Call Girls in Sharjah +971523073738

Other |

2026-07-01 12:51:19

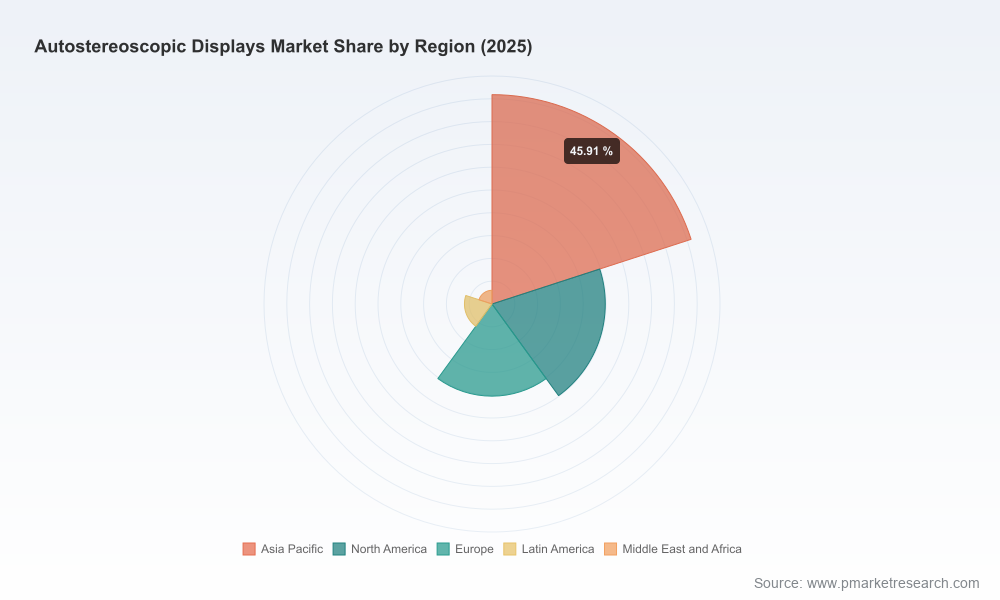

PW Consulting’s newest market brief on Autostereoscopic Displays synthesizes technology, commercial and policy dynamics into a pragmatic playbook for corporate leaders planning 2026 investments. Using a 2025 base and an empirically calibrated forecast running through 2032, our model projects the global autostereoscopic market to expand at a compound annual growth rate (CAGR) of 17.88%. To frame scale: the market moved from roughly USD 845 million in 2020 to about USD 1.82 billion in 2025 and is forecast to exceed USD 5.7 billion by 2032. This article is a strategic “teaser” — designed to surface the high-value implications and near-term actions while reserving the report’s proprietary segment-level tables and financial models for the full study available on our website.

Autostereoscopic Displays Market

Technology maturation: Optical and software advances — switchable light-field modules, high-precision lenticular arrays, eye- and head-tracking systems, and nascent metalens concepts — are converging into commercially viable form factors across signage, professional visualization and select consumer pockets. These advances materially compress time-to-value for pilots and commercial rollouts.

Autostereoscopic Displays Market

Commercialization momentum: 2025–mid‑2026 saw a notable tranche of product introductions and demonstrations from both specialists and large OEMs, signalling readiness to transition from proofs-of-concept to scaled deployments in verticals such as healthcare visualization, digital-out-of-home (DOOH) advertising, and automotive HMI.

Autostereoscopic Displays Market

Policy and supply-chain volatility: Trade measures enacted since 2025 (including reciprocal tariffs and profile‑based duties) and concentrated sourcing for key optical and AMOLED inputs significantly affect supplier selection, landed cost and time-to-market. These are not cyclical headwinds — they are structural inputs to any supply strategy in 2026.

The reported CAGR and the market’s multi‑year trajectory tell a clear strategic story: investment windows exist for participants who can align product readiness, supply resilience and go-to-market velocity. A near‑threefold expansion from the 2025 base to the 2032 horizon implies not only demand growth but also meaningful platform evolution — richer content ecosystems, tighter integrations with AI-driven spatial software, and new business models around managed signage and imaging-as-a-service.

Importantly, growth is not uniform: product and channel dynamics differ by use case, commercial cadence and procurement cycles. That heterogeneity is why the market is attractive for focused entrants and incumbent OEMs alike: targeted differentiation (software and content tooling, service contracts, or domain-specific optics) often yields outsized returns versus undifferentiated scale plays.

Specialist system integrators and optics innovators (e.g., Magnetic 3D, Alioscopy, Dimenco) continue to control high-end, application‑specific deployments by combining engineered optics with systems integration capabilities. Recent product launches and multiview displays exemplify this approach.

Platform and chipset players (e.g., Leia) are advancing switchable light‑field and spatial software platforms that can be licensed across device makers — an asset-light route to scale but one that requires robust IP and developer ecosystems.

Large OEMs (e.g., Samsung, Philips, LG) and visualization specialists (e.g., Barco) are selectively commercializing autostereoscopic signage and medical monitors, using their channel reach to accelerate deployments where integration with existing systems matters most.

Emerging entrants and regional manufacturers are leveraging component supply and local assemblies to undercut incumbents on cost and lead-time, especially in markets where localized service is a procurement preference.

Our concentration analysis indicates a market where top-tier vendors hold meaningful share but where competitive fragmentation and vertical specialization leave room for new value propositions. For detailed vendor scorecards, IP posture assessments and scenario permutations, the full report contains the underlying evidence base and our proprietary vendor matrix.

New product introductions in 2025–2026 highlight pragmatic shifts: smaller multiview signage units and mid-sized professional monitors now include integrated optics, embedded compute and eye-tracking — enabling faster pilot-to-deployment cycles and lower integration costs.

Trade and component exposure (tariffs, raw material sourcing) materially increase the economics of nearshoring, contract-manufacturing partnerships and multi-sourcing strategies. Firms that lock in alternative optical-film suppliers or negotiate long-term component contracts will preserve margin flexibility.

Healthcare and enterprise visualization are demonstrating high willingness-to-pay for domain‑validated solutions (regulatory robustness, integration with imaging workflows), making these verticals prime targets for premium product strategies.

Tariff uncertainty and policy-driven duties can change landed cost profiles rapidly. Scenario-based procurement contracts and hedged sourcing are no longer optional for OEMs and integrators.

Component concentration for optical films and specialty backplanes creates single‑point-of-failure risks; contract terms should include substitution clauses and penalty-sharing mechanisms for supply disruption.

Labor-cost differentials and regional production efficiencies favour mixed manufacturing footprints. Near-term capital allocation should evaluate trade-offs between absolute cost, time-to-market and political risk.

First 90 days: Validate customer economics through two rapid pilots (one in a high‑value vertical such as healthcare or automotive, one in DOOH). Simultaneously, map direct supplier exposure and secure contingent supply options for optical films and light engines.

Next 180 days: Convert successful pilots into commercial agreements. Negotiate multi‑year frameworks with strategic suppliers that include price collars and capacity commitments. Begin modularizing product stacks to separate optics, electronics and software for faster iteration.

360 days: Scale go‑to‑market via a partner network and roll out certified integrations for the top two verticals identified in pilot validation. Execute on IP and software investments that increase switching costs for customers (developer tools, content pipelines, analytics).

Our report is structured to move executives from insight to action. It includes:

Demand and revenue scenarios calibrated to policy shocks and supply disruptions, with sensitivity analyses aligned to the 2026 procurement calendar.

Vendor diagnostic templates that benchmark technology, go-to-market reach, margin structure and integration risk (ideal for M&A screening or strategic partnerships).

Manufacturing and sourcing playbooks that quantify trade-offs between centralized low-cost production and localized assembly strategies under different tariff scenarios.

Commercialization blueprints for verticals where autostereoscopic propositions translate into measurable business outcomes (e.g., reduced procedure time in healthcare, engagement uplift in DOOH).

Because the most valuable decisions hinge on fine-grained segmentation and pricing dynamics, the full report contains proprietary tables and model access (including our region/type/application breakdowns and a customizable financial model). We intentionally withhold those segment-level figures in this public briefing to preserve the integrity of our data license and to direct stakeholders to the authenticated report package.

Prioritize investments that enable modular product upgrades (optics, compute, software) rather than single-release hardware bets.

Treat supply-chain diversification and tariff mitigation as capital investments with defined ROI windows; contracting strategy will materially affect gross margins in 2026.

For M&A, target companies that combine product IP with domain-specific channel access — the combination shortens commercial ramp and raises barriers to replication.

For executives preparing budgets and strategic plans in 2026, our analysis delivers both the directional market thesis (large, high-growth market underpinned by a 17.88% CAGR) and a concrete operational agenda. If you require drill-down access to the scenario models, vendor scorecards or the full segmentation and revenue tables, PW Consulting’s full Autostereoscopic Displays Market report provides those deliverables along with tailored advisory engagements to support implementation.

Contact PW Consulting to schedule a briefing or to request the complete report package and the bespoke financial model that aligns with your strategic priorities.

For detailed analysis of this topic, please visit the official page:Autostereoscopic Displays Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com