SIC Power Devices for New Energy Vehicles: Strategic Outlook and Action Playbook for 2026

Overview

PW Consulting’s new market study, Sic Power Devices For New Energy Vehicles Market, equips executive teams with the strategic intelligence needed to make high‑stakes 2026 investment and procurement decisions. The report documents a steep industry expansion: the global SiC power device market for new energy vehicles has grown rapidly from under USD 1 billion in 2020 to an estimated USD 5.48 billion in 2025, and our baseline forecast shows continuing acceleration into the early 2030s. Over the forecast window the market is projected to expand at a compound annual growth rate of 28.45%, reaching roughly USD 31.6 billion by 2032. This trajectory is driven by a confluence of vehicle architecture changes, higher-voltage platforms, OEM adoption, and advances in SiC process generations.

Sic Power Devices For New Energy Vehicles Market

Why this matters for 2026 decision‑makers

For OEMs, Tier‑1s, semiconductor suppliers, and investors, 2026 is a pivotal year: product roadmaps, capacity commitments, and qualification programs initiated now will determine competitive positioning as SiC content per vehicle and total vehicle production rise. The market is both large and concentrated — our concentration metrics indicate that the top three players command a significant majority share, and the top five consolidate an even larger portion of the market — creating winner‑takes‑much dynamics for scale players while opening niche windows for differentiated specialists.

Sic Power Devices For New Energy Vehicles Market

Key inflection points for 2026 strategy include:

Sic Power Devices For New Energy Vehicles Market

- Securing wafer, epitaxial, and module capacity against production constraints in SiC substrate supply.

- Accelerating automotive qualification programs (AEC‑Q and newly published JEDEC test methods) to compress time‑to‑revenue for traction inverters, onboard chargers, and DC/DC systems.

- Designing product portfolios and supplier agreements for 800V architectures and higher power‑density inverter topologies.

What PW Consulting’s report delivers (practical, executable content)

The report blends deep market modeling with actionable tools crafted for immediate execution. Highlights include:

- Market sizing and high‑granularity demand scenarios through 2032, with sensitivity cases tied to EV adoption, architecture shifts, and supply constraints.

- Supply‑chain stress maps identifying chokepoints from substrate through module assembly and key levers to de‑risk procurement.

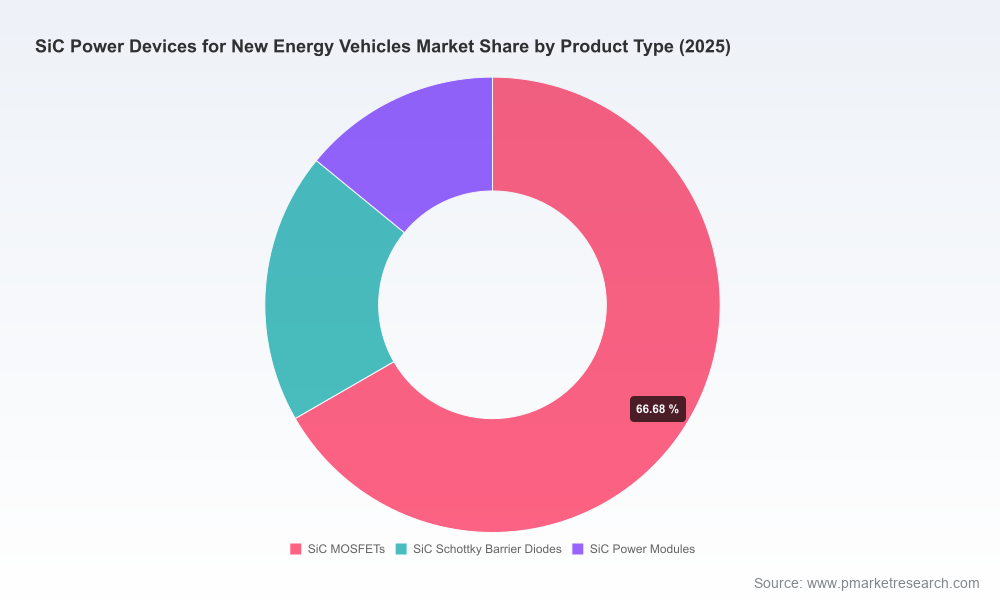

- Technology roadmaps that align device generation (MOSFETs, Schottky diodes, full‑SiC and hybrid modules) with system‑level tradeoffs for efficiency, cost, and reliability.

- Operator‑grade supplier scorecards and a negotiation playbook for OEMs and Tier‑1s to structure supply contracts, capacity reservations, and joint‑development agreements.

- Qualification and validation timelines that translate standards and test methods into project milestones and contingency buffers for 2026 product launches.

- Commercial and M&A frameworks for identifying bolt‑on targets, vertical integration opportunities, and cross‑border partnership models.

- A prioritized 12‑month implementation roadmap for procurement, R&D, and manufacturing leaders — including KPI templates and ROI calculators for migration to SiC technologies.

Market dynamics shaping 2026 strategies

Several industry forces are converging to make 2026 a decisive year:

- Supply constraints at the substrate level — particularly limited availability of large‑format SiC wafers — continue to cap rapid scale‑up and push customers toward long lead times or tiered allocation strategies.

- Manufacturing yield challenges remain material. High dislocation densities and associated yield loss in wafer processing translate into elevated device costs and cyclical supply tightness until upstream process maturity improves.

- Standards and reliability regimes are tightening. Recent JEDEC test methods for wide‑bandgap switching losses, along with established AEC‑Q qualification expectations, mean that suppliers and OEMs must plan extended validation campaigns to meet automotive reliability thresholds.

- System architecture evolution — notably the shift to 800V platforms in high‑performance BEVs and fast‑charging ecosystems — materially increases SiC content per vehicle and reshapes component selection and thermal management designs.

Competitive landscape: positioning and strategic moves

The competitive field is led by a mix of vertically integrated SiC specialists, legacy semiconductor leaders scaling SiC portfolios, and automotive OEMs with in‑house capabilities. Our assessment synthesizes technical differentiation, go‑to‑market models, and recent corporate developments that will influence partner selection and competitive dynamics in 2026.

- Wolfspeed (Durham, NC) — A vertical SiC specialist with aggressive Gen‑4 MOSFET and module roadmaps, emphasizing high power‑cycling capability for traction applications. Recent product introductions underline their push to capture high‑power inverter content.

- STMicroelectronics (Geneva) — A major automotive supplier with broad SiC offerings and deep OEM relationships; focuses on automotive‑grade MOSFETs and diodes for traction and charging systems.

- Infineon Technologies (Neubiberg) — Known for CoolSiC MOSFETs and integrated modules, Infineon balances process innovation with global manufacturing scale and well‑established automotive qualification practices.

- ROHM Semiconductor (Kyoto) — Investing in Gen‑4 MOSFETs and molded module packaging optimized for xEV traction inverters and onboard chargers, emphasizing thermal robustness and integration.

- onsemi (Scottsdale) — Positions EliteSiC MOSFETs and modules toward automotive traction and powertrain customers, pairing product breadth with system‑level support.

- Bosch Semiconductors (Reutlingen) — Bringing an automaker’s perspective to SiC device development, focusing on chips and modules tuned to vehicle integration and system reliability.

- Mitsubishi Electric & Fuji Electric (Tokyo) — Legacy industrial power players supplying full‑SiC and hybrid modules with emphasis on ruggedness and automotive certification.

- Semikron Danfoss (Nuremberg) — Module focus, often integrating devices from specialized suppliers to create e‑mobility assemblies.

- BYD Semiconductor (Shenzhen) — An example of vertical integration by OEMs, leveraging internal device supply to optimize vehicle BOM and capture margin.

Recent product launches and adoption signals — including high‑power Gen‑4 module introductions and early OEM integration of SiC in hybrid platforms — validate the technology pathway but also highlight an execution race among suppliers for automotive qualification and volume capacity.

Strategic recommendations for 2026 (prioritized)

Below are executive‑level actions to take in 2026 to secure advantage and reduce risk. These are ordered by near‑term impact and feasibility:

- Lock in upstream supply commitments: Negotiate multi‑year substrate and epi allocations, or co‑invest in substrate capacity with vetted partners to mitigate lead‑time risk.

- Accelerate qualification with parallelization: Run electrical, thermal, and system‑level qualification streams in parallel where possible; bake JEDEC and AEC‑Q pass criteria into supplier contracts.

- Align architecture migration to a two‑track product plan: Maintain a base‑platform (cost‑optimized) and a high‑voltage SiC track for premium models; this reduces BOM disruption while capturing upside from 800V architectures.

- Pursue strategic partnerships not just suppliers: Structure JDA or capacity reservation agreements with top SiC foundries and module integrators to lock technical roadmaps and price cadence.

- Invest selectively in in‑house capabilities: Consider targeted vertical moves (module assembly, test & qualification) where capture of system‑level IP and margins justify capital.

- Embed scenario triggers in contracts: Use flexible allocation clauses tied to product milestones and market indices to rebalance supply in case of demand spikes or substrate shortages.

Decision checklist: actions to start this quarter

- Map existing BOMs and identify vehicles or trims that are highest‑value for SiC migration in 2027–2028 programs.

- Initiate NDA‑protected technical audits with two leading SiC vendors; prioritize suppliers with demonstrated automotive Gen‑4 capabilities.

- Commission a supply‑chain stress test focused on 200 mm wafer availability and key assembly capacity.

- Define qualification acceptance gates that incorporate JEDEC switching loss methodologies and AEC‑Q reliability thresholds.

- Set aside a capital allocation window for opportunistic equity or JV investments in substrate or epi capacity.

Closing perspective

SiC power devices are shifting from a high‑value niche to a mainstream enabler of vehicle efficiency, range, and fast‑charging performance. For firms that move decisively in 2026 — securing supply, compressing qualification timelines, and aligning product architecture with system‑level benefits — the upside is outsized. Conversely, delayed or purely transactional sourcing approaches risk margin erosion and missed platform wins as the market consolidates.

PW Consulting’s Sic Power Devices For New Energy Vehicles Market report consolidates the forecasts, supplier intelligence, risk matrices, and executable playbooks executives need to operationalize a winning strategy. For access to the full dataset, segmented demand models, supplier scorecards, and our 12‑month implementation toolkit, please visit our report page to obtain the complete study and proprietary appendices.

For detailed analysis of this topic, please visit the official page:Sic Power Devices For New Energy Vehicles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com