Strategic Outlook: Fire Retardant Clothes Market — A 2026 Decision Playbook

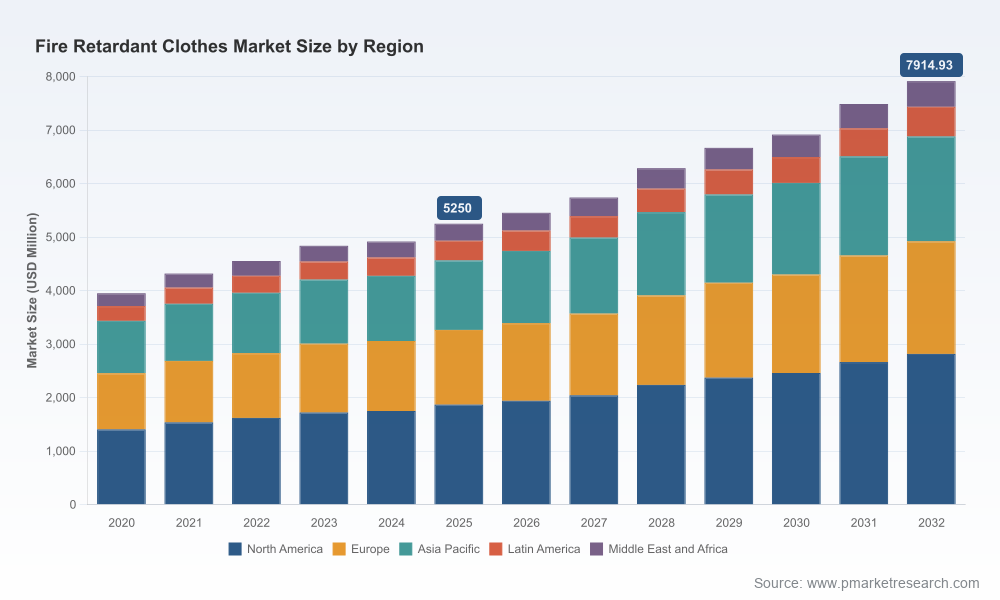

PW Consulting’s latest market study on Fire Retardant Clothes delivers an operational roadmap for leadership teams preparing for the 2026 planning cycle. Built on a 2020–2025 historical audit and a 2026–2032 forecast horizon, the analysis models a resilient market growing at a 6.04% CAGR from a 2025 baseline of USD 5,250 Million to an anticipated market size approaching USD 7,915 Million by 2032. This release synthesizes regulatory inflection points, raw-material economics, competitive dynamics and pragmatic go-to-market playbooks so executives can act with conviction — even as the detailed segment-level tables and proprietary model outputs remain reserved for the full report.

Fire Retardant Clothes Market

Why this report matters for 2026 decisions

- Translates macro momentum into executable choices: when to prioritize product investment, procurement commitments, channel realignment, and M&A.

- Combines regulatory scenario planning (including the latest NFPA updates) with unit-economics stress tests so product managers and procurement teams understand margin sensitivity to raw-material shifts.

- Benchmarks competitive positioning against the leading manufacturers and material suppliers, and highlights the practical moves — acquisitions, partnerships, and capability buildouts — that are shaping market share.

Market dynamics shaping 2026 strategy

The market’s mid-single-digit CAGR masks meaningful structural change. Regulatory tightening — most notably updates consolidating PPE requirements and introducing PFAS restrictions and enhanced testing criteria — is increasing the technical bar for both firefighter and industrial ensembles. At the same time, enforcement focus from OSHA and sectoral standards is accelerating a shift from task‑specific FR use toward mandatory daily‑wear programs in capital‑intensive industries. For commercial leaders, this changes the purchase decision from episodic procurement to ongoing lifecycle management of garments.

Fire Retardant Clothes Market

On the supply side, aramid-based inherent fabrics continue to command the premium share of demand because of superior heat and strength characteristics; industry data points to aramid materials representing a clear majority of flame-resistant fabric revenue. Treated cotton and lower-cost treated solutions remain relevant where economics or comfort dominate. The economics between these material families are material to product strategy: inherent aramid systems sustain higher ASPs and margins but require tighter supply assurance, while treated systems compete on price and scalability. Our scenario models show that a two- to three‑times effective price gap between inherent and treated solutions materially alters break-even across sales and service models.

Fire Retardant Clothes Market

Consolidation and portfolio expansion are accelerating. Recent M&A activity — such as National Safety Apparel’s acquisitions to broaden protective apparel and glove capabilities, and Ansell’s acquisition of a major PPE business — highlights strategic attempts to build end-to-end offerings and cross‑sell into utilities, oil & gas, and industrial accounts. Yet the sector remains moderately fragmented: the top three firms account for roughly 28% of market share and the top five for about 41%, indicating both scale advantages and room for targeted rollups.

Competitive landscape — what the leaders are doing

- DuPont de Nemours: Leveraging heritage intrinsic fibers (Nomex and related aramids) and certification expertise to protect incumbent share in high‑hazard end uses.

- Bulwark Protective Apparel & Carhartt: Doubling down on workwear DNA and channel intimacy with industrial buyers to defend recurring uniform programs.

- National Safety Apparel (NSA): Using acquisitions to widen product scope — from garments into glove and accessory portfolios — creating bundled solutions attractive to large accounts.

- TenCate, Milliken (Westex), Teijin: Competing on advanced textile performance and B2B partnerships with uniform OEMs and specification engineers.

- Portwest, Honeywell, Ansell, Lakeland, PBI and regional specialists: Each plays a defined role — from lightweight anti-static ranges to high-performance firefighting fabrics and disposable protective suits — creating a layered competitive map where specification, compliance and service determine win rates.

For potential entrants or capital allocators, the competitive roadmap is clear: win by combining material‑led differentiation with scale in distribution and value‑added services (testing, certification support, managed garment programs). The market is not winner‑takes‑all; it rewards vertical integration at one end and channel specialization at the other.

What the PW Consulting report delivers (practical contents)

- Robust market sizing and a seven‑year forecast with controllable inputs — enabling CFOs to stress-test revenue scenarios under different pricing and adoption assumptions.

- Regulatory impact matrix that translates NFPA, OSHA and PFAS-related updates into product redesign checklists, certification timelines, and capex implications.

- Raw‑material price and availability playbook, including supplier concentration maps and contract negotiation levers to stabilize aramid exposure.

- Commercial playbooks for selling to utilities, oil & gas, and industrial accounts: procurement triggers, bid templates, and service‑level KPIs for managed programs.

- M&A and partnership screening tools: a prioritized target list template, synergy capture model, and integration risk checklist tuned to this sector’s dynamics.

- Product development and compliance guides: PFAS-free chemistry alternatives, breathability and contamination-removal testing protocols, and reusable vs disposable lifecycle matrices.

- Operational tools: SKU rationalization heuristics, pricing elasticity models, and laundering & rental economics for captive vs outsourced service models.

Prioritized strategic recommendations for 2026

- Secure material advantage: For producers and OEMs, lock long‑term aramid supply contracts or evaluate minority upstream investments to protect gross margin against episodic price spikes. KPI: percentage of aramid needs under multi‑year contract by end‑2026.

- Design for evolving compliance: Fast‑track PFAS‑free chemistry adoption and embed new NFPA testing criteria into product roadmaps; prioritize products that can be certified across major standards to reduce spec‑driven conversion costs.

- Shift from product to program revenues: Launch or scale managed garment services (rental, laundering, compliance tracking) to capture recurring revenue and differentiate against low‑cost competitors.

- Pursue bolt‑on M&A that fills capability gaps (gloves, testing labs, laundering networks) rather than duplicative scale buys; use acquisitions to secure channel access into utilities and integrated industrial accounts.

- Invest in specification influence: Deploy targeted field trials and third‑party validation studies with major end users to accelerate institutional adoption of premium garments as daily wear.

- Operationalize traceability and digital services: Implement RFID and lifecycle tracking to support compliance audits, improve recall response and enable new service monetization.

Risk map and mitigation levers

- Regulatory shifts: Rapid standard changes could force product redesigns. Mitigation: maintain a rolling 12‑18 month certification pipeline and an R&D contingency fund.

- Raw‑material disruption: Aramid supply shocks will pressure margins. Mitigation: diversify suppliers geographically, use forward purchase agreements and consider synthetic blend alternatives where performance allows.

- Price competition: Low‑cost treated solutions may compress ASPs. Mitigation: defend higher margin segments with service bundles and certified performance claims.

- Reputational and litigation risks (PFAS, contamination): Mitigation: adopt transparent materials policies, third‑party testing and recall-ready traceability systems.

How executives should use this analysis in 2026 planning

Use the report as an implementation blueprint rather than an academic read. Specifically: translate the enclosed scenario outputs into five measurable 2026 initiatives (one procurement, one product, one commercial, one M&A, one operational) with assigned owners and an 18‑month milestone plan. The combination of conservative revenue growth assumptions and targeted margin protection levers in our models helps Boards evaluate investment cases with downside resilience and upside capture.

Conclusion — next steps

PW Consulting’s Fire Retardant Clothes Market study is designed to be a decision catalyst for 2026. It packages market scale (2025 baseline and a 6.04% CAGR to 2032), regulatory foresight, supplier economics and competitor playbooks into a single, actionable bundle. We intentionally hold detailed segment-level splits and proprietary model outputs for the full report to preserve the advisory value and to support client workshops where we apply the models to your portfolio. To access the segmented data tables, downloadable scenario models, and prioritized M&A target sets, visit our report page or contact PW Consulting to commission a tailored executive briefing and implementation workshop.

For detailed analysis of this topic, please visit the official page:Fire Retardant Clothes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com