Dual Hardness Polyurethane Wheels UAE – The Ideal Solution for Industrial Mobility

Other |

2026-06-17 17:21:35

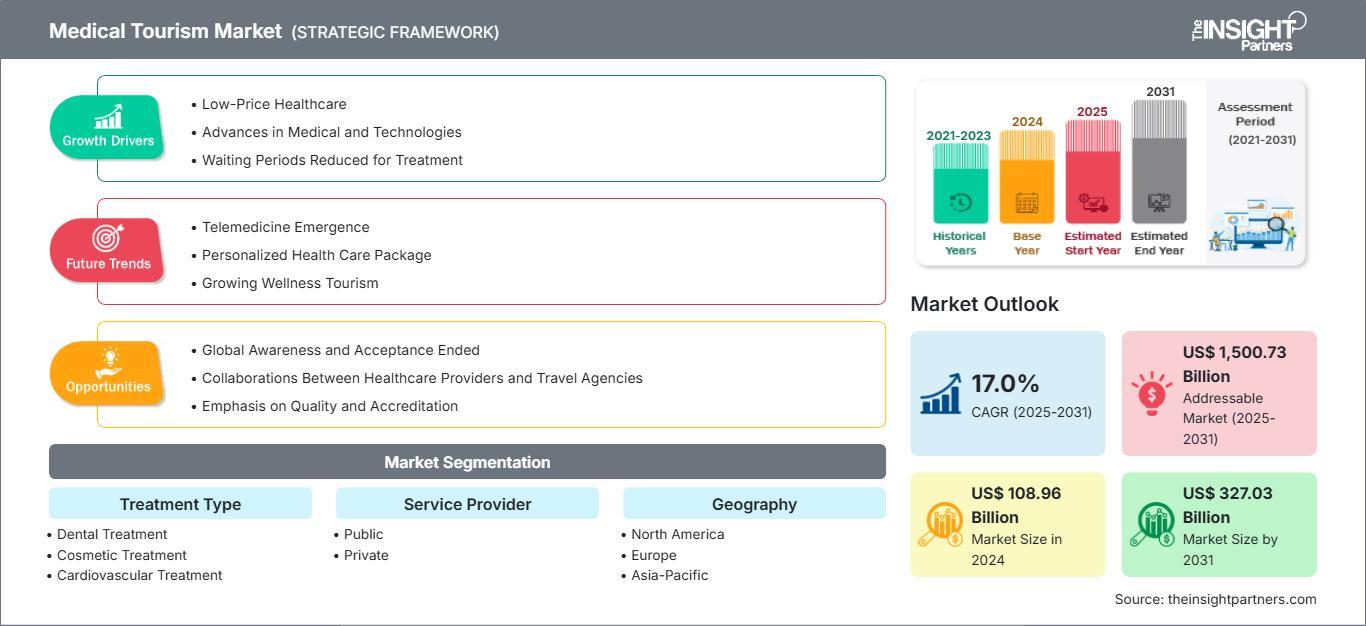

The Medical Tourism Market Segmentation landscape of cross-border healthcare is rapidly evolving into a sophisticated ecosystem where specialized care meets high-end hospitality. As patients become more discerning about their treatment pathways, understanding the nuances of the industry becomes essential for stakeholders. The Medical Tourism Market size is expected to reach US$ 327.03 Billion by 2031. The market is anticipated to register a CAGR of 17.0% during 2025 through 2031. This growth is heavily dictated by how service providers align their offerings with specific patient needs across various medical categories.

The shift toward a more structured market is visible in the way procedures are now being marketed as "Medical Value Travel." Instead of general medical trips, the industry is seeing a rise in bundled care packages that integrate pre-operative tele-consultations, the main clinical procedure, and post-operative wellness programs. This holistic approach ensures that the patient’s journey is managed professionally from their home country to the destination and back.

Download Sample Report -https://www.theinsightpartners.com/sample/TIPRE00003739

Medical Tourism Market Segmentation Analysis

To understand the trajectory of this industry, it is vital to examine the specific segments that define its structure. The market is primarily categorized by treatment type, service provider, and tourist type.

Market Drivers and Trends

The primary driver for the current surge in the medical tourism market is the escalating cost of healthcare and insurance premiums in developed regions. When a cardiac bypass in the United States costs roughly US$ 100,000, and the same procedure in India or Thailand is priced under US$ 10,000 at a JCI-accredited facility, the economic incentive becomes undeniable.

Furthermore, the "Zoom Boom" legacy has created a permanent uptick in the cosmetic and aesthetic segment. There is a growing trend where patients travel not just for lower prices, but for "technique-specific" results, such as seeking out renowned rhinoplasty specialists in Turkey or dental implant experts in Mexico. The integration of AI and digital health also acts as a catalyst, allowing hospitals to provide seamless follow-up care through telemedicine, which reduces the need for extended stays abroad.

Market Share Analysis and Geography

Asia Pacific remains the powerhouse of the industry, currently holding a dominant market share of nearly 46%. Countries like India and Thailand have invested heavily in healthcare infrastructure, making them top tier destinations for complex surgeries. Meanwhile, the Middle East is positioning itself as a luxury medical hub, focusing on high-end specialized treatments in oncology and fertility to attract patients from across the GCC and Europe.

In North America, the market is characterized by a high volume of outbound patients traveling for dental and bariatric surgeries. Conversely, European nations like Germany and Spain are attracting inbound patients for advanced orthopedic and oncology treatments, leveraging their reputations for clinical excellence and research-backed protocols.

Top Players and Market Leaders

The competitive landscape is dominated by large-scale hospital networks that have standardized their international patient workflows. These leaders are focusing on international accreditations like JCI and GHA to build trust. Key companies include:

Market News and Recent Developments

One of the most significant recent developments is the expansion of "E-Medical Visas" across several Asian and Middle Eastern countries, which has slashed the document approval time from weeks to just a few days. Additionally, there is a notable trend of private hospital chains in India and Malaysia expanding their capacity by thousands of beds to meet the post-2025 surge in medical travelers. Strategic partnerships between Western insurance providers and Asian hospital networks are also becoming more common, further legitimizing medical tourism as a mainstream healthcare option.

As the industry moves toward 2031, the focus will shift from "cheaper care" to "better care," with medical technology like robotic surgery and proton therapy becoming standard offerings in destination hubs. The Medical Tourism Market Segmentation will continue to refine itself, ensuring that specialized clinics and multi-specialty hospitals can cater to the diverse and growing needs of the global patient population.

Related Report :

· Medical Aesthetics Market Analysis and Opportunities by 2028

Contact Information -

Email: [email protected]

Phone: +1-646-491-9876

Also Available in : Korean German Japanese French Chinese Italian Spanish