The Importance of Accredited Cosmetic Surgery Centers in Riyadh

Health |

2026-06-01 05:25:02

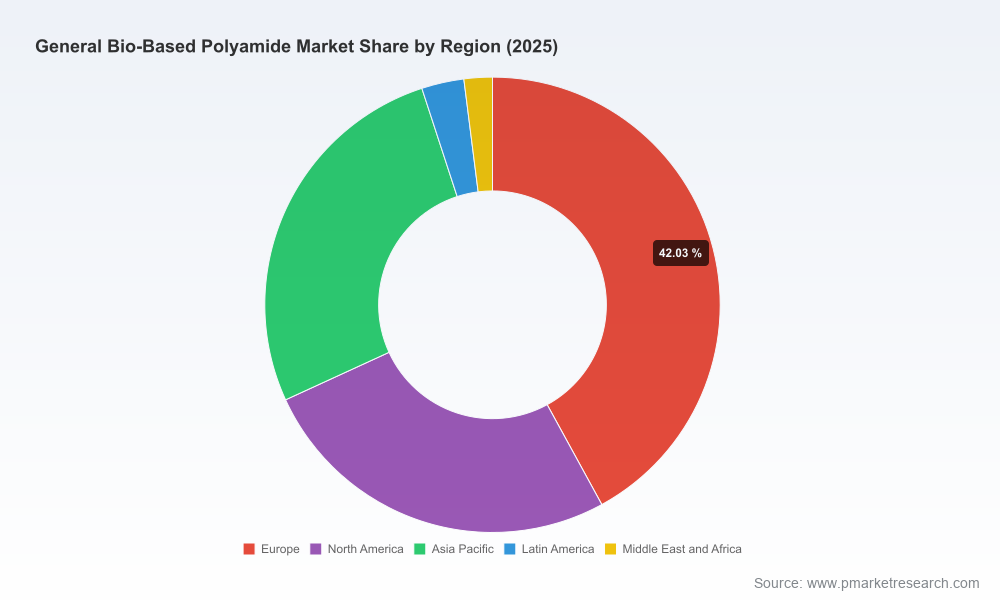

PW Consulting's latest market study on General Bio-Based Polyamides synthesizes macro dynamics, competitor moves, feedstock realities and regulatory drivers into a compact, decision-ready intelligence package for 2026. The market has transitioned from niche sustainability experiments into a commercially meaningful industrial value pool: our base-year sizing shows an industry that moved from roughly USD 1.1 billion in 2020 to about USD 2.25 billion in 2025, and is projected to scale to approximately USD 6.0 billion by 2032 — an implied compound annual growth rate of roughly 15.02% across the forecast window. These macro signals, combined with concentrated supplier activity (CR3 ~48.5%, CR5 ~62.3%), frame a near-term strategic inflection point for suppliers, OEMs, tier-one buyers and financers heading into 2026.

General Bio Based Polyamide Market

Actionable foresight: The market growth trajectory creates a narrow window where first-mover scale, certification and supply-security create durable competitive advantage.

General Bio Based Polyamide Market

Commercial clarity: We translate growth into practical decisions — which grades to prioritize, where to site capacity, how to structure offtake contracts, and how to price value propositions under different sustainability claims.

General Bio Based Polyamide Market

Risk mitigation: The report converts feedstock volatility, regulatory change and concentration risk into procurement and hedging playbooks that are executable during 2026 planning cycles.

Market sizing and conservative / aggressive forecast scenarios (2026–2032), with modeled demand drivers mapped to end-use adoption curves across automotive, textiles, consumer goods, electronics and industrial segments.

Supply-side intelligence: a proprietary supplier database, capacity build-out pathways, and a rolling 24-month “capacity-to-demand” dashboard for fast scenario stress-testing.

Raw material and cost modelling: end-to-end feedstock value chains (castor oil, sebacic derivatives, bio-attributed streams), monthly price-sensitivity matrices, and working capital impacts for different sourcing strategies.

Regulatory & certification playbook: assessment of REACH, EU Green Deal levers and sustainability labels (including guidelines for ISCC PLUS / bio-attribution claims), and a compliance calendar for 2026 procurement and product-launch gates.

Technology & product readiness: TRL-style assessment for major bio-polyamide chemistries, performance parity mapping versus fossil analogues, and recommended R&D focus areas with estimated time-to-market and capex envelopes.

Commercial GTM modules: route-to-market options, OEM engagement templates, price-premium capture models, and case studies for long-term supplier alliances and co-development agreements.

M&A and partnership scanner: prioritized target archetypes, valuation drivers, simple financial checklists and integration risk flags for strategic acquirers and private equity buyers.

Decision tools: 30/60/90-day execution plans, a capital allocation scorecard, and an interactive risk-adjusted IRR calculator tailored to bio-based polyamide projects.

Strong growth, fast consolidation: Rapid volume growth alongside meaningful market concentration means scale is increasingly decisive. New entrants must plan for two-dimensional competitiveness — technology differentiation plus secured feedstock — rather than relying solely on sustainability narratives.

Feedstock realities: Castor oil continues to dominate the renewable feedstock mix, creating both opportunity and exposure. Historical price swings in castor-derived intermediates can be material (monthly volatility has been observed—up to the order of tens of percentage points in extreme months), which necessitates active hedging, multi-feedstock sourcing and contractual protections for 2026 procurement strategies.

Certification and carbon accounting: ISCC PLUS and bio-attribution are maturing into procurement table stakes for many OEMs. Separately, validated low-carbon production footprints (for example, certified production pathways that have demonstrated carbon footprints close to ~1.3 kg CO2e/kg on certain PA11 chains) can materially change commercial negotiations and value capture.

Regulatory tailwinds: European policy drivers — REACH compliance tightness and Green Deal incentives for renewable materials — are accelerating adoption in regulated verticals (automotive, packaging) and reshaping supplier selection criteria.

The competitive set blends incumbent chemical majors with specialized bio-polymer players. Key players profiled in the report include a mix of integrated value-chain operators, technology-rich specialty producers, and regional scale suppliers. Notable strategic configurations and recent moves to note:

Arkema: vertically integrated into castor-derived PA11 and has expanded transparent Rilsan Clear production in Singapore (capacity start-up announced January 2026). Its pathway to a low production carbon intensity for certain PA11 chains is a commercially disruptive capability for high-value segments such as eyewear, medical and electronics.

Evonik: markets multiple partially and fully bio-based grades targeting technical applications and additive manufacturing; a relevant partner for performance-sensitive segments.

DSM-Firmenich (Envalior): positions bio-based high-performance grades for under-hood automotive and structural components with differentiated moisture-performance characteristics.

DOMO Chemicals: progressing mass-balanced, ISCC PLUS-certified PA6 variants (product extension launched 2025) — an important example of how certification plus supply assurance is being commercialized.

Regional and technology specialists (Cathay Biotech, RadiciGroup, Solvay, Mitsubishi Gas Chemical, Toray, Avient, BASF): collectively, these players push innovation across monomer chemistry, fibers, additive manufacturing powders and bio-attributed fossil blends.

For producers considering capacity investments: prioritize flexible assets that can switch between feedstocks or grades; secure backward integration or long-term castor/sebacic feed contracts before final investment decisions; model projects under conservative feedstock-price scenarios.

For OEMs and tier-one buyers: implement a supplier certification ladder (basic ISCC PLUS → low-carbon product → joint development) and include explicit price/volume/failsafe terms in multi-year offtakes to limit exposure to feedstock shocks in 2026 procurement cycles.

For R&D leaders: accelerate performance parity projects that lower moisture uptake and increase thermal stability to open automotive and industrial windows; prioritize pilot-to-production transition paths that demonstrate both mechanical performance and verified lifecycle carbon reductions.

For investors and M&A teams: target bolt-on technology plays that address feedstock flexibility, compounding/compounding know-how, and verification capabilities (LCA and chain-of-custody). Use our M&A scanner to filter targets that improve either margin resilience or route-to-market.

For procurement and risk teams: deploy blended sourcing strategies, incorporate indexed pricing bands tied to feedstock indices, and test call-option style contracts to cap downside exposure while preserving upside participation in price dislocations.

Day 0–30: Executive briefing and one-page action plan. Run our “feedstock stress test” using your procurement data to identify the single largest exposure to castor-based inputs and execute immediate short-term hedges where justified.

Day 30–60: Engage prioritized suppliers for ISCC PLUS / low-carbon proof points; pilot a dual-sourcing clause in at least one major contract; commence engineering studies for flexible capacity or compounding upgrades.

Day 60–90: Finalize 2026 CapEx allocation using the PW risk-adjusted IRR tool, shortlist M&A or partnership targets from the report’s scanner and present a board-ready recommendation.

This commentary gives a high-level view of the forces that will shape strategic choices in 2026. PW Consulting’s full General Bio-Based Polyamide Market report contains the granular segmentation tables, proprietary price and margin models, supplier-by-capacity matrices and client-ready implementation modules that executives and investment committees need to act with conviction. If your 2026 plan hinges on timely decisions — from brownfield upgrades to long-term supply agreements or targeted acquisitions — the full dataset and model deliver the missing operational detail. Contact PW Consulting to access the complete report and the interactive decision tools referenced here.

For detailed analysis of this topic, please visit the official page:General Bio Based Polyamide Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com