Three Phase Cast Resin Transformer Market: Strategic Imperatives for 2026

As organizations accelerate electrification, grid modernization, and urban densification, three phase cast resin transformers are moving from niche safety-driven choices to strategic infrastructure assets. PW Consulting’s Three Phase Cast Resin Transformer Market report (base year 2025; forecast 2026–2032) synthesizes longitudinal market data, regulatory trajectories, and supplier moves into a decision-grade roadmap for executive teams preparing investment, product and procurement choices in 2026. The analysis is purpose-built to reveal strategic inflection points while preserving proprietary granularity—this release is a concise preview designed to surface the insights that will materially affect 2026 planning cycles.

Three Phase Cast Resin Transformer Market

Macro dynamic: a stable growth runway

The market demonstrates a sustained growth trajectory across the last half-decade and into the next business cycle. From the post-2020 recovery the market expanded through 2025, reaching a robust base year size, and the PW Consulting forecast projects continued expansion through 2032 at a compound annual growth rate of 6.85% (2026–2032). This cadence reflects structural demand drivers—electrification of industry, decentralized generation and storage, mission-critical infrastructure build-outs, and an increasing preference for oil-free, low-maintenance distribution equipment in urban and indoor environments.

Three Phase Cast Resin Transformer Market

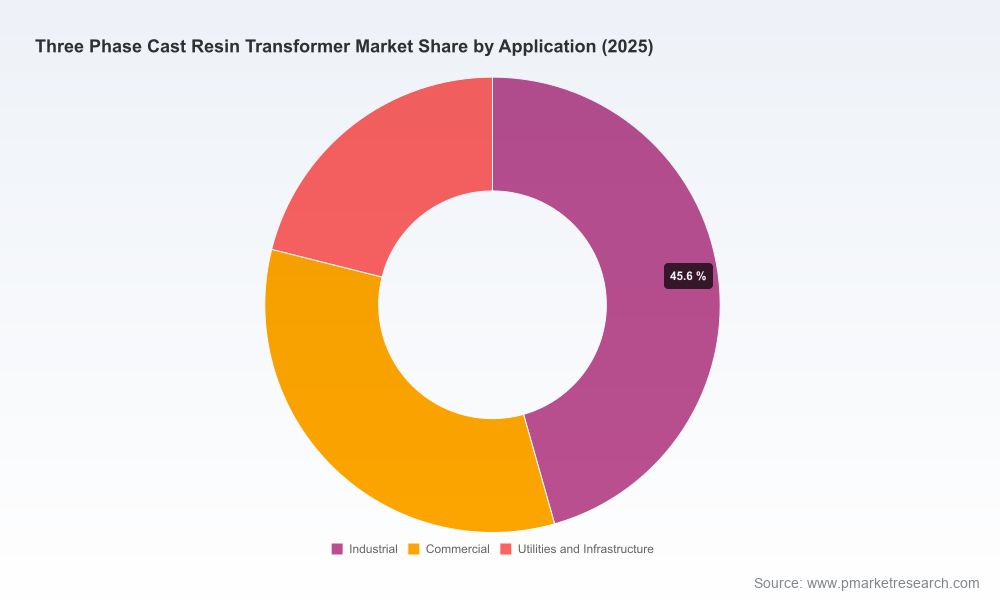

- Growth profile: historical expansion into 2025 established a larger installed base and a deeper replacement/modernization pipeline; forecasted growth to 2032 underlines multi-year demand visibility for manufacturers and buyers.

- Concentration: market share concentration is moderate at the top tiers, leaving room for regional specialists and technology-focused entrants to create differentiated positions.

Why 2026 is a decision inflection point

Several converging factors make 2026 the year when board-level decisions about capex, footprint, and product strategy should be finalized:

Three Phase Cast Resin Transformer Market

- Regulatory momentum: evolving efficiency and ecodesign requirements in key markets require product roadmaps to incorporate lower-loss designs and validated compliance testing. This creates both compliance risk and product-differentiation opportunities for firms that act early.

- Input-cost volatility: epoxy-based encapsulants and other core inputs have shown price and availability swings. Supply-chain risk is now an operational variable that should be explicitly modeled into pricing, sourcing, and contractual terms.

- Demand-side shifts: customers are prioritizing fire-safe indoor solutions, lower lifecycle losses, and compact footprints—criteria that change procurement specifications and create upsell pathways for premium product variants.

- Capacity and localization choices: manufacturers that committed to targeted capacity expansions or regional production in recent years are better positioned to capture near-term opportunities; buyers assessing long-term supplier resilience should incorporate footprint and scale into preferred-vendor selection.

Strategic implications — actionable priorities for 2026 planning

Executives should convert market signals into specific 2026 actions across product, supply chain and commercial functions. The following priorities are immediately actionable and grounded in the report’s modeling and scenario analysis.

- Product roadmaps — Accelerate low-loss and fire-safe variants to meet upcoming efficiency and ecodesign requirements. Prioritize modular platforms that allow power-rating and environmental-class customization without full redesign.

- Procurement and supplier strategy — Move from single-source spot-buying to multi-tiered supplier panels with contractual levers for input-cost pass-throughs and volume-flex options. Lock in technical acceptance criteria tied to IEC standards in contracts.

- Manufacturing footprint — Reassess near-market production as a hedge against freight constraints and long lead-times; use scenario models to quantify breakeven horizons for regionalizing assembly versus centralized manufacture.

- Aftermarket and service — Commercialize predictive maintenance and lifecycle-loss audits as premium services that improve total cost of ownership for end customers and deepen customer relationships.

- M&A and partnerships — For manufacturers seeking scale or capability, prioritize bolt-on acquisitions that add specific climate classes, high-MTBF designs, or seismic-hardened qualifications which are hard to replicate organically.

- Cost-to-serve optimization — Revise pricing models to reflect installation complexity, urban delivery constraints, and aftermarket service potential rather than pure unit-cost markups.

Competitive landscape — who to watch and why

The ecosystem is diverse: global original equipment manufacturers, European specialists, Asian volume players, and regional pure-plays each bring distinct capabilities. PW Consulting’s competitive framework evaluates firms across technology breadth, manufacturing footprint, environmental-class certifications, and go-to-market focus.

- Global OEMs — Several multinational energy and industrial groups combine deep R&D and broad aftermarket networks. These firms compete on integrated system offerings (renewables, distribution automation) and reliability credentials.

- European specialists — Producers with historic expertise in cast resin designs emphasize high MTBF and compliance with demanding environmental classes—appealing to utility and industrial buyers focused on lifecycle performance.

- Asian and emerging-market players — Cost-competitive manufacturers leverage scale and agile production to serve expanding regional demand, often with faster lead-times for certain configurations.

- Niche innovators — Technology-focused firms and select regional suppliers differentiate through compact, lightweight topologies and application-specific customization (data centers, offshore renewables, seismic zones).

Notable strategic moves have accelerated competitive dynamics in recent quarters: some leading suppliers have publicly expanded production capacity in priority markets, while product launches have emphasized compact, installation-friendly packages. These developments increase short-term capacity availability in certain corridors and raise the bar on product specifications. For procurement teams, supplier selection in 2026 should therefore be informed both by product fit and by validated production resilience.

What PW Consulting’s report contains — the practical toolkit

The full report translates market-level insights into tools that teams can deploy during budgeting, sourcing, and product planning cycles. Highlights of the deliverables include:

- Market sizing and forecast methodology with transparent assumptions and sensitivity scenarios for alternate macroeconomic and commodity price paths.

- Scenario-based demand models segmented by power-rating bands, application classes and regions (granular tables and interactive worksheets are included in the full report)

- Supplier scorecards that evaluate technology, capacity, certification, and commercial flexibility—built for RFP shortlists rather than academic ranking.

- Regulatory and standards compliance matrix with recommended product features and testing checkpoints mapped to major jurisdictions and upcoming deadlines.

- Cost-model templates that allow buyers and manufacturers to simulate the impact of raw-material price shocks, freight permutations and tariff scenarios on unit economics.

- Procurement playbook with contract clauses, acceptance-test templates, and inventory policy recommendations to mitigate lead-time and quality risk.

- Manufacturing footprint decision framework that quantifies trade-offs between localization, scale economies and time-to-market for new variants.

- Technology roadmap and product prioritization matrix—an executable plan for R&D investment allocation across loss-reduction, fire performance, and compact-design tracks.

How executives should use this preview

Consider this briefing a strategic North Star for 2026 choices. Boards and executive committees should use the signals above to fast-track three pragmatic deliverables before the next budgeting cycle closes:

- Approve targeted R&D investments that align with regulatory timelines and customer willingness-to-pay for lifecycle savings.

- Undertake a supplier resilience audit that stress-tests current contracts against raw-material volatility and lead-time shocks.

- Define a localized production or assembly strategy for priority markets where speed-to-deployment and regulatory compliance create a premium.

All three actions are low-latency in execution yet high-impact in terms of exposure reduction and capture of upside demand.

Next steps — where to get the full intelligence

This release is intentionally compact: it surfaces the strategic lines of force and the operational priorities that PW Consulting clients will use in 2026. The full Three Phase Cast Resin Transformer Market report provides the confidential, drill-down datasets, segmented forecasts, supplier benchmarks, and executable templates referenced above. For procurement teams, product leaders, and investors who require the detailed tables, model files, and supplier heatmaps that power transaction-grade decisions, we invite you to access the complete study via PW Consulting’s research portal.

In an industry where regulatory thresholds, material inputs, and deployment contexts are changing fast, having a forward-looking, scenario-ready playbook is not optional. PW Consulting’s analysis equips leaders to transform strategic intent into implementable plans during 2026—while preserving the tactical confidentiality that successful execution requires.

For detailed analysis of this topic, please visit the official page:Three Phase Cast Resin Transformer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com