Contact Lenses Market: Insights, Key Players, and Growth Analysis

Other |

2026-05-27 09:28:19

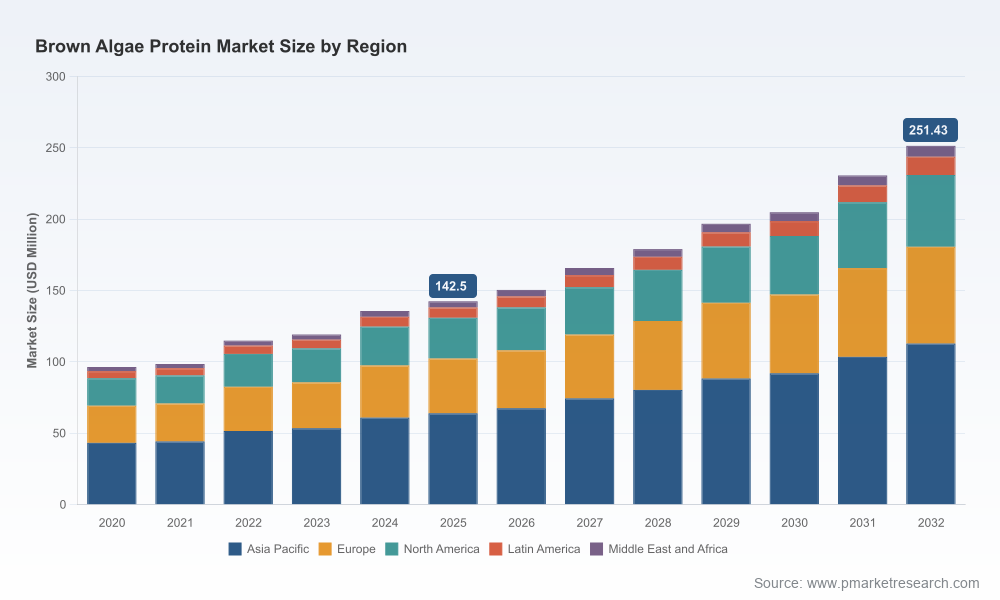

PW Consulting today releases an executive briefing summarizing the strategic value of our full Brown Algae Protein Market report for executives planning moves in 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the analysis quantifies a market that rose from under USD 100 million at the start of the decade to an estimated USD 142.5 million in 2025, and which PW projects will expand to roughly USD 251.4 million by 2032 — reflecting a compound annual growth rate of 8.45% over the forecast period. This briefing is designed as a decision-oriented preview: it demonstrates our evidence-based judgement and practical recommendations while directing commercial readers to the full report for the granular segment economics and proprietary tables that underpin our conclusions.

Brown Algae Protein Market

Timing and scale: Brown algae protein is transitioning from niche to mainstream applications as extraction technology, regulatory clarity, and ingredient formulation capabilities converge. Our market sizing shows accelerating commercialisation momentum that makes 2026 a critical inflection year for capital allocation and strategic partnerships.

Brown Algae Protein Market

Risk-controlled entry: The market’s structure — modest concentration at the top and a broad base of specialist suppliers — creates opportunities for both incumbent ingredient companies and new entrants to secure differentiated positions without confronting immediate monopolistic pricing pressures.

Brown Algae Protein Market

Portfolio optimisation: CPG, nutraceutical, and feed companies can use the report’s frameworks to evaluate where brown algae protein becomes a source of margin uplift, nutritional differentiation, or sustainability storytelling versus where it is still a cost center requiring process engineering.

Market sizing and methodology: A complete reconciliation of historical demand (2020–2025) and a transparent forecast model for 2026–2032, including scenario outputs and sensitivity to raw-material supply and extraction yields.

Supply-chain maps and cost curves: Comparative economics for feedstock sourcing (wild-harvests, cultivated kelp, and opportunistic Sargassum harvests), unit-cost breakouts for main extraction routes, and a supplier-positioning matrix that highlights where margin capture is feasible.

Extraction-technology assessment: Side-by-side evaluation of protein isolates, concentrates, and hydrolyzates — covering yield ranges, capital intensity, downstream refining needs, and typical quality attributes relevant to food, feed, and nutraceutical applications.

Regulatory and sustainability playbook: Practical checklists for regional food-safety approvals, claims substantiation, and third-party certification. Also included are operational templates for sustainable harvesting partnerships and traceability systems aligned with fisherfolk and coastal communities.

Commercial go-to-market tools: Product-positioning scorecards, pricing tier frameworks, co-manufacturing contracting templates, and retailer-spec compliance matrices designed to limit time-to-shelf for food applications.

M&A and partnership intelligence: A transaction playbook and valuation comparators that highlight where consolidation creates immediate scale benefits, and where joint ventures with upstream harvesters reduce feedstock volatility.

Scenario analyses and playbooks: Base, upside, and downside scenarios that model feedstock shocks, extraction yield improvements, and demand shifts across the main application clusters — together with recommended tactical responses for each scenario.

Brown seaweed species such as Laminaria, Sargassum and Ascophyllum nodosum remain the primary upstream feedstock for protein extraction. The sector also faces new low-cost biomass opportunities — for example, large seasonal accumulations of Sargassum which recent third-party studies estimate in the order of tens of millions of tonnes globally — that can materially alter feedstock cost curves if properly harvestable and processed. That said, sustainable harvesting practices, community partnerships, and regulated aquaculture expansion will be essential to protect coastal ecosystems and ensure consistent quality for food-grade protein ingredients.

The ecosystem combines global ingredient multinationals, specialised extractors, regional processors and vertically integrated harvesters. Our competitive benchmark highlights the strategic positions of core players:

Algaia S.A. (France) — specialist extractor providing functional ingredients and bioactives, notable for nearshore sourcing and partnerships that support environmental compliance and supply continuity.

Acadian Seaplants (Canada) — established harvester/processor with depth in brown-seaweed-derived meals and proteins for animal nutrition and agronomy markets, offering scale in North Atlantic feedstock supply chains.

CP Kelco (Tate & Lyle) and Cargill — legacy hydrocolloid and ingredient players leveraging larger commercial footprints to integrate alginate-based fractions and associated protein products into mainstream food and industrial formulations.

Gelymar (Chile), Qingdao Gather Great Ocean Algae Group and Qingdao Brightmoon (China) — regionally dominant processors with access to South American and East Asian biomass pools, often competing on cost and volume for commodity-grade supplies.

Smaller specialists such as Ocean Harvest Technology, Mara Seaweed and Seagreens — focus on sustainable sourcing, premium food-grade powders and niche functional applications that target higher-margin segments.

Market concentration remains moderate: the top three companies account for under one-third of the market while the top five account for just under two-fifths. This fragmentation creates strategic options for scale consolidation, selective partnership formation and niche premiumisation.

Lock down feedstock diversity: Establish dual-sourcing agreements (wild harvest + cultivated kelp) and pilot Sargassum-based processing where legal and technically feasible to build resilience against local supply shocks.

Invest selectively in extraction R&D: Prioritise pilot-capex for technologies that improve protein yield and functionality (e.g., enzymatic fractionation and low-temperature refinement) to open up higher-value food and nutraceutical uses.

Deploy staged commercial pilots: Use co-manufacturing or toll-extraction to test formulations, sensory profiles and shelf-life with anchor customers before committing to greenfield capacity.

Pursue strategic M&A or JVs for scale: For companies seeking rapid vertical integration, target processors with reliable biomass access or extraction IP rather than only end-product brands.

Lead with sustainability credibility: Invest in traceability, community partnerships, and certification as a means to command premium pricing and reduce regulatory friction in developed markets.

Build regulatory-first commercialization roadmaps: Early engagement with food-safety authorities and proactive toxico-nutritional dossiers will shorten time-to-market for new formulations in 2026–2027.

Price and product tiering: Create distinct SKUs for commodity protein fractions and high-value isolates/hydrolyzates to capture both volume and margin as demand broadens.

Ingredient incumbents: Accelerate pilot extraction capacity and partner with coastal harvesters to secure feedstock. Focus first on lower-barrier applications (e.g., some feed and industrial uses) to validate economics before moving into food-grade isolates.

CPG and nutraceutical brands: Start with small-batch co-formulations and consumer sensory tests, leverage sustainability narratives, and work on technical dossiers to support any structure-function claims.

Feed and aquaculture operators: Target species-specific formulations that improve FCR or animal health, while validating scale supply via long-term harvesting agreements or cultivation contracts.

Private equity and strategic investors: Use staged investment with operational KPIs tied to extraction yield improvements, product qualification wins and binding offtake contracts.

PW Consulting combines proprietary market models, in-field supply-chain mapping, extraction-cost benchmarking and go-to-market playbooks tailored to ingredient, brand and investor clients. Our full report delivers the detailed tables, regional splits, application-level economics and supplier scorecards required to execute on the strategies summarized here. For corporate strategists and deal teams preparing allocations in 2026, the report provides the granular intelligence and operational templates needed to move from hypothesis to execution within 90–180 days.

To access the complete Brown Algae Protein Market report — including the segmented demand tables, supplier scorecards and downloadable financial models referenced in this briefing — please visit the PW Consulting website or contact our industry team. The full report contains the data-level intelligence that will materially shorten diligence timelines and reduce execution risk for brown algae protein initiatives in 2026.

For detailed analysis of this topic, please visit the official page:Brown Algae Protein Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com