PW Consulting Forecast: Logistics & Cold Chain Market to Grow at a Robust 8.5% CAGR

Other |

2026-07-02 17:33:44

As the payments industry accelerates toward biometric-first experiences, PW Consulting’s latest market intelligence on facial recognition payment devices frames a clear, actionable strategy for enterprise decision-makers preparing for 2026. Our new analysis synthesizes commercial adoption patterns, regulatory inflection points and vendor dynamics to help payments architects, retail operators, device OEMs and investors allocate capital and prioritize pilots with confidence.

Facial Recognition Payment Devices Market

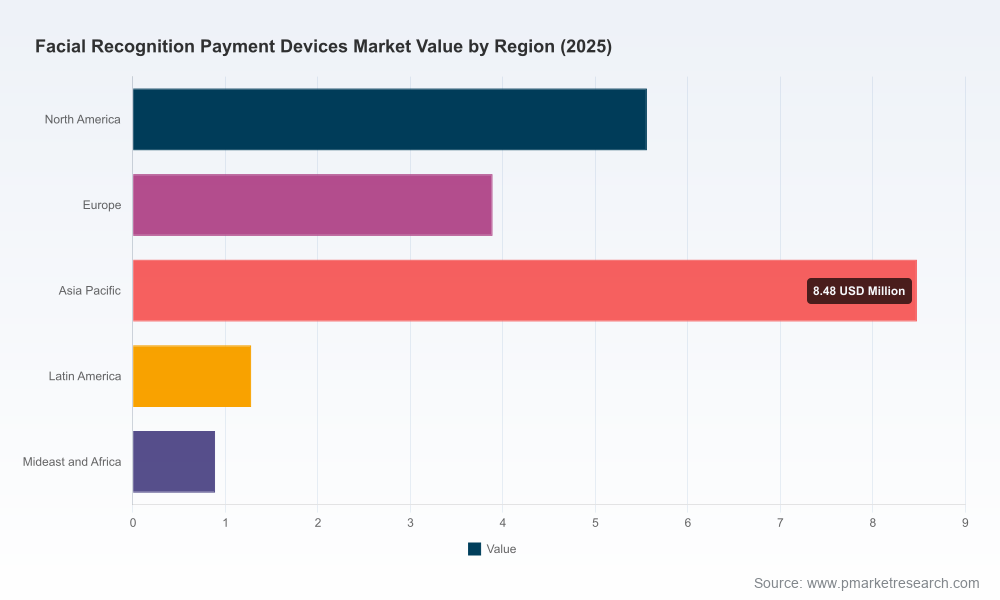

The facial recognition payment devices market is transitioning from early experimentation to scalable commercial deployments. Our modeling shows the market expanding at a compound annual growth rate (CAGR) of 19.85% over the near-medium term. From the report’s base year of 2025 — where the overall market size is reported at USD 20.1 Million — the market is projected to grow substantially through the forecast period 2026–2032, reaching USD 73.25 Million by 2032. This growth profile highlights a persistent opportunity for product innovation, integration with payment rails, and value capture across hardware, firmware and services layers.

Facial Recognition Payment Devices Market

Validate scale hypotheses: The projected near-20% CAGR indicates that pilots validated in 2024–25 can scale to commercial rollouts in 2026 with appropriate vendor selection and regulatory guardrails.

Facial Recognition Payment Devices Market

Prioritize composable stacks: The economics favor modular solutions — combining camera/3D sensing modules, local edge inference and cloud-based identity orchestration — over vertically closed terminals, particularly where integration with existing POS and payment processors is required.

Plan for regulatory differentiation: Compliance and privacy engineering will be a competitive moat. Companies that demonstrate robust necessity assessments, data minimization, and auditable models will unlock enterprise customers in regulated jurisdictions.

PW Consulting’s report is engineered for execution. Highlights include:

A granular market-size model (historical 2020–2025, base year 2025, forecast 2026–2032) and sensitivity scenarios to stress-test investments against slower and faster adoption curves.

Vendor benchmarking across product portfolios, technical capabilities (2D/3D sensing, liveness, edge AI), go-to-market routes, and partner ecosystems.

Commercial playbooks for pilots and rollouts tailored to high-opportunity verticals such as quick-serve retail, transportation and unattended commerce.

Regulatory readiness checklists (data processing impact assessments, consent flows, local registration requirements) mapped to major jurisdictions.

Implementation templates including TCO drivers, POS integration patterns, and sample contracting clauses for data handling and liability.

The market is characterized by a mix of hardware-centric OEMs, software-first specialists and integrated solution providers. Market concentration metrics indicate a moderate level of concentration (CR3 ~38.5%, CR5 ~52.7%), illustrating that while a handful of vendors capture meaningful share, there is still room for regional specialists and technology-focused challengers.

NEC Corporation (Tokyo): A leader in large-scale deployments and systems integration, NEC has demonstrated face recognition payment flows at marquee events and large venues. Its strength is end-to-end systems, which appeals to enterprises seeking turnkey, enterprise-grade deployments.

PAX Technology (Shenzhen): Positioned at the convergence of Android smart POS and biometric integrations, PAX is expanding its footprint through partnerships that add multimodal biometrics to mainstream POS platforms — a critical path for mainstreaming facial recognition in retail.

Newland NPT & Telpo (China): These device OEMs focus on smart POS and unattended terminals with embedded facial recognition, targeting retail and kiosk use cases. Their advantage is deep channel access in large domestic markets and integrated device offerings for quick deployments.

VisionLabs, PopID, PayByFace, Intema: Software and service specialists that excel at biometric matching, identity orchestration and verticalized flows (e.g., quick-serve restaurants). They provide the software glue and integrations that enable hardware OEMs to deliver compelling user experiences.

Orbbec: A key supplier of 3D sensing modules and cameras, Orbbec underpins the hardware stack where depth sensing materially improves accuracy and liveness detection — a technical differentiator in higher-risk payment scenarios.

Recent market moves underscore two dynamics: first, ecosystem convergence (payment processors and device OEMs collaborating to create frictionless flows), and second, accelerated productization of biometric authentication on mainstream POS terminals. Examples include high-profile demonstrations of hands-free checkouts and commercial partnerships integrating multimodal biometric stacks into existing POS families.

Regulation is a defining variable in 2026 strategy. Two recent developments crystallize the landscape:

China’s Security Management Measures for Facial Recognition Technology (effective June 2025) raises the bar for necessity justification, limits mandatory use where alternatives exist, and requires registration for large-scale processing of facial data. This shifts procurement toward documented purpose-limitation and transparent consent frameworks.

The EU AI Act’s high-risk requirements for biometric systems (effective from August 2025) introduce obligations around risk assessments, audit trails and bans on certain emotion-scoring use cases — constraining feature roadmaps but also creating an advantage for vendors that bake compliance into their products.

Implication: regulatory compliance is not optional; it is a market entry requirement in many jurisdictions. Enterprises should budget for legal, privacy and technical controls as part of the core project cost, not as an afterthought.

For executives sizing up investments and pilots in 2026, PW Consulting recommends a focused set of moves:

Adopt a “privacy-by-design” procurement rubric: require vendors to provide necessity justifications, data retention policies and portability mechanisms as part of RFP responses.

Favor modular architectures: choose vendors that expose APIs and support integration with existing POS middleware and payment processors to reduce vendor lock-in and accelerate deployment.

Invest in multimodal biometrics & liveness: combine facial recognition with complementary signals (e.g., PIN, tokenized card, behavioral analytics) to manage fraud risk and meet regulatory expectations.

Run jurisdictional pilots: validate consent models and operational workflows in representative markets before scaling cross-border — regulatory nuances materially affect deployment timelines.

Build supplier diversity into sourcing: balance established systems integrators and regional OEMs with specialist software providers to optimize cost, performance and compliance.

Embed measurement into rollouts: define KPIs for authorization success rates, false acceptance/rejection, throughput impact and customer sentiment to guide iterative product improvements.

Position for ecosystem partnerships: where possible, form early alliances with payment processors and major POS OEMs to access merchant channels and accelerate adoption curves.

Given the projected growth and current competitive dynamics, the most attractive opportunities for 2026 are:

Edge AI and 3D sensing suppliers that improve accuracy and reduce reliance on central matching.

Middleware providers that standardize identity orchestration across POS families, enabling merchant-led opt-in experiences.

Compliance tooling — assessment frameworks, consent orchestration and audit logging — that simplify cross-border deployments.

Verticalized applications in quick-service retail and unattended commerce where speed and frictionless checkout yield measurable lift.

Facial recognition payment devices are moving from niche pilots to a phase where robust technical capabilities, regulatory fitness and partner ecosystems determine winners. The market’s projected trajectory — underpinned by near-20% CAGR and a more-than-threefold expansion from the 2025 base through 2032 — creates a landscape where disciplined investment and nimble execution will be rewarded.

PW Consulting’s full report provides the granular segmentation, vendor scorecards, and deployment playbooks needed to operationalize these insights. For leaders who want to turn 2026 into a year of measurable adoption — not just experimentation — the detailed analysis and practical templates in our study are designed to shorten decision cycles and de-risk scale.

Contact PW Consulting to access the complete market model, vendor matrices, and implementation toolkits that underpin this strategic outlook.

For detailed analysis of this topic, please visit the official page:Facial Recognition Payment Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com