Visible Light Communication Chip Market to Reach USD 2.15 Billion by 2034 at 13.7% CAGR, Driven by Li-Fi Adoption and Smart Lighting Infrastructure

Other |

2026-06-05 11:48:24

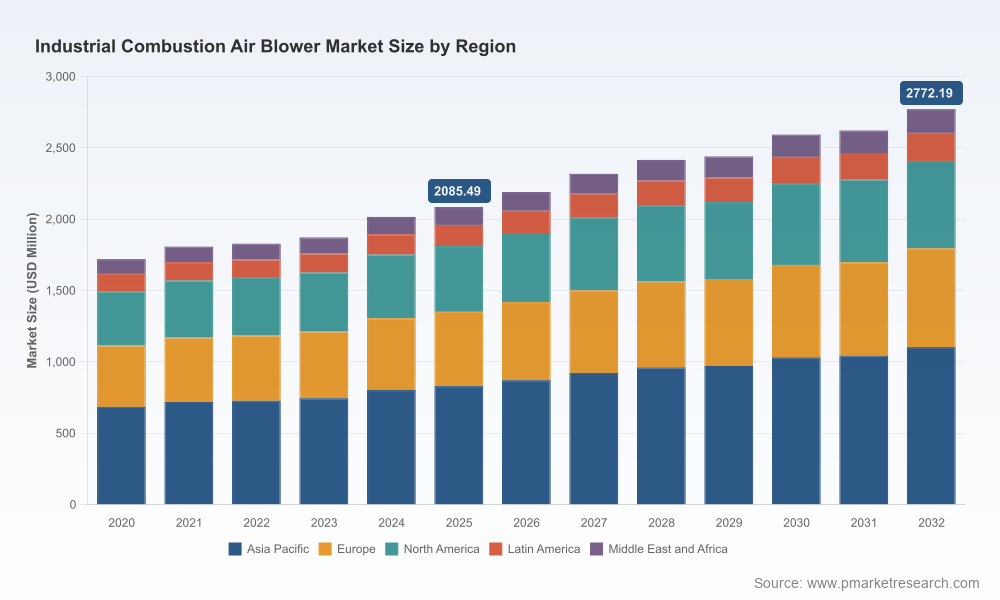

As industrial operators, OEMs, and capital planners prepare for the next wave of plant upgrades and compliance-driven investments, PW Consulting’s latest Industrial Combustion Air Blower Market report delivers the strategic intelligence needed to prioritize actions in 2026. The global market reached an estimated USD 2,085.5 Million in 2025 and is modeled to expand at a compound annual growth rate (CAGR) of 4.15% through the 2026–2032 forecast window. This trajectory reflects steady demand for robust combustion air delivery across process heating, power generation, metals and materials, and critical industrial burners — while simultaneously exposing OEMs and end users to material-price volatility, tightening energy-efficiency standards, and evolving service models.

Industrial Combustion Air Blower Market

Several overlapping dynamics make 2026 pivotal for strategic choices in the combustion air segment. First, enforcement and harmonization of energy-efficiency rules across major markets will change design constraints and procurement requirements for fans and blowers. Second, supply-chain and raw-material cost volatility continues to compress margin levers for manufacturers while amplifying total cost of ownership concerns for end users. Third, a measured but persistent market growth path creates windows for targeted product investment, aftermarket monetization, and selective capacity expansion. For executives choosing where to deploy limited capital in 2026, these forces demand a disciplined combination of regulatory foresight, demand-sensing, and risk-managed sourcing.

Industrial Combustion Air Blower Market

The combustion air blower segment is best characterized as moderately concentrated: the top three suppliers account for roughly one-third of the market, while the top five approach the mid‑40 percent range. This concentration reflects the combination of legacy OEM strength, specialized engineering capability, and integrated system offerings. Our competitive analysis focuses on capability clusters rather than headline share alone — because in 2026, differentiation will come from service networks, customization speed, and compliance capability.

Industrial Combustion Air Blower Market

Representative companies illustrate these clusters: established industrial fan manufacturers that supply rugged-duty forced-draft units and custom pressure blowers; specialist fabricators that design blowers capable of continuous operation at extreme temperatures; and integrated solutions groups that bundle blowers with combustion controls and services for turnkey delivery. Recent market moves underscore these trends: a notable capacity expansion by an established blower manufacturer in early 2026 to reduce lead times; public monitoring of federal and state-level regulatory developments by another legacy supplier; and leadership appointments at mid-market players to support global operations. Collectively, these developments highlight supplier responses to order-book volatility, regulatory compliance needs, and aftermarket growth strategies.

Two non-market forces require special attention in 2026 planning: regulation and raw-material prices. On regulation, accelerated activity in the EU and active state-level programs in North America are tightening energy-efficiency thresholds for electric motors and fans, creating certification and design requirements that will affect product architecture, testing protocols, and allowable performance baselines. Meanwhile, national-level rulemaking processes have shown oscillation — with some proposals withdrawn or delayed — making it essential for manufacturers and buyers to maintain dynamic compliance roadmaps rather than static checklists.

On the input side, steel, aluminum and cast-iron price swings materially influence bill of materials and therefore pricing and sourcing strategies. Our report provides procurement playbooks for hedging exposure, plus design-for-cost approaches that preserve performance while reducing reliance on the most volatile inputs.

PW Consulting’s Industrial Combustion Air Blower Market report is designed as a decision-enabling deliverable: it blends granular engineering guidance, regulatory intelligence, and commercial strategy — while preserving the commercial sensitivity of our segmentation intelligence behind a single access point. Subscribers receive the full model, downloadable scenario tools, supplier scorecards, and an executive briefing package. For leadership teams preparing capital plans or procurement cycles in 2026, we also offer tailored workshops that translate the report’s findings into prioritized action plans matched to corporate risk tolerances and growth targets.

Executives evaluating capital allocation, product strategy, procurement, or M&A in the combustion air space should treat 2026 as a year for decisive positioning — not incremental adjustments. Our report provides the empirical foundation and pragmatic toolset to convert market signals into executable plans. To access the complete intelligence — including the full segmentation model, scenario outputs, and supplier analytics that we intentionally keep behind our subscriber portal — contact PW Consulting for an executive briefing and a demonstration of the forecast model tailored to your strategic questions.

For detailed analysis of this topic, please visit the official page:Industrial Combustion Air Blower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com