vendors that embed compliance testing and offer documented safety integration support.

Talent and integration: The supply of skilled integrators and application engineers is a gating factor. Companies that pair product sales with training, remote diagnostics and local service networks will realize faster time to value.

Prioritize modular, interoperable platforms: Select robotic platforms that support rapid tool‑change, open control APIs and standardized communication stacks to protect against future technology lock‑in.

Invest in pilot‑to‑scale playbooks: Convert successful benchtop pilots into repeatable production cells by documenting fixtures, cycle times and failure modes during pilot phase to accelerate scale‑out.

Embed service and spare strategy at procurement: Negotiate parts availability, remote support SLAs and uptime guarantees as part of the procurement contract to reduce operational risk.

Use our scenario engine for capex planning: Run sensitivity analyses on adoption rates and price erosion to align 2026 capex with probable revenue timelines and payback thresholds.

Explore ecosystem partnerships: Consider co‑development or reseller agreements with established platform vendors to accelerate market entry while leveraging proven hardware ecosystems.

Executives told us they needed three things to move decisively in 2026: credible forecasts, operational playbooks and competitor benchmarking that maps to procurement and product planning. This report delivers all three. It combines a transparent forecasting methodology and scenario modeling with hands‑on deployment templates and a comparative vendor matrix that ranks suppliers by precision, integration readiness and total cost of ownership.

To preserve the strategic value of the dataset for subscribers and clients, this briefing omits the granular regional, type and application monetary breakdowns — the full report includes complete segmentation tables, downloadable spreadsheets and an interactive model that unlocks those insights for decision-makers ready to act.

If you are planning automation investments in 2026, request PW Consulting’s full Desktop Industrial Robot Market report to access the detailed segmentation, vendor scorecards and the scenario engine.

For bespoke advisory or a rapid diagnostic workshop to align your 2026 automation roadmap with capital and operational constraints, our senior consultants are available to help translate the report’s findings into an executable plan.

PW Consulting’s market research equips leaders to convert the desktop robotics growth wave into measurable margin improvement and manufacturing agility. The coming 18 months will determine who captures the productivity gains of compact automation — those who pair data‑driven strategy with disciplined execution will define the next generation of efficient, high‑mix manufacturing.

For detailed analysis of this topic, please visit the official page:Desktop Industrial Robot Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com