Renewable Silica Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

Executive summary

The renewable silica market is transitioning from niche sustainability experiments to structured commercial expansion. Between 2020 and 2025, the market more than doubled in scale, and our modeling indicates a steep acceleration across the next phase of commercialization. With the market expected to grow from approximately USD 366.4 million in 2025 to an output trajectory that exceeds USD 1.1 billion by the end of the 2026–2032 forecast window, the sector is moving into a stage where supply-chain decisions, certification strategies and early-mover commercial plays will determine competitive leadership. The compound annual growth rate (CAGR) for the forecast period is 18.01%, underscoring the urgency for corporate planning in 2026.

Renewable Silica Market

Why 2026 is a make-or-break year for corporate strategy

2026 will mark the moment when pilot projects and capacity announcements transition into tangible market supply and customer procurement commitments. Several leading producers have signaled capacity expansions and first-in-region commercial launches timed around 2025–2026, which creates a narrow window for downstream players (tire, rubber, coatings, personal care, food & pharma) and investors to secure feedstock, qualifying processes and off-take terms under sustainable certification regimes.

Renewable Silica Market

- Timing: Planned plant ramp-ups and product launches mean 2026 is the year when pipeline commitments convert into commercial availability.

- Procurement leverage: Buyers who define feedstock sourcing and certification requirements in 2026 can lock competitive advantage into supplier contracts that last multiple years.

- Regulatory and brand risk: Early sustainability claims, certification choices and product labeling established in 2026 will influence marketing and regulatory exposure for the next decade.

Market trajectory and what the headline numbers hide

Headline market sizing shows a clear expansion from 2020 (approx. USD 168.5 million) to 2025 (approx. USD 366.4 million) and a forecast path that reaches the billion-dollar scale by the early 2030s. While these macro figures demonstrate the strong overall momentum, they mask several structural dynamics that are essential for board- and C-suite-level decisions:

Renewable Silica Market

- Concentration dynamics: Market share is unevenly distributed—leading producers control a meaningful share of production capacity, creating both entry barriers and acquisition opportunities for strategic investors.

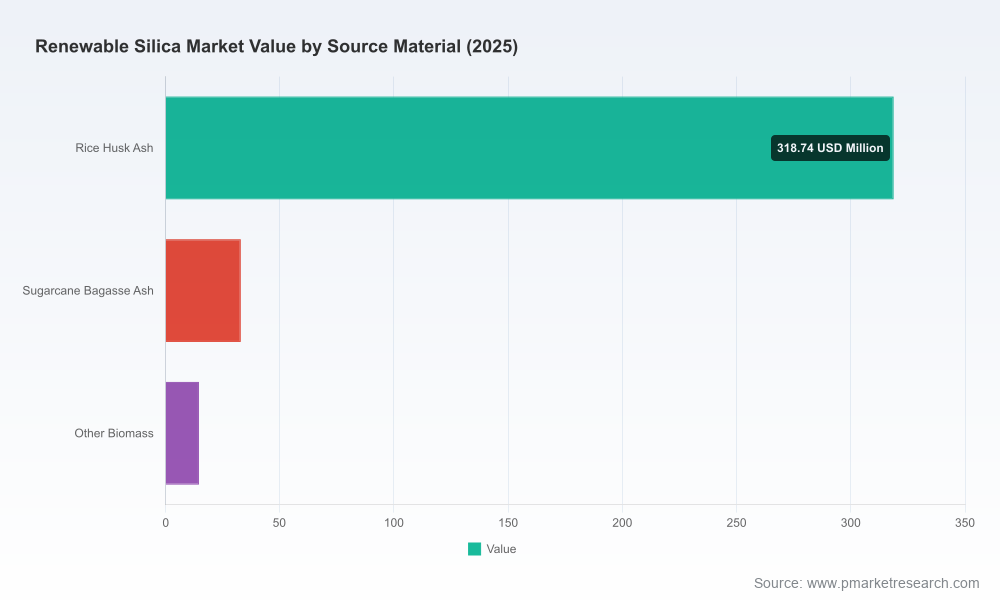

- Feedstock-driven economics: Agricultural by-products (notably rice husk ash) are the primary upstream feedstock; variability in composition and logistics materially impacts plant yields and product unit economics.

- Certification and carbon accounting: The emergence of circular and bio-circular product claims, and certifications accepted by large OEM buyers, will create premium versus commodity pockets within the renewable silica market.

Our report provides detailed scenario mappings that connect these structural variables to sensitivity on price, margins and break-even timing—information we purposefully reserve for the full study to support transaction-level confidentiality.

Competitive landscape — who matters and why

The competitive set combines legacy specialty chemicals incumbents with agile regional challengers focused on bio-based feedstocks. This hybrid landscape affects customer expectations, technology diffusion and acquisition activity.

- Solvay S.A. (Brussels, Belgium) — Recently launched a bio-circular highly dispersible silica (HDS) product derived from rice husk ash at its Italian site and is executing a global circular silica roadmap. Solvay’s combination of geography, product breadth and sustainability certification strategy positions it as a key supplier for multinational OEMs pursuing rapid decarbonization goals.

- Evonik Industries AG (Essen, Germany) — Maintaining leadership in precipitated silica technology, Evonik is expanding capacity in North America to serve green tire demand. Their approach blends incremental capacity with process optimization for high-performance grades.

- Blue Ocean Biotech (India) — An example of a vertically integrated green-startup model: local feedstock access, green energy integration and focused capacity ramp plans. Such players are proving that regionally optimized, low-cost production can scale rapidly where feedstock logistics are favorable.

- Regional specialists and new entrants — Several firms (Brisil, Green Silica Group, BSB Nanotechnology, Ekasil, Madhu Silica, Biosilico and others) are commercializing rice husk-derived grades and other biomass-sourced silicas. Their strategic advantage lies in local feedstock networks, lower capex footprints and tailor-made customer service for regional supply chains.

Collectively, the top-three and top-five producers capture a material share of the market; our concentration analysis indicates meaningful aggregation among the largest suppliers, creating both supply-side resilience risks and acquisition targets for industrial players seeking rapid entry.

Supply chain, feedstock and processing considerations

Rice husk ash is the dominant upstream feedstock in renewable silica production. While abundant in many agrarian regions, its quality varies by variety, harvest and post-harvest handling—introducing processing complexity that affects yields and product consistency. These technical constraints should directly inform sourcing strategies, capex allocation for pretreatment, and supplier qualification protocols.

- Feedstock contracts: Multi-year sourcing agreements with quality bands are critical to stabilize plant throughput and to reduce variability-driven margin leakage.

- Process investments: Capital allocation should prioritize pretreatment, quality-control labs and modular scaling to accommodate feedstock heterogeneity.

- Certification alignment: Selecting certification schemes acceptable to target end-markets (e.g., tire OEM sustainability programs) will affect premium capture and customer acceptance.

Technology, emissions and certification — the new battleground

Technical differentiation is shifting from basic silica performance to lifecycle emissions, circularity of inputs and traceability. Manufacturers that can demonstrably reduce CO₂ intensity per ton—either through process innovations or through use of waste-derived feedstocks—will command a pricing premium with large corporate buyers. Some producers have publicly quantified significant per-ton CO₂ reductions from bio-circular processes; such claims will become central to commercial dialogues.

Commercial strategies and M&A themes to watch in 2026

Given the rapid market growth and the mix of incumbent and regional players, we expect the following strategic plays to define 2026 activity:

- Strategic offtake + equity: Downstream customers entering minority stakes in regional bio-silica producers to secure supply and co-develop product specifications.

- Bolt-on acquisitions: Specialty chemicals incumbents acquiring local feedstock-managed players to accelerate regional footprint and reduce time-to-market.

- Capex phasing: Phased modular investments that enable 2026 commercialization while preserving optionality for capacity scaling under proven product performance.

- Certification-led premiuming: Investments in traceability and ISCC+ or equivalent credentials to capture sustainability premiums from brand-sensitive customers.

What PW Consulting’s full report delivers (practical & actionable)

Our full Renewable Silica Market report is structured to support both enterprise strategy and transaction teams. Highlights include:

- Robust market sizing and multi-scenario forecasts (2026–2032) with sensitivity to feedstock cost, capex timing and certification uptake.

- Commercial models and unit-economics templates—ready to plug in your capex and feedstock assumptions for board-level decision-making.

- Supplier due-diligence checklists, feedstock QA templates and contract clauses designed for renewable silica sourcing.

- Technology-readiness assessments and a comparative matrix of production routes, energy profiles and emissions baselines.

- Detailed competitor profiles and strategic heat maps (including capacity pipelines, geographic focus and product specialties).

- Go-to-market playbooks for each downstream vertical, including customer segmentation, price-premium capture strategies and co-development models.

- M&A screening tools and valuation approaches calibrated for specialty material assets with sustainability premiums.

To honour the preview nature of this release and maintain commercial discretion, we have intentionally withheld granular regional and application-specific revenue splits from this summary. The full dataset and interactive dashboards—integral to executing 2026 decisions—are available through the complete report.

Recommendations for C-suite and investment committees in 2026

- Adopt a two-track sourcing strategy: secure short-term regional offtakes to validate supply while negotiating scalable long-term contracts tied to quality bands and certification milestones.

- Prioritize modular capex: design plants that can start commercial runs in 2026 and scale with demand visibility, limiting stranded asset risks.

- Invest in certification infrastructure: early alignment with recognized circularity standards will unlock premium procurement pipelines, particularly with multinational OEMs.

- Build feedstock resilience: diversify sourcing corridors and invest in upstream aggregation or partnerships to mitigate variability in rice husk ash quality.

- Prepare M&A playbooks: have evaluation criteria ready for bolt-on producers that can be integrated quickly to secure regional scale.

Final note — the strategic value of the PW Consulting report

For executives making 2026 allocation and sourcing decisions, the value of timely, transaction-grade insight cannot be overstated. Our report translates headline growth into executable actions: precise sourcing blueprints, capex phasing models, and deal-structuring templates that align with sustainability certification and downstream performance requirements. The renewable silica market’s projected CAGR and overall growth trajectory create both opportunity and risk—those who act in 2026 with validated economic models and supply certainty will shape market standards for the decade.

For access to the comprehensive dataset, scenario tools and company-level teardown analyses, please refer to the full Renewable Silica Market report available through PW Consulting’s publication portal.

For detailed analysis of this topic, please visit the official page:Renewable Silica Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com