North America Standard Surgical Gowns Market Trends, Demand and Revenue Forecast

Health |

2026-06-09 09:41:18

PW Consulting’s latest Elevator And Elevator Control Market study provides a purpose-built intelligence package to inform capital allocation, product roadmaps, M&A screening, and service strategy for 2026. Our industry-wide model shows an established global market that expanded from roughly USD 81.5 billion in 2020 to about USD 105.4 billion in 2025, with a continuation of growth through our forecast horizon. We project a compound annual growth rate (CAGR) of approximately 5.51% over 2026–2032, taking the market toward an estimated USD 153.4 billion by 2032 under our base case assumptions.

Elevator And Elevator Control Market

Timing matters: 2026 is the inflection point between recovery-era retrofit demand and a new wave of sustainability- and automation-driven investments. Firms that align product development and service offerings now will capture disproportionate margin improvement through 2028–2030.

Elevator And Elevator Control Market

Regulatory convergence is accelerating capital needs: Fresh codes and international standards published in 2025–26 create an immediate compliance runway for global operators, while also opening opportunities for value-added modernization services and certified components.

Elevator And Elevator Control Market

Consolidation optics: The market exhibits material concentration among incumbent OEMs and a strengthening band of control-component specialists—making M&A and partnership strategy central to profitable growth.

Top-down market sizing and bottom-up scenario forecasts (historic 2020–2025 calibration; forecast 2026–2032). Models include sensitivity to construction cycles, urbanization indices, and service-market elasticity.

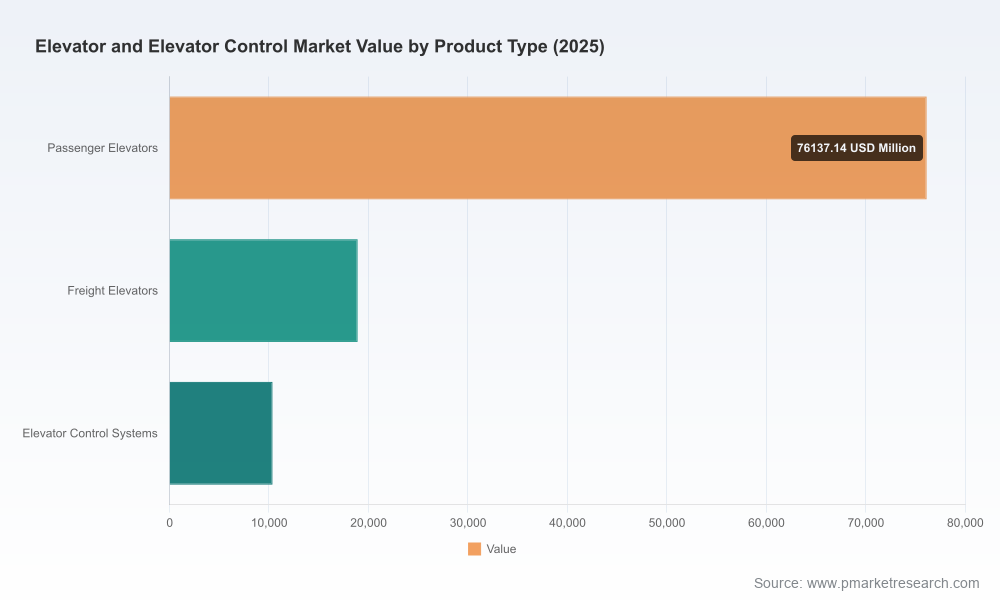

Segmentation frameworks across product type, end-use sector, and region — with strategic implications for pricing, aftermarket, and retrofit streams. (Note: detailed regional and application-level tables are reserved for the full report.)

Supply-chain cost map: inputs, pass-through dynamics, and hedging playbooks focused on primary inputs such as steel and iron ore, which continue to drive manufacturing cost volatility.

Standards and compliance tracker: practical steps to adopt ASME/CSA updates and the new ISO 8100 series, plus certification timelines and cost-to-compliance benchmarks.

Technology assessment: vendor-agnostic review of regenerative drives, IoT-enabled controls, AI-driven traffic prediction, dual-channel safety architectures, and machine-room-less platforms.

Competitive playbooks: profiles, SWOT-style strategic options, partnership matrices and a live M&A watchlist covering global OEMs, control-component suppliers, and regional champions.

Commercialization guides: go-to-market approaches for OEMs, independent service providers, controls vendors and property owners, plus 30/100/365-day implementation checklists.

Shift from unit sales to lifecycle economics. With modernization and service accounting for an increasing share of value capture, executives should re-calibrate KPIs to emphasize installed-base margin and recurring revenue growth.

Product roadmap prioritization. Energy efficiency (regenerative systems), safety redundancy (dual-channel controllers), and connectivity (secure IoT stacks) are now baseline requirements in new high-rise and mission-critical specifications. Faster adoption yields premium pricing and lower warranty spend.

Supply-side resilience is strategic. Volatility in steel and iron-ore inputs will continue to create episodic margin pressure; procurement strategies, longer hedges, and component localization should be evaluated alongside price-indexed contract clauses.

Regulatory readiness as advantage. Early adherence to ISO 8100-series and updated ASME/CSA rules converts compliance into a competitive differentiator for global bidders.

M&A and partnerships to close capability gaps. The market’s concentration—with top-three players commanding a meaningful share and top-five an even larger one—means inorganic approaches remain efficient paths for scale, technology access, and geographic reach.

Our synthesis of public filings, product launches, and facility investments shows incumbents doubling down across three axes: product modernization, digital services, and mission-critical solutions.

Otis Worldwide continues to reinforce its leadership through targeted product introductions and modernization packages tailored to data centers and low‑/mid‑rise retrofits. Recent heavy-duty and flexible modernization offers signal a play to capture both mission-critical new-builds and the high-margin modernization wave.

KONE emphasizes energy-efficient, connected elevators with advanced safety controllers; its dual-channel controller architecture and focus on smart operations make it a top choice for sustainability- and resiliency-focused clients.

Schindler and TK Elevator are focusing on sustainability and platform efficiency—Schindler through IoT-driven operations and TK with eco-efficient platforms—both pursuing combined hardware-plus-service models.

Japanese and Korean manufacturers (Mitsubishi Electric, Hitachi, Fujitec, Toshiba, Hyundai) are leveraging high-performance controls, high-speed capabilities and bespoke solutions for dense-urban high-rise projects and vertically integrated customers.

Control-component specialists and motor suppliers (Inovance, Nidec, Shanghai STEP, others) are critical nodes in the ecosystem; their product roadmaps materially affect differentiation in ride quality, safety redundancy, and energy recovery.

New heavy-duty and modernization product launches by leading OEMs signal prioritization of mission-critical and retrofit segments—areas where margins and recurring service potential are highest.

Facility expansions and innovation labs indicate continued investment in integrated control and AI capabilities; suppliers investing in labs and development hubs will shorten time-to-market for advanced offerings.

Standards updates and harmonization (North American safety code updates and the new ISO 8100 series) are changing procurement specifications globally and creating near-term demand for certified upgrades and recertification services.

Base case (CAGR ~5.5%): Gradual adoption of smart controls and steady retrofit activity. Actions: prioritize service-led growth, invest in certified modernization packages, and protect installed base through remote monitoring contracts.

Accelerated electrification & sustainability upside: Faster roll-out of green building mandates and incentive programs drive premiumization. Actions: accelerate productization of regenerative drives and energy-as-a-service offers; position for green-label certifications to win municipal and institutional business.

Downside stress (macro slowdown/raw-material shock): Construction contraction and input-price spikes compress margins. Actions: execute cost-to-serve redesigns, tighten working capital, and opportunistically pursue distressed M&A to acquire service footprints at attractive multiples.

Day 0–30: Run the downloadable financial model against your own KPI set to identify stress points under different commodity and construction scenarios.

Day 30–60: Prioritize a 3‑point product roadmap (safety redundancy, energy recovery, connectivity) and initiate one pilot in a target geography or vertical.

Day 60–100: Execute at least one partnership or small acquisition to fill a capability gap—controls, software, or regional service network—and update procurement contracts with indexed clauses to manage steel-price risk.

This preview intentionally emphasizes insight and strategic framing while withholding granular region- and application-level tables, vendor-by-vendor revenue splits, and the raw datasets that power our models. The full report includes the complete segmentation matrices, downloadable scenario models, supplier heatmaps, a detailed M&A target list, and an implementation playbook with contract templates and compliance checklists—tools designed to convert insight into measurable commercial outcomes in 2026.

The Elevator And Elevator Control market in 2026 is neither a commodity space nor a static engineering market. It is a capital‑intensive, regulation-driven platform for recurring service, software-enabled differentiation, and sustainability-linked revenue. With an established growth trajectory and a clear set of regulatory and technological inflection points, the executives who translate the report’s scenario intelligence into concrete product, procurement, and M&A moves over the next 12 months will set the strategic position for the decade ahead.

For access to the full datasets, scenario models, and operational playbooks that underpin this analysis, please visit PW Consulting’s report page and download the complete Elevator And Elevator Control Market study.

For detailed analysis of this topic, please visit the official page:Elevator And Elevator Control Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com