PW Consulting: Strategic Outlook — EV DC Charge Controller Market (2026 Trailer)

PW Consulting today publishes a focused strategic synopsis of our forthcoming Ev DC Charge Controller Market report — a decision-grade roadmap for executives, product leaders, and investors planning 2026 initiatives in fast charging infrastructure. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study quantifies a high-growth market trajectory (2026–2032 CAGR: 27.5%) and documents the market’s rapid expansion from a multi-hundred-million USD segment in 2020 to an industry exceeding half a billion USD in 2025, with an anticipated material step-up in 2026. This briefing explains why the report matters for next-year choices while preserving the detailed segmentation and proprietary scoring behind our models to encourage licensed access to the full dataset.

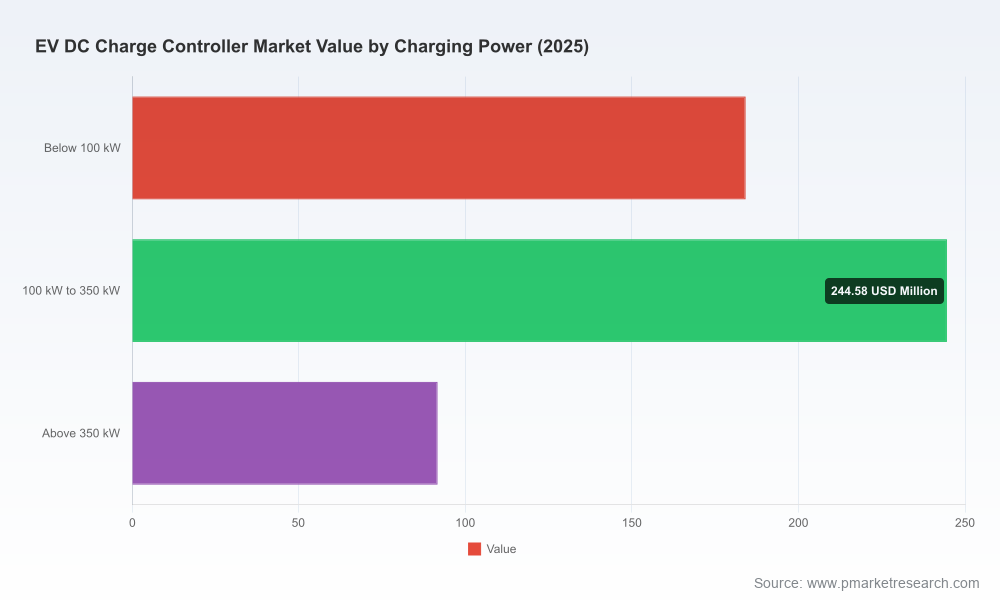

Ev Dc Charge Controller Market

Why this report is mission-critical for 2026 decisions

- Capital allocation under uncertainty: Our forecast framework translates high-level growth and scenario sensitivities into mid-term revenue runways and payback profiles for hardware, embedded software and systems-integration investments.

- Product roadmaps that align with regulation: The report maps product feature prioritization against imminent regulatory inflection points (e.g., AFIR timelines and mandated support for next-gen vehicle-charger communications), so R&D budgets target capabilities that unlock commercial deployments in 2026–2027.

- M&A and partnership terrain: We provide deal archetypes and capability gap maps showing where acquisitions, licensing, or JV strategies compress time-to-market for ISO 15118/Plug&Charge, bidirectional charging, and megawatt-class interfaces.

- Procurement and supplier risk management: A structured supplier scorecard and component-sourcing sensitivity analysis identify single‑source risks (power semiconductors, control SoCs, comms stacks) and mitigation levers for 2026 sourcing cycles.

Market dynamics shaping 2026 strategy

EV DC charge controllers sit at the intersection of power electronics, vehicle communication stacks, and systems integration. Three dynamics require board-level attention for 2026 planning:

Ev Dc Charge Controller Market

- Standards and regulation are accelerating feature requirements. Mandates and codes across jurisdictions are converging on ISO 15118 family capabilities (Plug & Charge, V2G-enabling profiles) and on coherent grid-interactive behavior. AFIR and national regulations elevate these capabilities from differentiators to baseline procurement requirements for public DC infrastructure.

- Technology-enabled efficiency is changing unit economics. Wide bandgap semiconductors and optimized DC/DC/AC power stages materially reduce losses and thermal requirements, enabling higher-power, more compact controllers. This shift changes component sourcing choices and influences total cost of ownership models used by fleet and site operators.

- Product modularity and software are decisive. Buyers increasingly treat charge controllers as upgradeable software platforms rather than fixed-function appliances. This favors vendors with flexible hardware reference designs, robust communications stacks, and field-updatable security and energy-management capabilities.

How PW Consulting’s report turns market noise into operational insight

The published study is intentionally practical: it marries granular technical analysis with commercial strategy tools. Highlights of the report’s operational deliverables include:

Ev Dc Charge Controller Market

- A transparent market sizing and forecast model (2020–2032) that explicates demand drivers and scenario sensitivities — including a base case consistent with the 27.5% CAGR for 2026–2032.

- Technology deep dives on EVCC/SECC architectures, communications stacks (ISO 15118 variants, DIN/IEC interfaces), and power-electronics design choices that impact efficiency, thermal management and modular scalability.

- Regulatory and standards impact matrices linking AFIR, ISO 15118-20, national grid codes and MCS guidance to product compliance pathways and time-to-market implications.

- Supplier and OEM scorecards covering product maturity, software roadmaps, manufacturing scale, and integration readiness — presented as anonymized matrices in the public synopsis and as full vendor profiles in licensed deliverables.

- Commercial playbooks and financial templates (CAPEX/OPEX comparators, lifecycle TCO, payback models) tailored to different deployment archetypes: depot, corridor fast charging and public multi-point stations.

- A patent and IP landscape with freedom-to-operate flags and R&D focus areas to accelerate development while managing licensing exposure.

Competitive landscape — strategic positions and near-term signals

The charge controller value chain features a mix of established electrical engineering houses, software‑centric middleware suppliers, and fast-follow hardware specialists. PW Consulting’s qualitative analysis synthesizes product positioning, go-to-market routes, and recent strategic moves from core industry players.

- Phoenix Contact (Germany) — With its CHARX connect integrated CCS inlet and DC controller initiative, Phoenix Contact signals a push toward simplifying vehicle-side integration for commercial vehicles and heavy-duty applications. That product strategy compresses system integration effort for OEMs and fleets, and the Q3 2026 series production target makes this a near-term consideration for partners planning 2026 pilots.

- chargebyte (Germany) — Focused on communication modules and protocol stacks (ISO 15118, DIN 70121), chargebyte occupies a critical niche for EVSE and EV OEMs seeking certified comms building blocks. Their modular approach reduces software integration time for compliance-driven rollouts.

- Vector Informatik (Germany) — Provider of compact and universal SECC/EVCC controllers where centralized software control and multi-point station management matter; their products appeal to public station integrators seeking validated communication and control layers.

- Watt & Well (France), EcoG (Germany), Delta Electronics (Taiwan) — These vendors emphasize power-electronics and integrated controller platforms, spanning AC/DC and DC/DC conversion with embedded control firmware. Their strength is in system-level optimization for efficiency and heat management.

- ABB, Siemens, Eaton — Global incumbents delivering end-to-end DC fast chargers and comprehensive service ecosystems. Their scale advantage supports deployments requiring extensive site engineering, fleet charging programs, and enterprise-level SLAs.

- Kempower, Tonhe Technology, PHYTEC Messtechnik — Modular system providers and embedded-electronics specialists that address niche deployment models (depot chargers, split-cabinet architectures, developer-friendly controller modules). PHYTEC’s public showcases underscore the developer acceleration value of modular reference designs.

Collectively, the market demonstrates moderate concentration: a small group of global vendors command a meaningful portion of supply while a wider field of specialized players competes on modularity, software, or price. Competitive battles in 2026 will be fought on software ecosystems, compliance certification velocity, and production scale for power-dense architectures.

Strategic recommendations for 2026 (executive checklist)

- Prioritize ISO 15118/Plug & Charge certification pathways now — regulatory timelines make late compliance a barrier to public deployments after 2026.

- Invest in wide-bandgap (SiC) enabled designs where efficiency and power density materially affect site economics; build supply contingencies for critical semiconductors.

- Adopt modular controller architectures with clear upgrade paths for software and communications — preserves CAPEX while enabling future feature rollouts such as V2G and MCS compatibility.

- Separate hardware and software GTM plays: consider licensing or OEM partnerships for protocol stacks while retaining systems integration and service margins.

- Prepare for heavy-duty charging by evaluating megawatt interface readiness and grid connection coordination with utilities and system integrators.

- Use supplier scorecards and scenario stress-tests to inform 2026 procurement cycles and long-lead component orders.

- Plan pilot deployments with clear KPIs tied to lifecycle cost and uptime — operational data will become a defensible moat when scaling after 2026.

What is intentionally reserved for the full report

Consistent with the “trailer” approach, this briefing surfaces strategic conclusions, market momentum and supplier themes while preserving the report’s proprietary granularity: the full dataset contains detailed regional and application-level splits, vendor-by-vendor revenue estimates, and the complete supplier scoring model — all essential for investment underwriting and competitive diligence. Licensing the full report provides access to executable templates, downloadable datasets, and our interactive forecast model to run alternative scenarios tailored to your business assumptions.

Next steps

PW Consulting’s Ev DC Charge Controller Market report is designed as a 2026 playbook. For procurement leads, product chiefs, and corporate strategists preparing budgets or partnerships next year, the study delivers the analytical depth and executable guidance necessary to move from strategy to implementation. Contact PW Consulting or visit our research portal to request the executive summary, licensing options, and custom advisory engagements that translate the report’s insights into a prioritized 2026 action plan.

For detailed analysis of this topic, please visit the official page:Ev Dc Charge Controller Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com