Medical Silicone Vasculature Models Market: Strategic Briefing for 2026 Decision-Makers

Executive snapshot

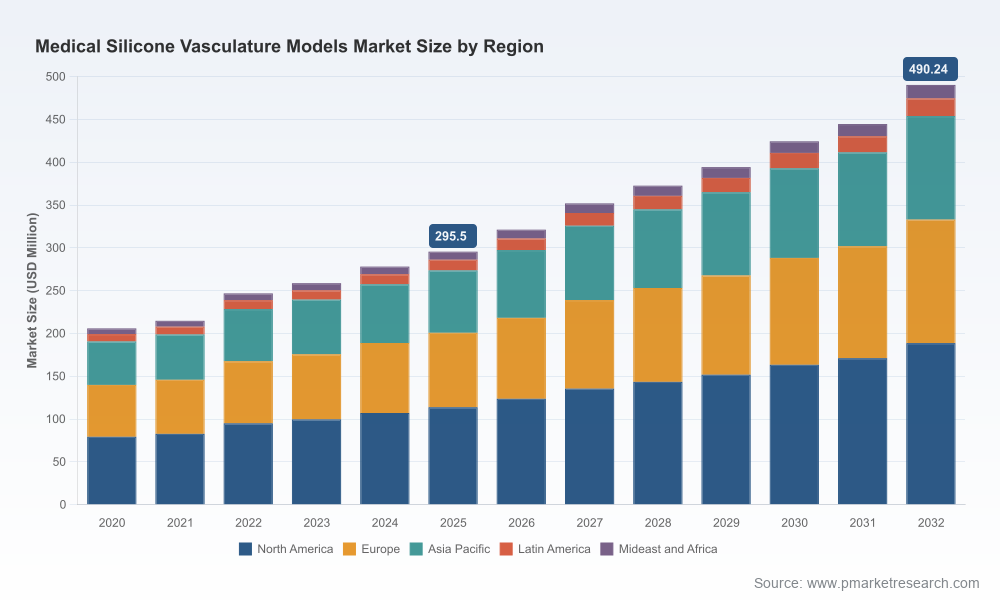

PW Consulting’s new market research on Medical Silicone Vasculature Models provides a forward-looking playbook for executives making strategic choices in 2026. Built on a consistent historical series (2020–2025) with 2025 as the base year and a seven-year forecast horizon (2026–2032), the study quantifies a resilient growth trajectory driven by advances in 3D printing, patient-specific workflows, and expanded use across training, device R&D and pre-surgical planning. The market grew from roughly USD 206 million in 2020 to about USD 296 million in 2025, and — at a compound annual growth rate of 7.51% — is projected to approach the half-billion-dollar mark by 2032.

Medical Silicone Vasculature Models Market

Why this report matters for 2026 strategy

For leadership teams evaluating product investments, partnerships, manufacturing footprints, or M&A in 2026, the medical silicone vasculature models market is no longer a niche, ad-hoc supplier segment. It has matured into a strategic node that links device development, regulatory testing, training ecosystems and hospital procedural planning. Key inflection points for near-term decisions include:

Medical Silicone Vasculature Models Market

- Regulatory alignment: Guidance and testing expectations (including ISO/ASTM standards and agency guidance on simulated-use testing) are raising the bar for anatomical fidelity and tortuosity in mock-vessel testing. Buyers increasingly require models that can be certified against recognized protocols.

- Technology convergence: Additive manufacturing, soft-tissue material science and imaging-to-model workflows are converging. Manufacturers who can deliver repeatable, patient-specific silicone geometries at scale have a disproportionate commercial upside.

- Cost and supply resilience: Medical-grade liquid silicone rubber (LSR) and related supply inputs are a persistent cost and continuity consideration. Firms that lock favorable material sourcing or vertically integrate critical processes gain tactical pricing and margin advantages.

- Customer segmentation: Use cases have evolved beyond classroom training—device R&D, bench validation and pre-operative planning are core demand engines. Each use case imposes different quality, traceability and customization requirements.

What’s in the PW Consulting report (practical deliverables)

The report is designed to be execution-focused for corporate strategy, commercial teams and product leaders. Highlights include:

Medical Silicone Vasculature Models Market

- Market sizing and a transparent forecasting model that supports scenario pulls for different 2026 investment choices.

- Demand-driver analysis that connects hospital procedure volumes, device launch pipelines and simulation training adoption to addressable-market trajectories.

- Technology and materials map that ranks manufacturing approaches (3D printing, molding, hybrid composites), process bottlenecks and maturity timelines.

- Regulatory and testing matrix, cross-referencing ISO/ASTM standards and agency guidance to typical product specifications used in simulated-use and bench testing.

- Commercial playbooks: go-to-market strategies by buyer archetype (device OEMs, academic simulation centers, hospitals), pricing heuristics and service bundling options.

- Competitive landscape with profiles, capability comparisons and recent activity timelines to support target screening and partnership prioritization.

- Scenario-based risk assessments (supply shock, accelerated adoption, stricter regulation) and decision-sensitivity analyses that translate to board-level strategic options.

Competitive landscape — who matters and why

The market is characterized by a mix of highly specialized small-to-mid sized engineering firms, university spin-outs and established simulation companies. Market concentration is moderate: the largest three players do not command a dominant share, and the top five together hold less than half of market revenues—creating opportunities for consolidation and differentiated service plays.

Notable players profiled in the report include:

- United Biologics (Irvine, CA): Known for proprietary silicone formulations tailored for endovascular simulation. Their material science focus supports high-fidelity hemodynamic behavior and repeatable device interaction testing.

- BDC Laboratories (Wheat Ridge, CO): Offers engineered compliant mock vessels for cardiovascular device testing and hands-on simulation. Active trade-show engagement signals a strong commercial motion into OEM and educational channels.

- Ningbo Trando 3D Medical Technology (Ningbo, China): Specializes in 3D-printed silicone vascular models at scale for neuro, coronary and peripheral interventions—their cost-competitive manufacturing footprint complements global demand.

- Elastrat (Geneva, Switzerland): Delivers transparent soft and rigid silicone phantoms with a focus on research-grade reproducibility and optical clarity for imaging applications.

- Mentice (Gothenburg, Sweden): Combines patient-specific silicone models with integrated simulation platforms, positioning at the intersection of software-enabled training and physical model supply.

- Preclinic Medtech (Shanghai) and MedScan3D (Galway): Both emphasize high-simulation, patient-specific 3D silicone models for training and device testing, with different strengths in regional manufacturing and client integrations.

- Swiss Vascular (Zurich/ETH spin-off): A new entrant launched in mid-2025 with anatomically exact cerebral vessel models; their academic lineage underscores strong R&D capabilities for neurovascular applications.

Recent competitive signals to watch in 2026

- New product launches and academic spin-outs are accelerating domain-specific offerings (for example, anatomically precise cerebral phantoms introduced in 2025).

- Exhibitions and trade-show activity in early 2026 indicate intensifying OEM engagement and buyer outreach by specialist labs.

- Partnerships between simulation platform providers and silicone model manufacturers are emerging as a route to capture higher lifetime value per customer.

Strategic imperatives for leadership in 2026

Based on our quantitative baseline (7.51% CAGR to 2032) and qualitative market scans, PW Consulting recommends five near-term priorities for organizations seeking to lead or defend position in this market:

- Invest in modular manufacturing capability: Develop a hybrid capacity across molding and additive manufacturing to serve both volume and bespoke patient-specific demand efficiently.

- Secure materials resilience: Negotiate multi-year LSR supply contracts, qualify alternate material sources and test recycled/alternative silicones where regulations permit to protect margins during supply volatility.

- Design for regulatory reproducibility: Embed ISO/ASTM test protocols and FDA-referenced tortuosity criteria into product development lifecycles to shorten OEM qualification cycles and lower commercial friction.

- Move up the value chain: Bundle models with validation services, data capture and analytics (e.g., device-tissue interaction metrics) to shift from one-off sales to recurring-service revenue.

- Prioritize partnership and M&A plays: Target bolt-on acquisitions that add complementary manufacturing methods, geographic fulfillment nodes or domain-specific model catalogs (neuro, coronary, peripheral).

Scenario planning — practical lenses for 2026 investment committees

- Base case (planning baseline): Continued steady growth driven by training and device R&D adoption aligned to our 7.51% CAGR forecast. Investment in scalable production and certification yields predictable ROI.

- Innovation-accelerated case: Rapid adoption of patient-specific models and integrated software platforms accelerates premium product demand—favor firms with strong imaging-to-print pipelines and software partnerships.

- Regulatory-tightening case: Stricter standards for simulated testing create a barrier that benefits larger, certified suppliers; smaller players will need third-party validation or risk market exclusion.

- Supply-shock case: Raw-material disruptions push near-term prices up and compress margins. Hedging, vertical integration or strategic sourcing alliances mitigate downside.

How to use the report in boardroom decisions

Our research translates into concrete deliverables for decision-makers:

- CapEx and capacity planning: Model the investment horizon for additive versus molding capacity under multiple adoption curves.

- M&A screening: A shortlist of targets based on technology fit, geographic coverage and customer overlap—supported by a valuation sensitivity model.

- Commercial GTM playbooks: Tailored routes to market for device OEMs, academic training centers and hospital purchasers, including pricing tiers and service-bundle recommendations.

- Regulatory roadmap: A prioritized checklist to move products through testing and into regulated use cases with minimal rework.

Next steps and where to find the full intelligence

This briefing demonstrates the strategic value of focused intelligence on the medical silicone vasculature models market as 2026 decisions are crystallized. For teams that need transaction-grade data, detailed segmentation matrices, vendor scorecards and the full dataset behind our forecasts, PW Consulting’s full report and interactive model are available. Clients seeking a tailored workshop, due-diligence support or M&A advisory tied to this market should contact our Healthcare Strategy practice for a priority briefing and bespoke scenario run tailored to your portfolio.

For detailed analysis of this topic, please visit the official page:Medical Silicone Vasculature Models Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com