Roll Coating Machine Market: Strategic Imperatives for 2026 — PW Consulting Industry Brief

Executive snapshot

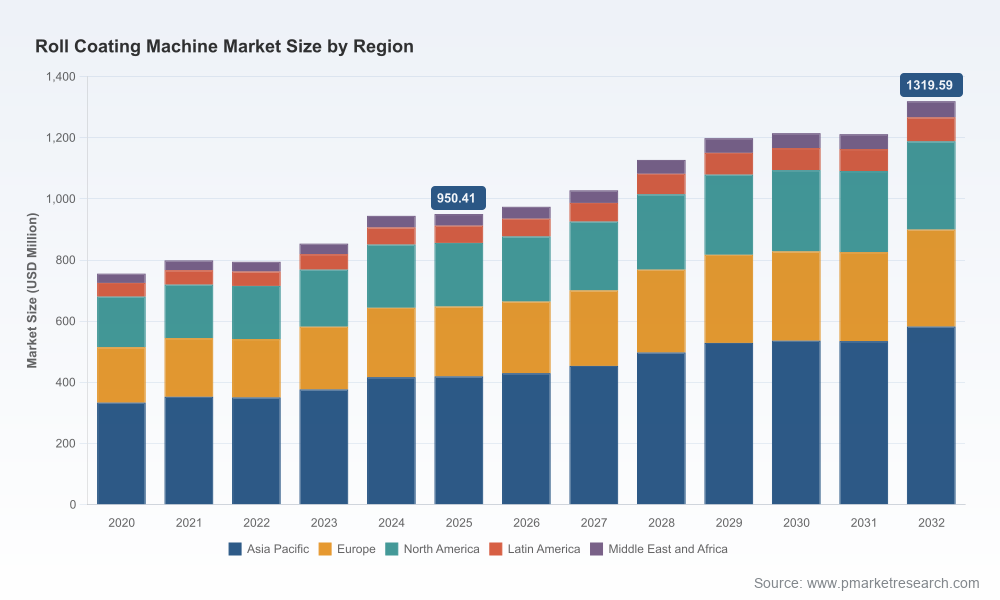

As manufacturing supply chains recalibrate for a new industrial cycle, the global roll coating machine market stands out as a strategic investment node for capital equipment planners and industrial OEMs. Our PW Consulting base-year assessment (2025) places the market at approximately USD 950.4 Million. Through the 2026–2032 forecast horizon the market is expected to grow at a steady compound annual growth rate (CAGR) of 4.8%, reaching roughly USD 1.32 Billion by 2032. That steady trajectory masks meaningful pockets of technology disruption, input-cost sensitivity and consolidation opportunities that will determine winners in the next three years.

Roll Coating Machine Market

Why this market matters for 2026 decision-makers

- Capital allocation: Buyers planning CapEx cycles in 2026 must balance replacement/expansion needs against rapidly evolving coating technologies (precision sub-micron coating, high-speed web handling and integrated metallization) that materially affect total cost of ownership.

- Supply chain exposure: Roll coating equipment is steel- and components-intensive. Recent commodity dynamics — including rising hot-rolled coil pricing and regional tariff measures — are reshaping sourcing, lead times and supplier risk profiles.

- Aftermarket and services: With a fragmented manufacturing base and multiple specialized OEMs, aftermarket services, retrofits and predictive maintenance are becoming primary revenue and margin levers for equipment vendors and solution partners.

Market dynamics: what is actually shifting

The near-term market behavior is being driven by three interacting forces. First, end-market demand from packaging, furniture, automotive and energy materials continues to diversify coating requirements (from high-gloss decorative finishes to functional, electrode-grade coatings). Second, raw material pressure — notably steel price increases and import tariff environments — is forcing procurement teams to reassess supplier geographies and inventory strategies. Third, technology innovation (automation, advanced slot-die and microgravure systems, in-line metallization) is compressing lifecycle economics: buyers that adopt newer platforms can achieve higher throughput and lower per-unit operating cost, but only if they align CapEx timing with production roadmaps.

Roll Coating Machine Market

What we found — data-driven highlights (high-level)

- Resilience: The market rebounded through the early 2020s and reached an estimated USD 950.4 Million in 2025, reflecting broad-based industrial demand and investment refresh cycles.

- Moderate growth: A 4.8% CAGR through 2032 reflects continued modernization across end-markets rather than explosive new-adoption dynamics; growth will be concentrated in upgraded automated systems and specialty coatings rather than across-the-board volume expansion.

- Fragmentation: Market concentration metrics show a dispersed supplier base — the top three suppliers account for under one-fifth of the market, and the top five capture less than a third. This fragmentation creates both procurement complexity and M&A runway for strategic consolidators.

Competitive landscape — how to read the vendor map

The roll coating machine sector blends global multinationals and highly specialized regional players. Our workbench mapping identifies several archetypes that matter for procurement and strategic partnerships:

Roll Coating Machine Market

- Full-system integrators: Companies that supply end-to-end, high-throughput coating and laminating lines for packaging and metal coil markets. These players win on systems engineering and project delivery competence.

- Precision specialists: Vendors focused on microgravure, slot-die and sub-micron coating systems for electronics, medical and energy applications. They command premium pricing for tight tolerances and specialized process knowledge.

- Converter-focused builders: Manufacturers that design modular, conversion-centric equipment for paper, tissue and converting lines where uptime and serviceability are primary decision criteria.

- Regional niche players: Firms that deliver cost-competitive solutions for broad industrial finishing needs, often emphasizing retrofitability and simplicity for mid-tier manufacturers.

Representative firms from our competitive set include long-standing system builders, precision coating specialists and regionally-focused equipment makers. Each exhibits differentiated strengths — from integrated metallization platforms to web-handling expertise and pilot-to-production scalability. For procurement leaders, vendor selection should be driven by three vectors: process fit, service and parts network, and upgrade roadmap compatibility.

Recent vendor developments to watch (selection)

- Black Bros. Co.: Continued high activity in early 2026 highlights the importance of aftermarket attention (e.g., roller-wear detection, maintenance guidance) as a competitive differentiator for system suppliers.

- Bobst Group: Recent product introductions underline the acceleration of integrated metallization and high-speed film coating capabilities that serve flexible packaging and specialty film producers.

- BARBERAN: Trade show exposures and digital roll-to-roll demonstrations signal a push toward combining traditional roller coating with digital finishing capabilities for short-run, high-mix production.

Practical implications for sourcing, operations and M&A in 2026

- Timing CapEx to technology cycles: Avoid ‘spec lock’ on legacy platforms where functional gains from newer slot-die/microgravure systems materially improve throughput. Treat major equipment purchases as strategic options — assess retrofit paths and upgrade modules prior to committing.

- Hedge input-cost exposure: Steel and long-lead components remain volatile. Adopt multi-sourcing, price-indexed contracts and safety-lead-time buffers for critical spares. Consider pushing certain fabricated subassemblies to local partners to blunt tariff and transport risk.

- Prioritize service networks: With market fragmentation, availability of skilled service technicians and spare parts will be a decisive performance differentiator. Evaluate vendors on spare-part lead times, remote diagnostics capability and preventive-maintenance programs.

- M&A and partnership playbook: Consolidation opportunities exist in adjacent niches — retrofitting specialists, control-system providers and localized service networks are attractive targets for larger integrators seeking faster aftermarket scale.

What the PW Consulting report delivers (actionable contents)

Our full market study is structured to be operationally useful for buyers, suppliers and investors planning 2026 initiatives. Key deliverables include:

- Methodology and bottom-up market sizing with a clear, auditable base-year (2025) and scenario-driven forecasts through 2032.

- Tactical buyer playbooks: CapEx decision matrices, retrofit versus replace calculators, and total cost of ownership (TCO) models tailored to common end-use requirements.

- Vendor scorecards and procurement negotiation templates covering technical capability, service coverage, lead times and risk-adjusted pricing.

- Technology roadmaps and adoption curves for automation, high-precision coating technologies and hybrid digital-finishing integrations.

- Supply-chain stress tests: scenario analysis driven by raw material price shocks (including HRC steel trajectories), tariff regimes and logistics disruptions.

- M&A screening framework identifying mid-market targets by strategic fit, recurring revenue potential and aftermarket share.

How to use these insights in a 90–180 day plan

- Immediate (0–90 days): Conduct a supplier health check focusing on spare-part availability and remote-service capability. Begin negotiations to secure priority lead times for critical components.

- Near term (90–180 days): Reassess capital projects slated for 2026 against the report’s tech-adoption scenarios. If upgrading to high-precision coating is considered, initiate pilot programs with precision specialists before full-scale procurement.

- Strategic (next 12 months): Build an M&A watchlist and commence initial outreach for service-network consolidation or acquisition targets to capture aftermarket margins.

Why PW Consulting’s perspective matters

Our analysis synthesizes equipment engineering realities, end-market coating requirements and macro inputs (material pricing and trade policy dynamics) that together determine equipment ROI. The market’s moderate CAGR masks meaningful differentiation: operators that align technology choices with process needs and service strategies will reduce unit costs and shorten payback windows. Conversely, misaligned investments risk technological obsolescence and poor asset utilization.

Note on data access

This brief highlights the strategic contours and operational implications of PW Consulting’s roll coating machine market study. To preserve the tactical utility of our segmentation models and competitive scorecards, we intentionally limit public disclosure of core sub-segment revenue splits and granular regional/application breakdowns here. The full report contains exhaustive tables, vendor benchmarking matrices, and downloadable decision-support tools designed for procurement, engineering and corporate development teams.

Next steps

For procurement leaders, OEM strategists and private-equity teams preparing 2026 plans, PW Consulting offers tailored briefings and model licensing to accelerate decision-making. Contact our industry practice to schedule a briefing, receive sample analytic extracts or commission custom scenario runs tuned to your product mix and sourcing footprint.

For detailed analysis of this topic, please visit the official page:Roll Coating Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com